Public Post

China – is (it still possible) the worst is over?

My latest video, making the case for a bottoming of China's economy. In light of this week's poor official data, the argument might look off-base, which means it should at least be interesting. I do think the logic holds up, but as discussed here, there are reasons I could be wrong.

Subscribers Only

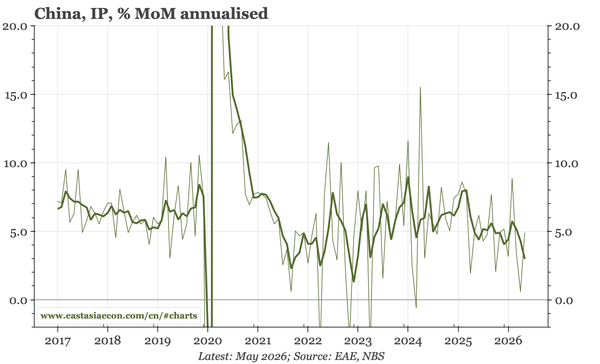

China – another month of weak data

I have been arguing that the underlying economy has been stabilising, with prices bottoming out before the Iran war. But stabilisation is external-led, and today's data show the domestic cycle remains a mess. That will likely become a policy issue if IP doesn't stay at an annualised run-rate of 5%

Subscribers Only

China – externally driven inflation

The rise in PPI that continued in May is of macro significance: it is pushing up industrial sector earnings, and the GDP deflator will likely turn positive in Q2. But it is difficult to find signs of domestically generated inflation that would suggest a real upturn in the economy.

Subscribers Only

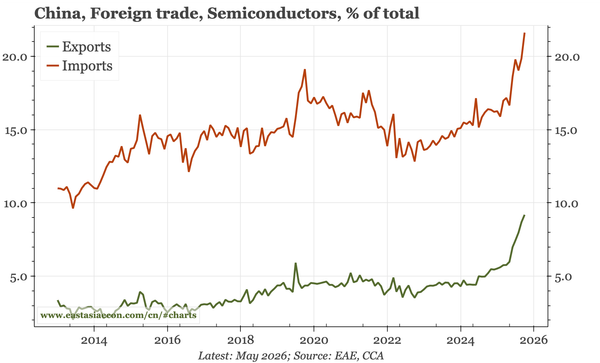

China – imports and exports strong in May

Chips rather than energy have been the bigger driver of trade patterns this year. That's true for exports and imports, though there are other drivers of both reaching record highs in May: autos for exports, ores and likely gold for imports. Despite the rise in imports, the trade surplus remains big.

Subscribers Only

China – no big change in PMIs

In today's official data, headline PMIs for both manufacturing and services remain around 50. The details of the manufacturing PMI don't suggest much Middle East disruption. The run-up in prices that pre-dated Iran is, however, sustaining. On the other hand, employment remains weak.

Subscribers Only

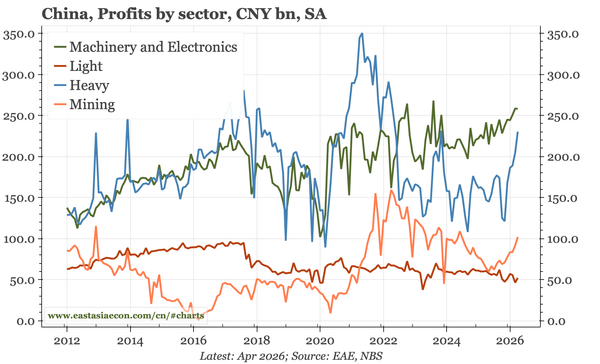

China – underlying profits a bit better

The bounce in headline profits in April was largely base effect, but there are signs of underlying improvement: revenues have started to rise, the increase in PPI is boosting profits in heavy industry, and hasn't yet derailed the post-2024 increase in total downstream manufacturing earnings.

Subscribers Only

China – consequences of the semi surge

The surge in semiconductor exports that is such an import theme across the region is also an important dynamic in China. But in China, the semiconductor trade has broader implications: for the trade surplus, import demand, the export outlook, and inflation, both in the region and ROW.

Subscribers Only

China – cycle weaker in April

Most of the headline activity data in April weakened, with goods retail sales being particularly bad. So, clearly no macro recovery. But services retail sales picked up, and the stability in home sales and household liquidity preference, and firmer pricing, continue to suggest broad stabilisation.

Subscribers Only

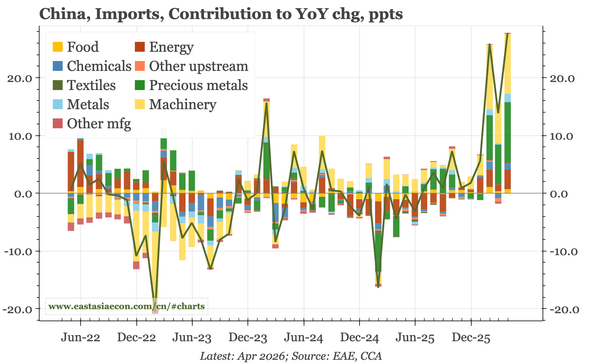

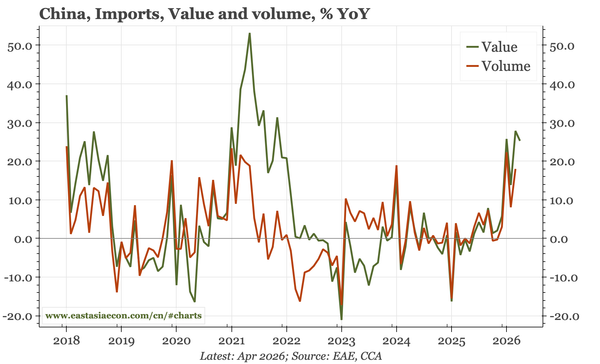

China – why are imports so strong?

The big trade story this year is the sudden rise in imports. There are some signs of firmer domestic demand. But 80% of the increase is from two categories alone: precious metals and semiconductors. And most of the semi strength is volumes, which is puzzling when global IC prices are rising so much.

Subscribers Only

China – inflation up again

PPI inflation accelerated again in April, and with CPI inflation firm, the GDP deflator is on track to rise in Q2 for the first time in 2022. The turn is being led by energy and commodity prices. There are some signs of a stabilisation in underlying prices too, but so far, they are tentative.

Subscribers Only

China – imports strong again

After doing nothing for 3 years, imports are suddenly growing 20%. Chips are one component, but while I thought that related to prices, official data show the bigger diver of overall imports is volumes. I am not sure that's because of domestic demand, but it is starting to reduce the trade surplus.

Subscribers Only

China – is the deflation crisis over?

The three red lines and covid delivered a huge, multi-year blow to the economy. Multiple signs have started to emerge that this hit has been absorbed, and that China macro is stabilising. This suggests that the recent lessening of deflation might prove durable, with broad implications across markets

Subscribers Only

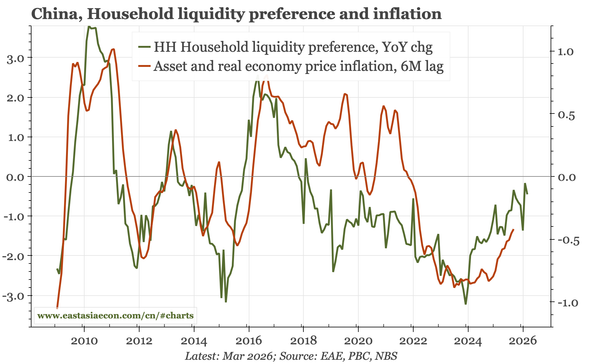

China – cycle stabilisation

The broad theme is macro is stabilisation, shown by three indicators that are bottoming after multi-year declines: property starts, household demand deposits, and producer prices. The implications, as are already being seen, are slower rate cuts, stabilising yields, and a stronger currency.

Subscribers Only

China – semiconductors boost imports

Today's trade data for March don't get us so far: only headline data have been released, and underlying trends are still obscured by Chinese New Year distortions. Overall, however, exports look firm, with auto sales rising again. Imports are very strong, but that is more about chips than energy.

Subscribers Only

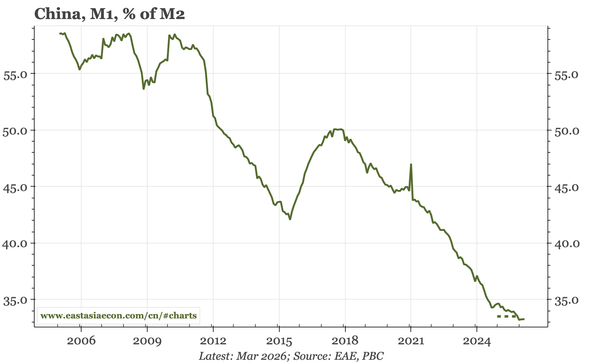

China – the monetary case for lessening deflation

The lessening of deflation has largely been driven by external factors. But domestic monetary developments have helped: the increase in PBC liquidity injections, and as shown again by today's March monetary release, the stabilisation of M1 growth and the M1:M2 ratio.