Subscribers Only

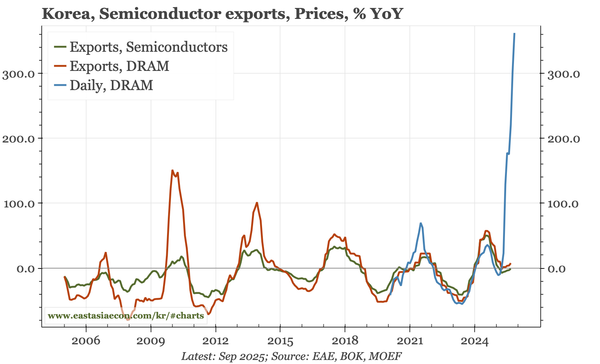

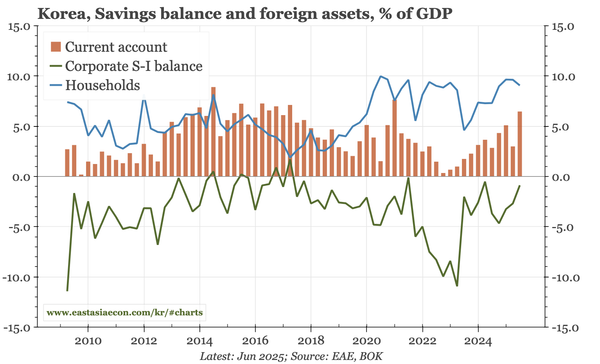

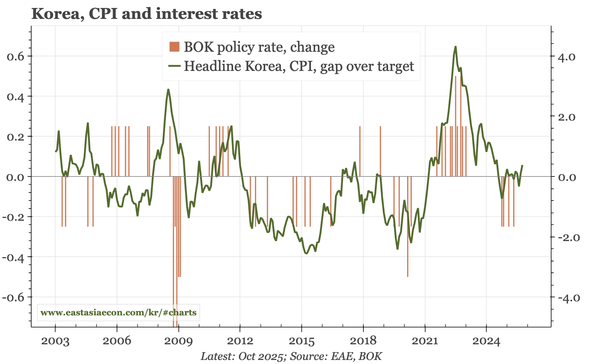

Korea – "financial dominance"

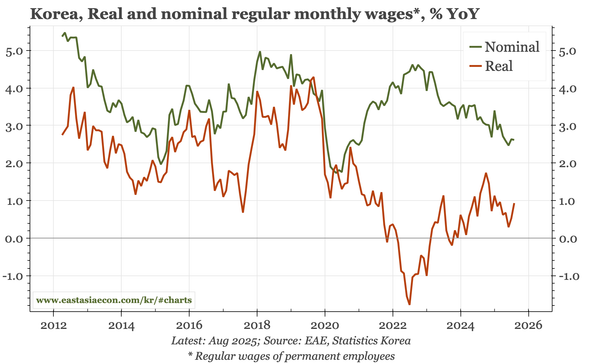

With October meeting minutes, export and labour market data, there's enough to review the outlook for Korea. I think the underlying economic picture remains consistent with more cuts. But the minutes show Board members continuing to prioritise concerns about KRW weakness and house price strength.