Public Post

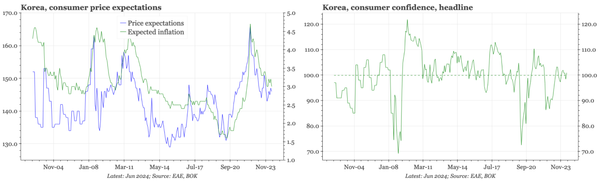

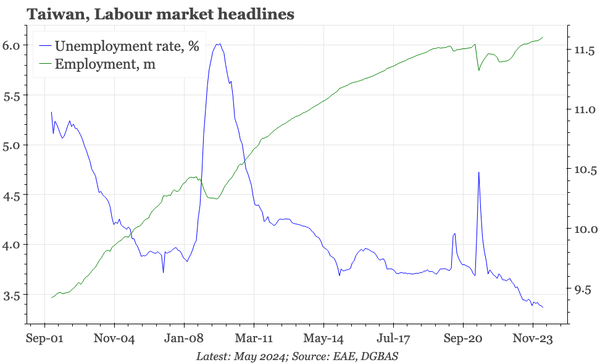

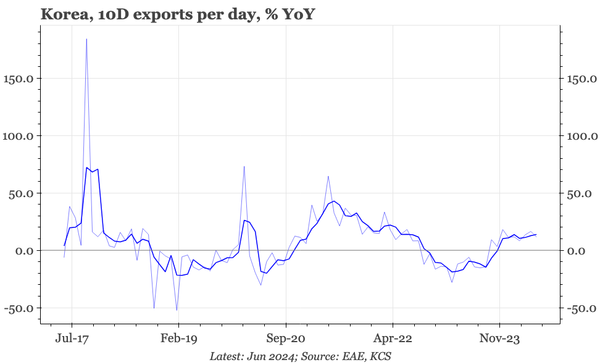

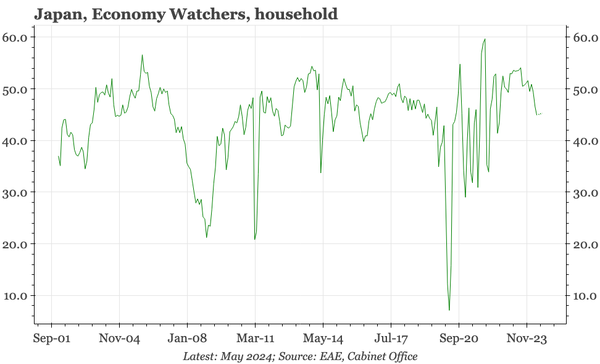

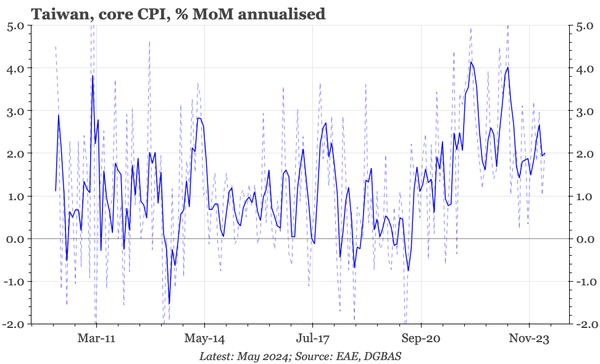

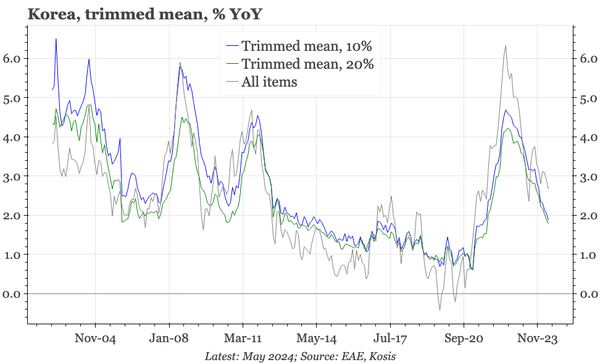

QTC: Korea – underperforming domestically too

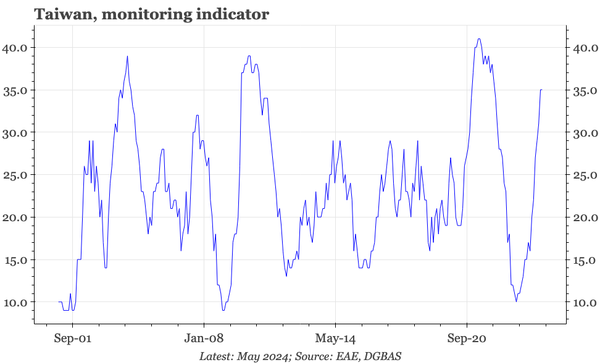

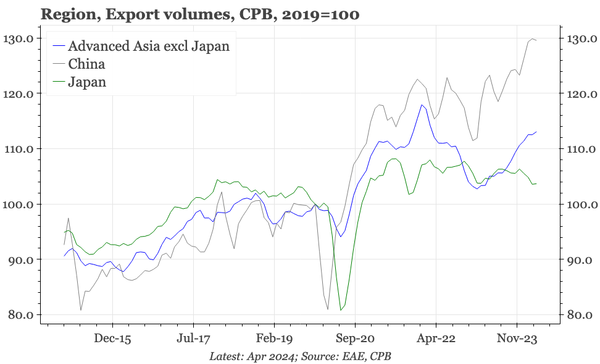

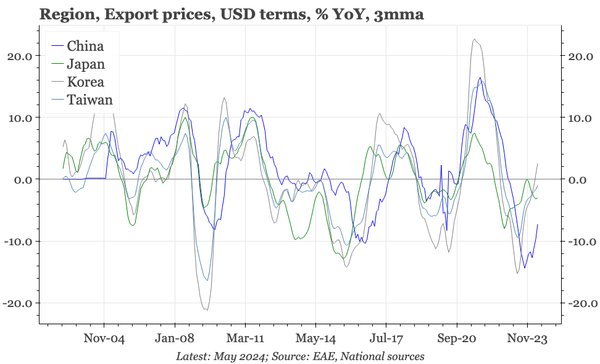

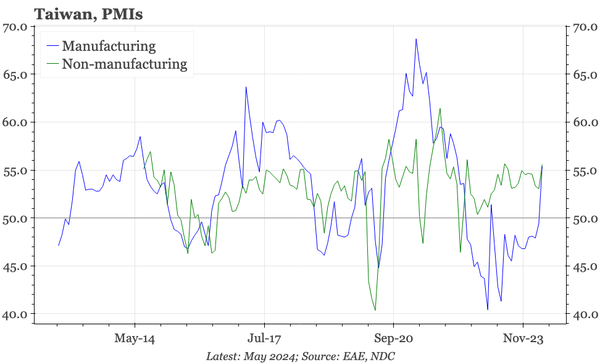

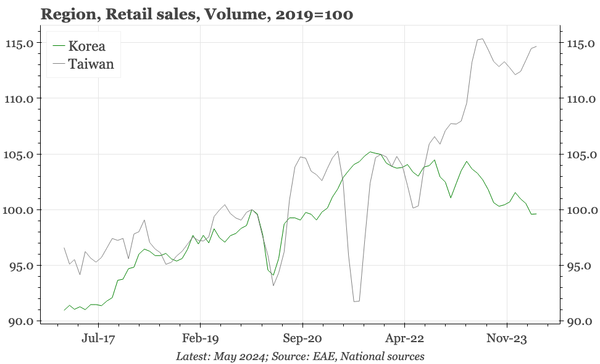

Export performance is the most obvious driver of Taiwan's outperformance relative to Korea since the pandemic, but the domestic story has been stronger too.