Public Post

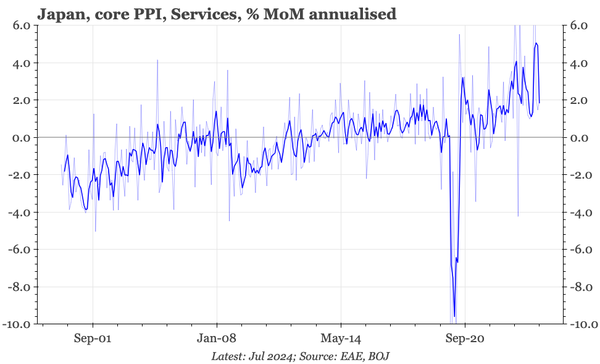

Japan – upstream services inflation steady

Services PPI inflation eased back in August, but that was partly base effect. The BOJ's new high-labour content measure isn't that different, and remains near 3%. Sequentially, SPPI is running around 2%, but all the volatility since 2022 makes it difficult to discern the underlying trend.