Subscribers Only

Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

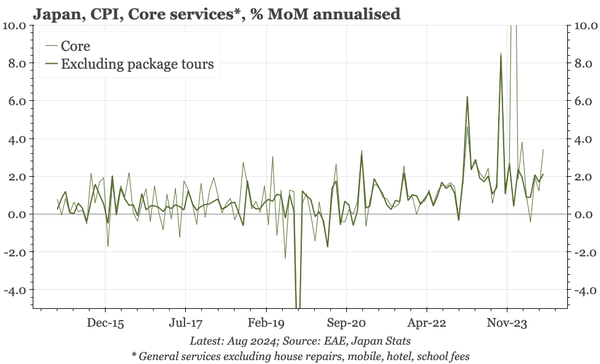

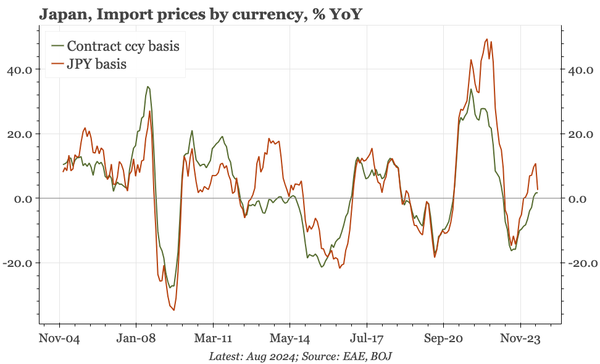

So, no surprise from the BOJ today. But the bank's statement remained constructive, revising up consumption. Today's separate services inflation data for August was also firm. Import prices have receded on the rising JPY, but we'd think the BOJ should be hiking again with a strong Q3 Tankan.

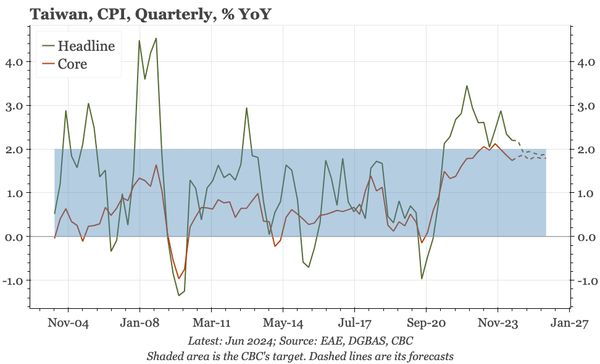

Taiwan's CBC kept rates on hold yesterday, but hiked the RRR to control housing. More interesting was the bank's very benign outlook: growth neither fast nor slow, and inflation falling to just within its target range. Particularly regarding inflation, that doesn't allow much room for error.

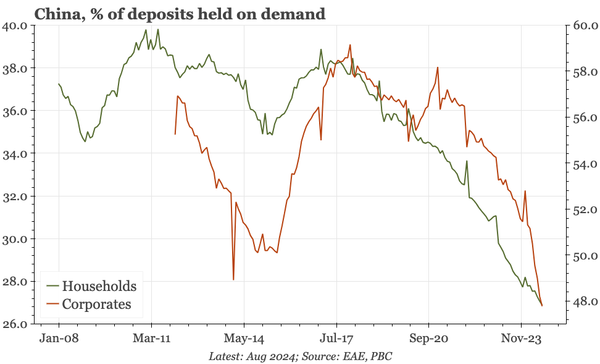

While data for the corporate sector are distorted by regulatory changes, this is still one of the most important charts for China macro. As long as companies and especially households are locking up their money in time deposits, it is highly unlikely that inflation and nominal growth rebound.

Core machine orders are one of the BOJ's standard leading indicators, always getting a mention in the bank's economic outlook reports. The data are, however, volatile, and today's numbers for July don't show any new direction being established.

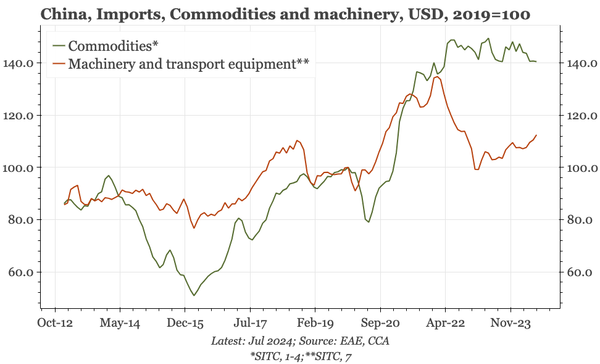

China's imports are two-speed. That's like the economy, but with a big difference: whereas for macro it is property that is weak while mfg is strong, for imports it is commodities that are more resilient than capital goods. Like the overall macro muddle through, that resilience likely can't last.

Japan's exporters haven't reacted in standard fashion to JPY weakness, not cutting prices to increase volumes. Indeed, volumes fell YoY in August. That contrasts with the clear recovery in the rest of the region. It means higher JPY earnings for exporters, but less incentive for domestic capex.

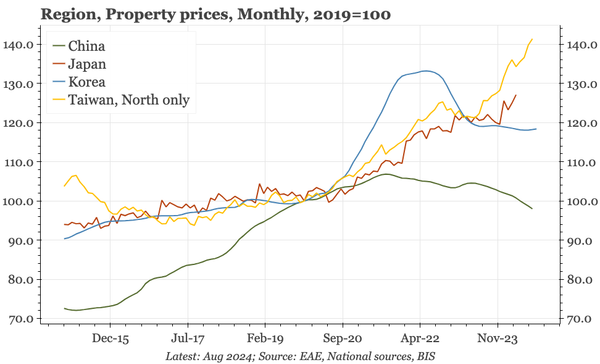

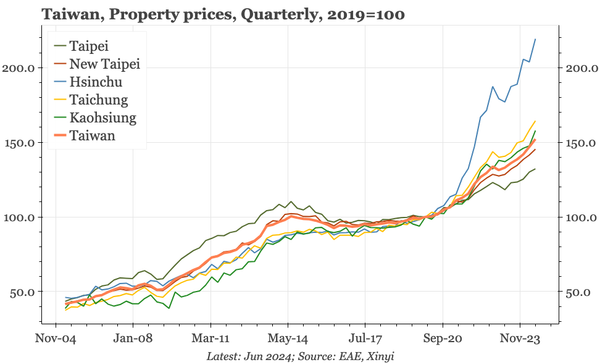

Exports feel a bit peaky, and CPI inflation has eased. But property price inflation isn't cooling. Perhaps an export slowdown changes that – the fastest price gains are in Hsinchu, home of TSMC. But unless and until that happens, it is very difficult for the central bank to turn doveish.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

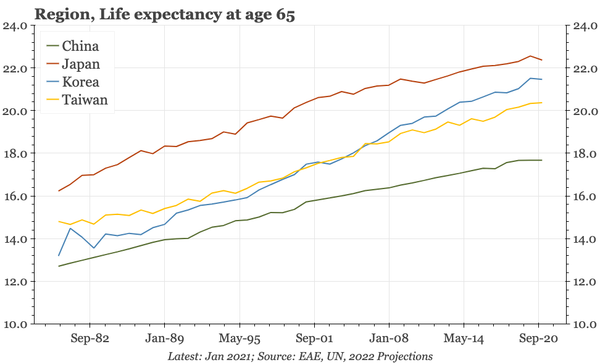

This week's announced rise in the retirement age is economically welcome. But the rise of 3-5 years, implemented over 15 years, is modest. In that time longevity is likely to rise almost as much, meaning by the time this week's changes are completed, China will still be at square one.

August data suggest GDP is now only growing by around 4% YoY. The headwinds remain property activity, which dropped again in August to new lows, and retail sales, which has now contracted MoM in five of the first eight months of 2024. Sustaining muddle through is getting much more difficult.

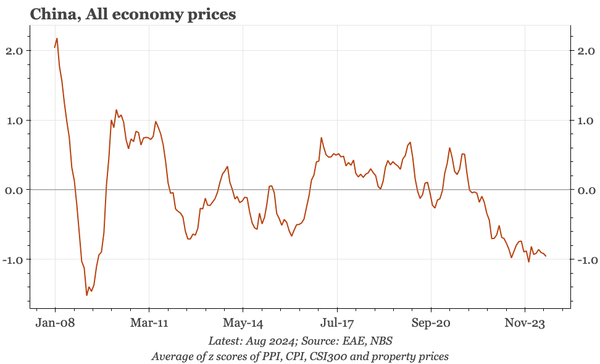

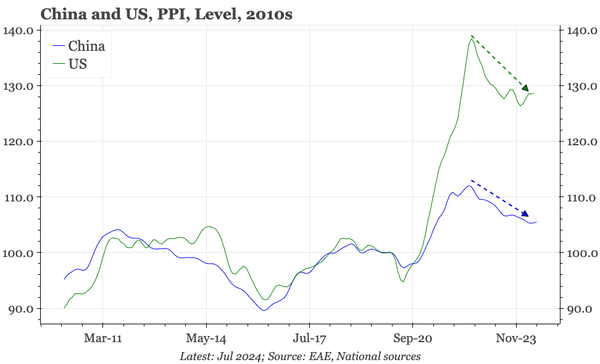

Today's industrial price data for the first 10 days of September and property prices for August show intensified deflationary pressure. Yesterday's monetary data were weak. The PBC said yesterday that it will focus on price stability, but it also said it has plenty of other things to do as well.

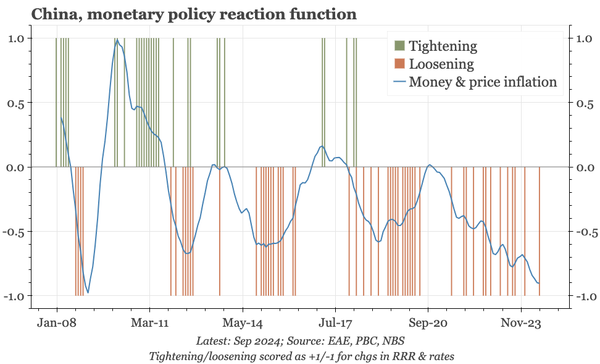

More than 12M ago, we argued yields should fall. In that respect, today's drop to record lows isn't a surprise. We don't see anything fundamental yet to cause a change in direction. That's based on four factors: the PBC's reaction function, inflation, household savings, and the CNY.

It is clear that the market moves that accompanied the BOJ's July policy changes are impacting prices. But it isn't obvious that they have derailed the underlying path for the economy. It seems to us the door remains open for an October hike, with the obvious risk being events in the US.

The shift in $JPY is clearly having an impact, with JPY import price inflation dropping from July's +10.8% YoY to just 2.6% in August. But BOJ officials suggest they remain confident in the underlying outlook, which isn't unreasonable given the resilience of survey data such as today's BSI.

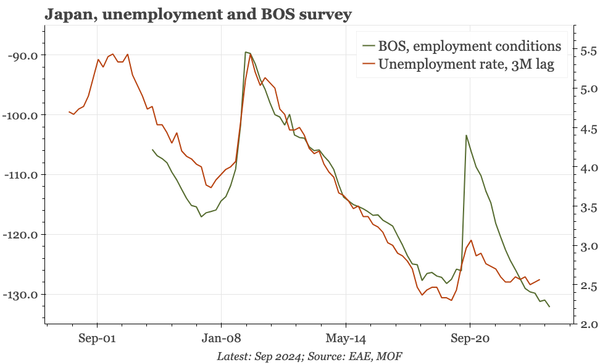

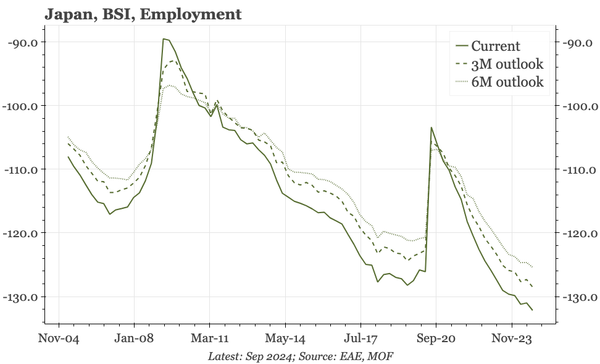

A critical part of the BOJ's positive narrative is the labour market tightness shown by the Tankan. That survey will be released next in early October, but early signs are positive, with today's BSI survey from the MOF, also quarterly, showing tightening over all three of its measurement periods.

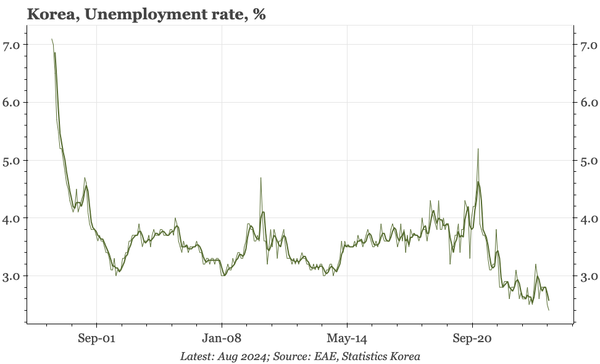

Data today show exports still growing, and UE still low. The BOK hasn't been ignoring exports, but the bank has been more focused on weak domestic demand. The labour market data don't suggest that weakness is disappearing, with strength in employment concentrated in state and part-time positions.

Just looking at the headline labour market data, and it would be difficult to know that the BOK is moving steadily towards a rate cut. Data released today show that in August, the unemployment rate fell to a new multi-decade low of just 2.4%!

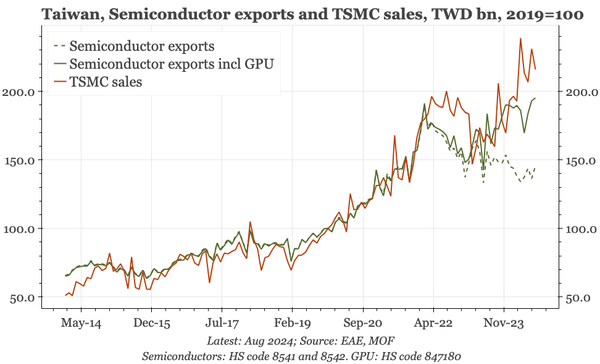

TSMC's sales were softer in August (especially after adjusting for seasonality), and with sentiment towards the sector starting to weaken, it seems possible that the best of the cycle is now in the past. That will limit further improvement in Taiwan's overall exports.

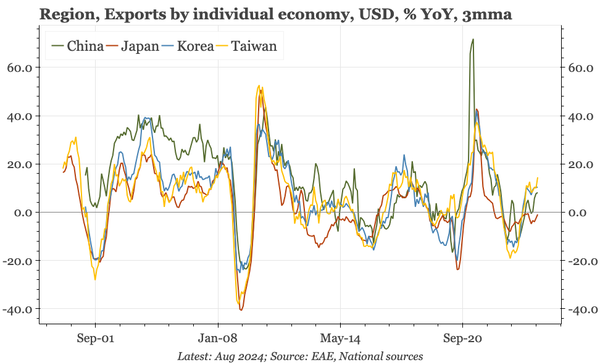

It seems increasingly unlikely that exports can offset the weakness of domestic demand. Today's export data for August weren't strong. Volumes might be better, but the regional export cycle is likely peaking, and that at a time when China's domestic demand seems to be weakening further.

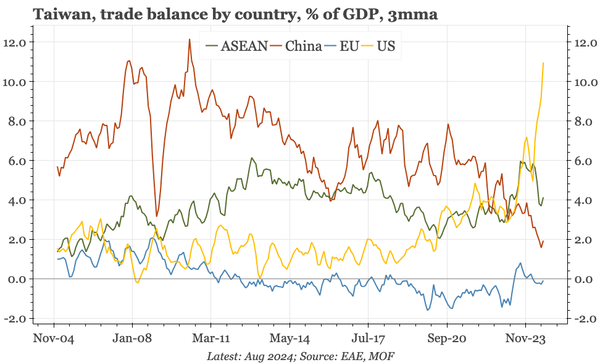

While exports jumped in August, with signs that the semi upswing is losing steam, it still seems likely that the export peak is near. Pretty much all the growth is coming from the US, which is propelling a surge in the bilateral trade surplus. That makes Taiwan vulnerable if Trump wins re-election.

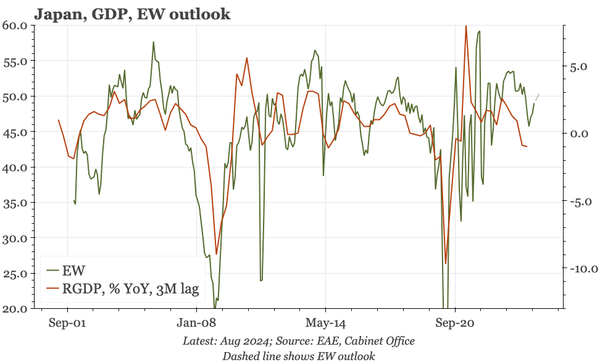

The Economy Watchers survey improved in August. That matters, as if the market vol around the BOJ meeting in July had caused damage to the cycle, it should be showing up by now. The rise in the household score is particularly important, given the previous weakness of consumption.

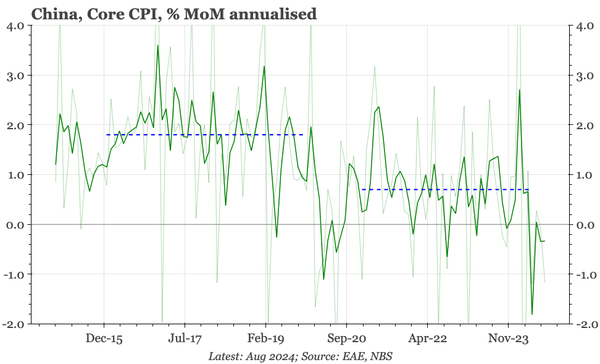

MoM core CPI fell again in August, and while perhaps a bit too early to pronounce that China is definitively in core deflation, it is getting close. PPI deflation also worsened, and the leads suggest that will continue. Despite stronger food prices, it is likely interest rates continue to fall.

Last week I gave a short conference presentation updating the framework I've been using to think about China today versus Japan in the 1990s. The slides focus on deflation, manufacturing, currencies, and household consumption.

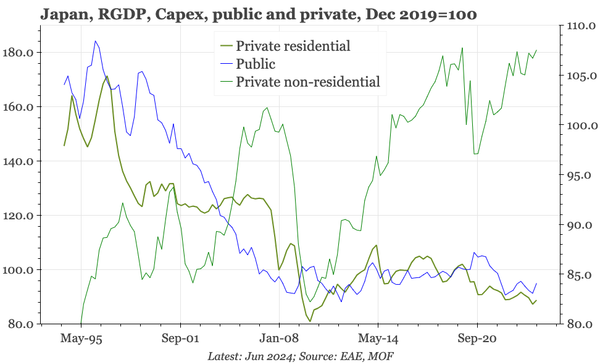

In today's second release, Q2 GDP growth was revised down, from 3.1% QoQ annualised to 2.9%. The driver was weaker capex, which, like consumption, has yet to rise back above pre-covid levels.