Public Post

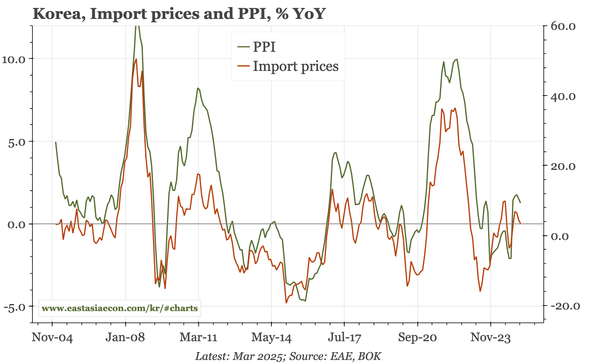

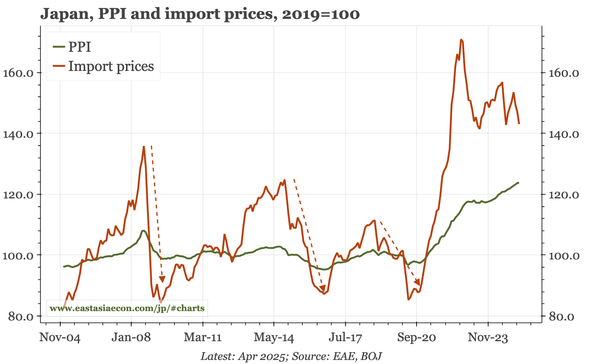

Japan – import prices versus PPI

The gap between PPI and import prices is a useful way of thinking about inflation and the BOJ. Usually, the gap is closed as import prices are cut by a combination of global recession and JPY strength. If neither happens, PPI inflation isn't likely to recede, and BOJ hikes will remain on the table.