Public Post

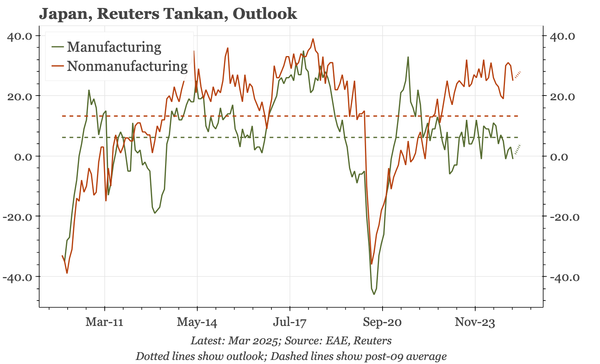

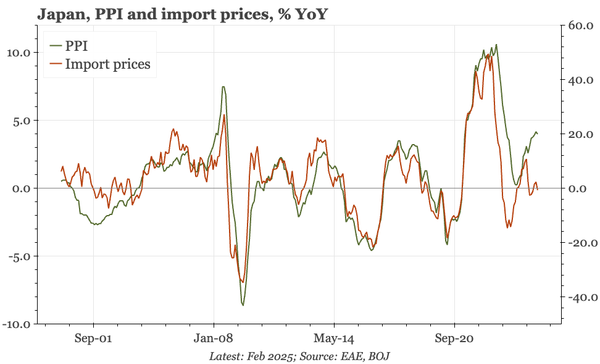

Japan – inflation expectations still strong in Q1

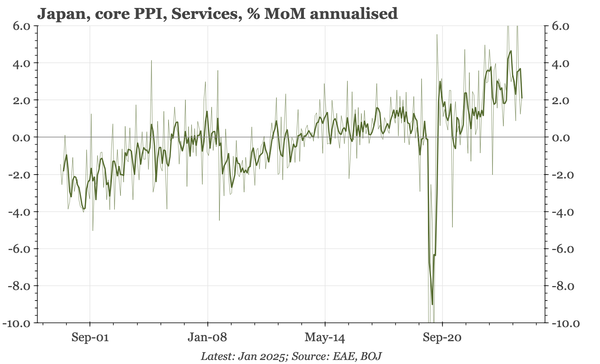

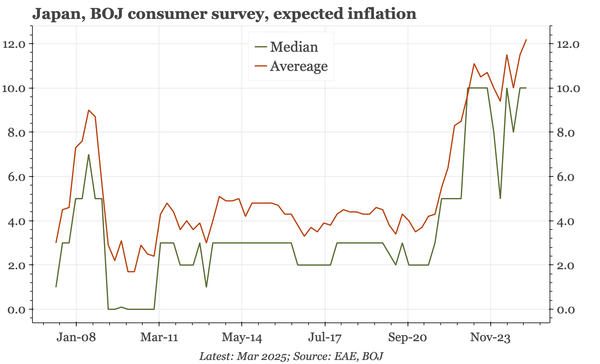

In today's BOJ quarterly consumer survey, inflation expectations remained strong, just as they had in the corporate Tankan last week. Given tariffs, this is not nearly as significant for the BOJ as it would have been, but it is better to be facing Trump's shock with inflation rather than deflation.