Subscribers Only

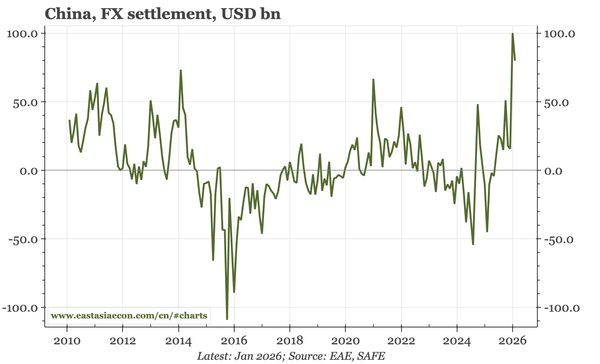

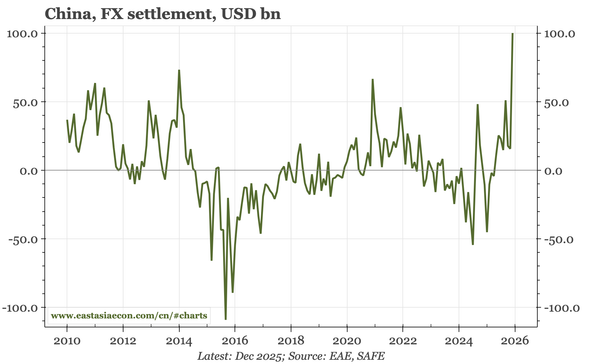

China – big inflows, sluggish domestic

January fx settlement data suggest large fx intervention for a second consecutive month. One reason is the CA surplus, which other data today show widened in Q4. Another is interest rates which are more stable, even though monetary trends aren't changing much, and property prices continue to fall.

Subscribers Only

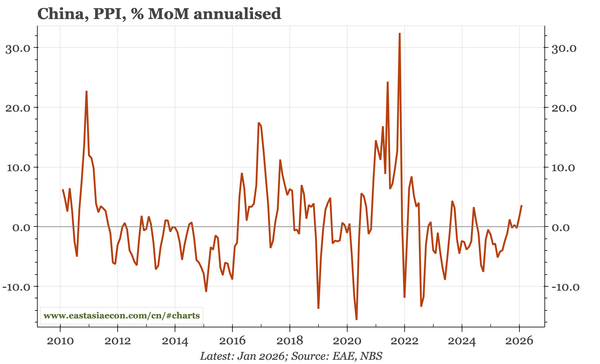

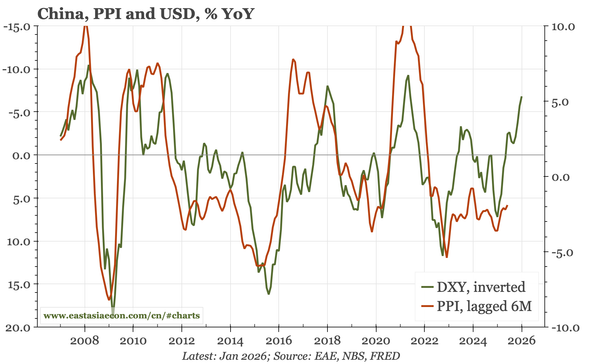

China – PPI up again

CPI inflation softened in January, but it always does when the new year holiday falls in February. PPI has less seasonal distortion, and rose MoM in January for the second consecutive time. The GDP deflator is likely to improve again in Q1. This is about external factors, but deflation is lessening.

Subscribers Only

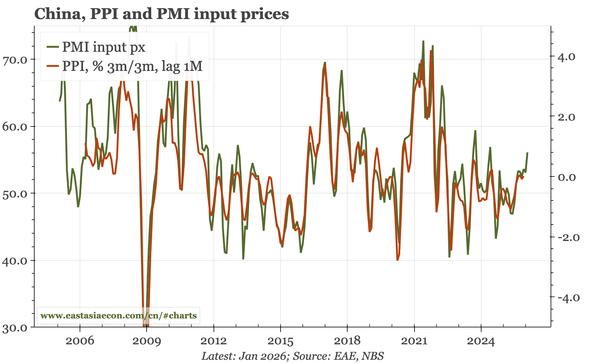

China – some nominal momentum

Today's official PMIs were below 50. That shows the domestic economy is weak – though the data were likely pulled down by the coming holiday. More interesting was the further rise in prices in manufacturing. That change relates to USD/global prices, but does suggest an upturn in nominal momentum.

Subscribers Only

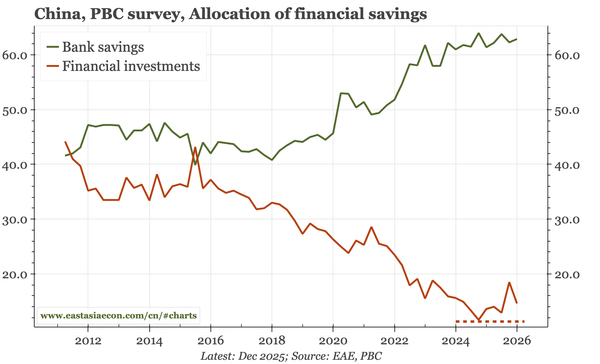

China – the end of the flight to safety

Like the actual monthly deposit data, Friday's PBC Q425 depositor survey shows a slowing of the flood of household savings into the safety of bank deposits. The structural deflation pressure caused by the collapse of real estate activity and the chaos of the covid lockdowns is beginning to ease.

Subscribers Only

China – nominal pick-up

Most important for markets is today's Q4 data is the pick-up in the deflator and nominal GDP, which external trends suggest can run further. In terms of the details, the data show two big discrepancies: collapsing FAI v industrial stability, and falling retail sales v rising consumption share of GDP

Subscribers Only

China – domestic so-so, external go-go

Some of the signs of domestic stabilisation I'd been tracking in 2025 faded into year-end. However, they didn't disappear entirely. China is also starting to benefit from the global tailwinds of weaker USD and rising commodity prices, creating upside risks for China's nominal cycle.

Subscribers Only

China – foreign flows stronger than domestic

China's release today of December data for money, credit and fx settlement tell three stories: domestic savings outflows have lost momentum, credit ex-government is looking a bit stronger, and capital inflows are really picking up. If right, the last dynamic is the most important for markets.

Subscribers Only

China – inflation up, for now

The second-derivative improvement in inflation is continuing, and should be seen in a better deflator when the Q4 GDP data are released later this month. However, there's not yet enough to think the trend can persist beyond Q126. One factor that could derail the improvement would be a stronger CNY.

Public Post

China – the case for a floor

My latest video, discussing the lessening of deflationary pressure, whether that can continue, and what the implications are for markets.

Subscribers Only

China

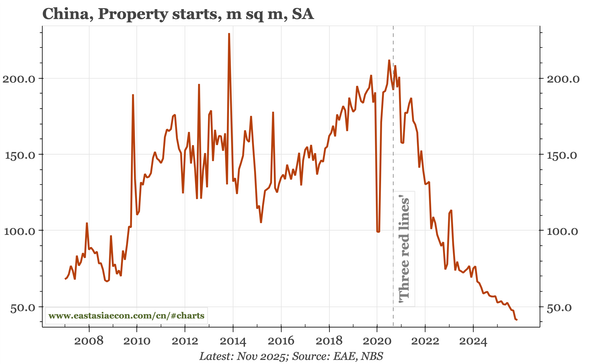

Like last month, November data show a contrast between real weakness in some areas of the economy (such as property, goods consumption) and more stability in others (pricing, output). Overall, however, the balance is once again shifting towards more weakness.

Subscribers Only

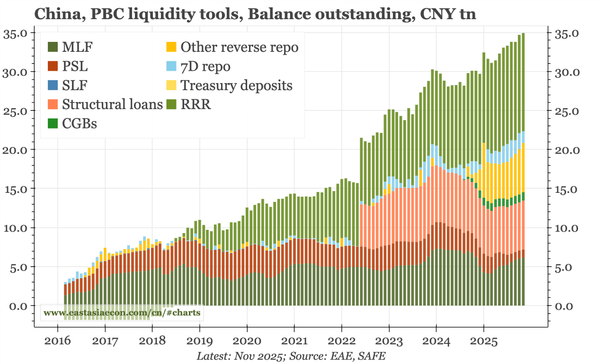

China – three positive monetary dynamics

Real economy developments still look negative for inflation. That the deflator nonetheless looks to be turning can be partly attributed to local food prices and global commodity prices. However, I think monetary factors are also playing a role, with three dynamics in particular worth highlighting.

Subscribers Only

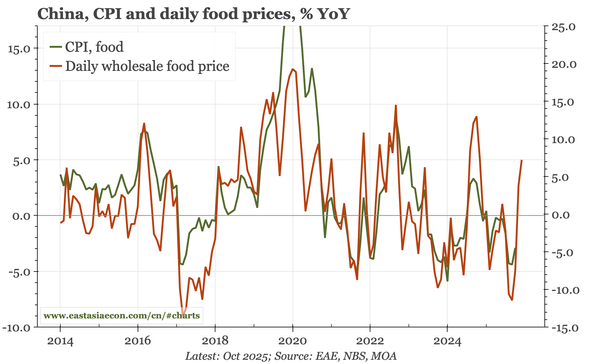

China – food prices lift CPI

Today's inflation data weren't surprising, with the big shift being food prices lifting CPI. Non-food prices aren't rising, but in level terms aren't falling either, which is an improvement from 1H25. Nominal growth should look better through Q126.

Subscribers Only

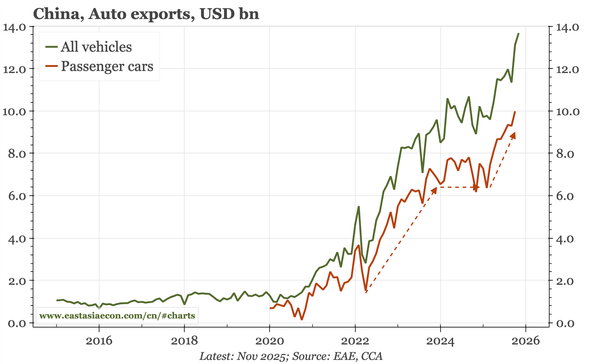

China – exports up again

The weakness in exports of October reversed in November, with a rebound in growth to ROW, and shipments to the US stabilising. Auto shipments reached a new all-time high, and are growing as quickly this year as in the initial take-off in 2023-24. Import demand declined, so the trade surplus rose.

Subscribers Only

China – lessening deflation

High-frequency data show upstream prices remained stable in November, while food prices have been rising. The combination points to a further lessening of headline deflation. I doubt that signals a real turn in nominal growth, though there are now some upside risks.

Subscribers Only

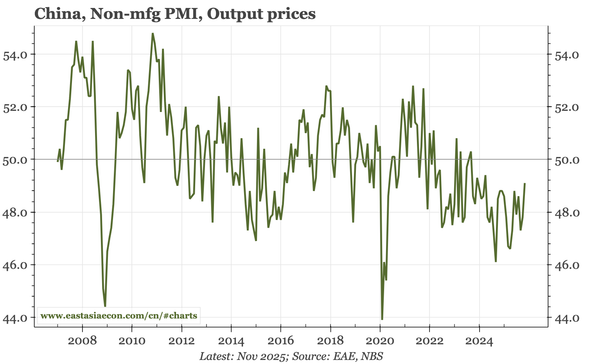

China – more data puzzles

The official composite output PMI in November fell below 50. That wasn't because of FAI: the industrial PMIs were stable. Rather, it was weakness in services. That is puzzling. For now, the one concrete indicator from today's inflation is actually positive: deflation isn't getting worse.