Public Post

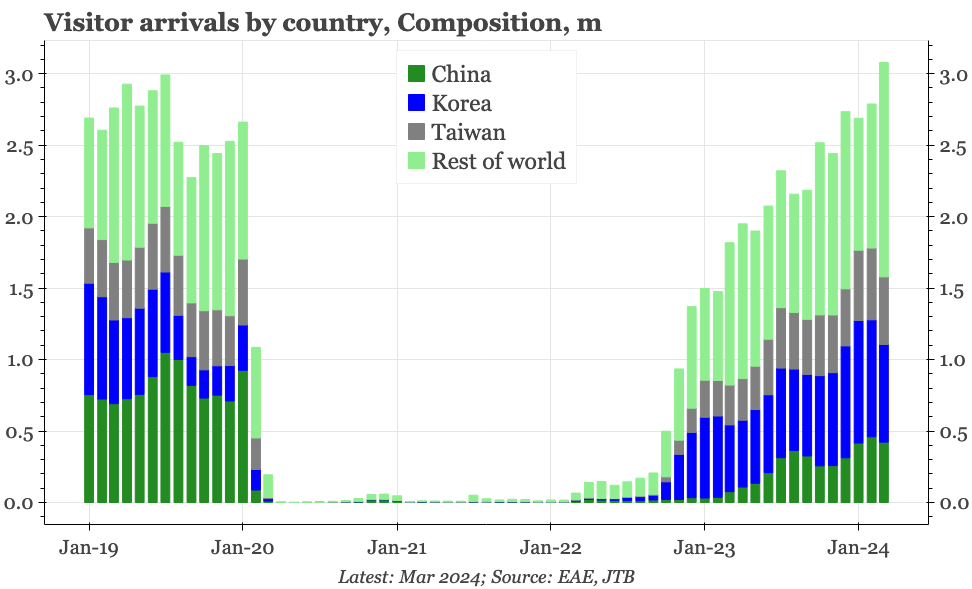

Japan – tourism diversification

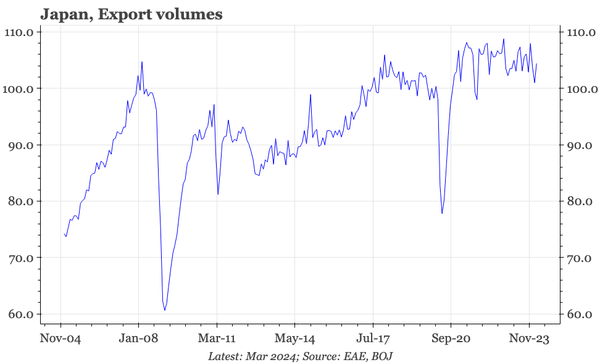

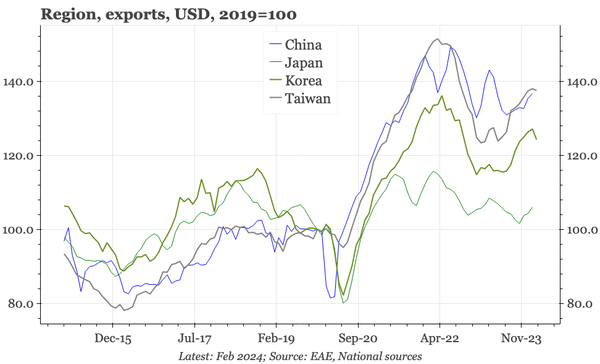

The cheap JPY isn't boosting Japan's merchandise exports, but it has helped with a sharp recovery in tourism, even though arrivals from China remain subdued.