Public Post

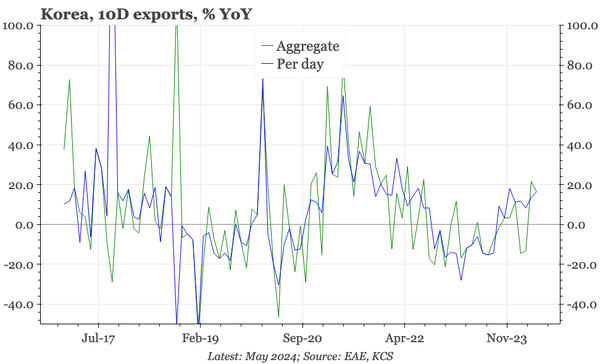

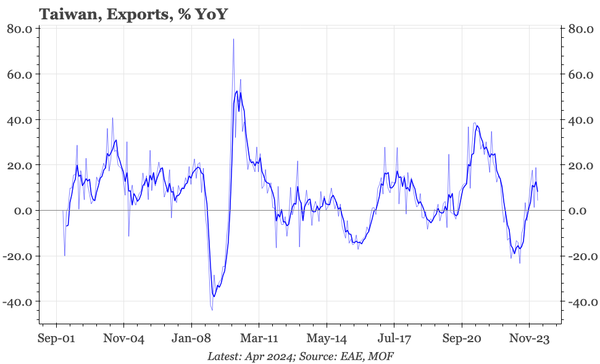

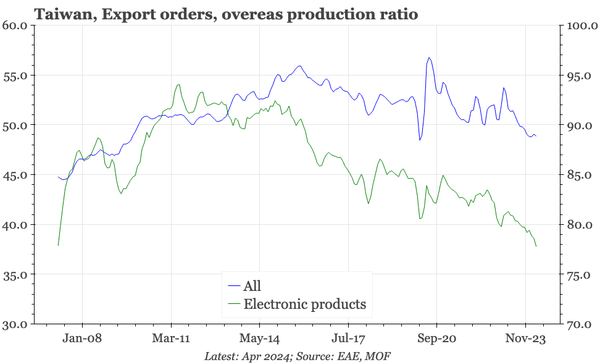

Taiwan – export orders also better

Export orders rose in April, but continue to trail actual exports. One reason could be supply-chain restructuring, shown by the fall in the overseas production ratio.