Public Post

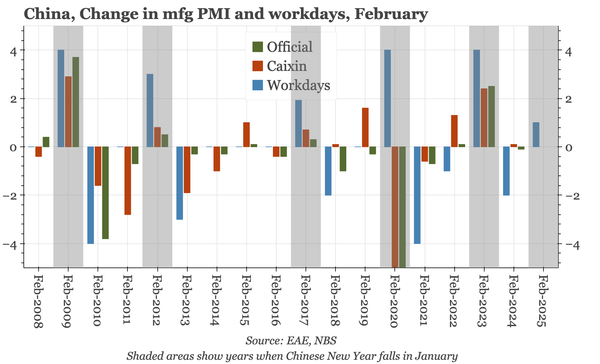

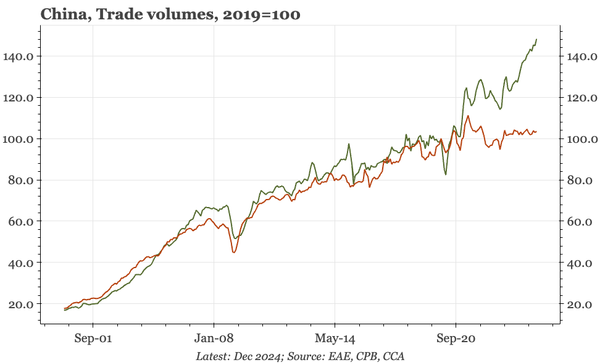

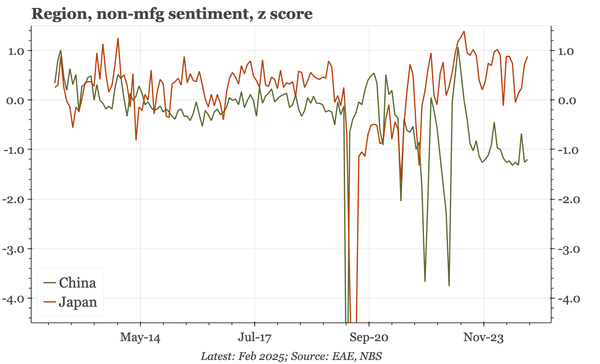

Region – Japan outperforming China services

This is a good way of showing the contrasting cyclical momentum in China and Japan. Except for the sudden stops during covid, the services PMI in China is the lowest on record. In Japan, it is near the strongest.