Public Post

Japan – cycle holding up, so far

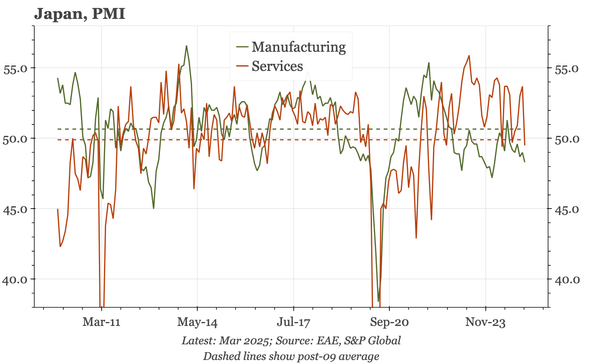

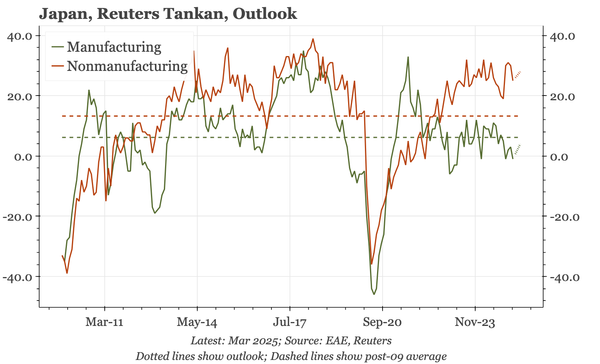

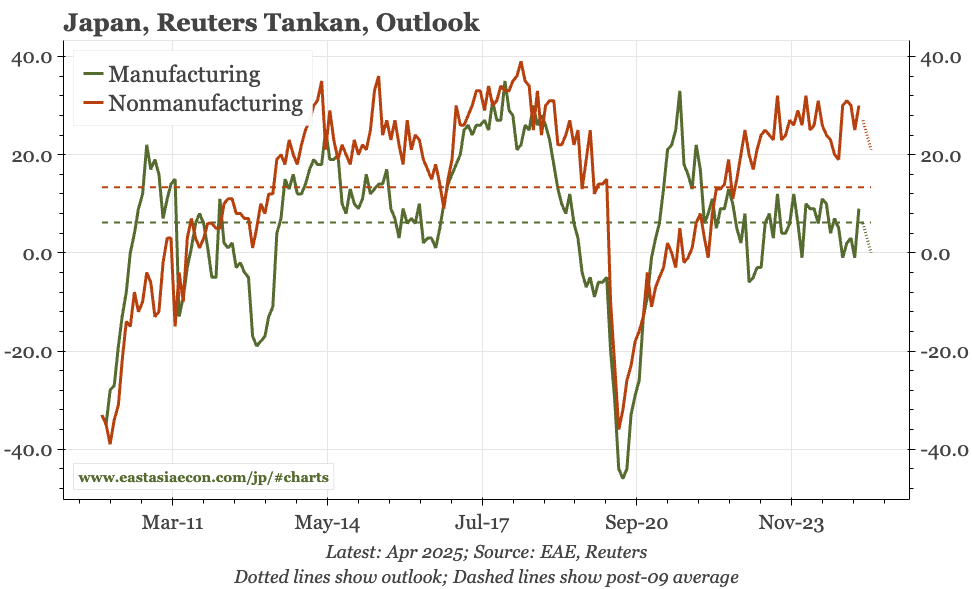

Bits and pieces today. Machine orders were stable in February. The April Reuters Tankan didn't show much deterioration, even though the survey was conducted after "Liberation Day". At least for services, one continued driver is tourism, with visitor numbers in Q1 surpassing 10m for the first time.