Public Post

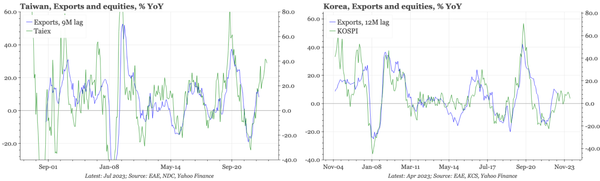

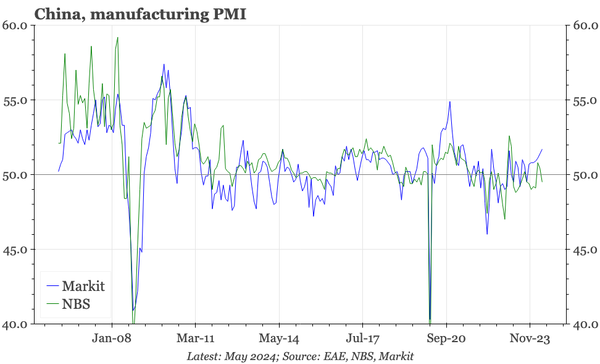

QTC: China – two-speed PMIs

With PMIs in TW and KR improving in May, the gap between the S&P and official mfg PMI is probably export-related. Still, the two PMIs do now give very different messages about the strength of the overall cycle.