Public Post

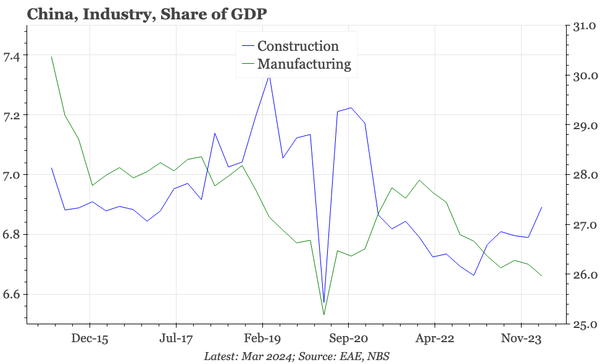

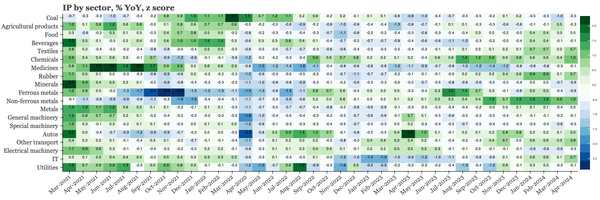

China – broad-based pick-up in IP growth

IP growth remains the bright spot in China's economy, with the pick-up in April being broad-based across industries.