China - not a firm floor

The headline data were a bit stronger in August, but the details remain weak. It doesn't feel that the government is yet doing enough to really turn the economy around.

Official August activity data

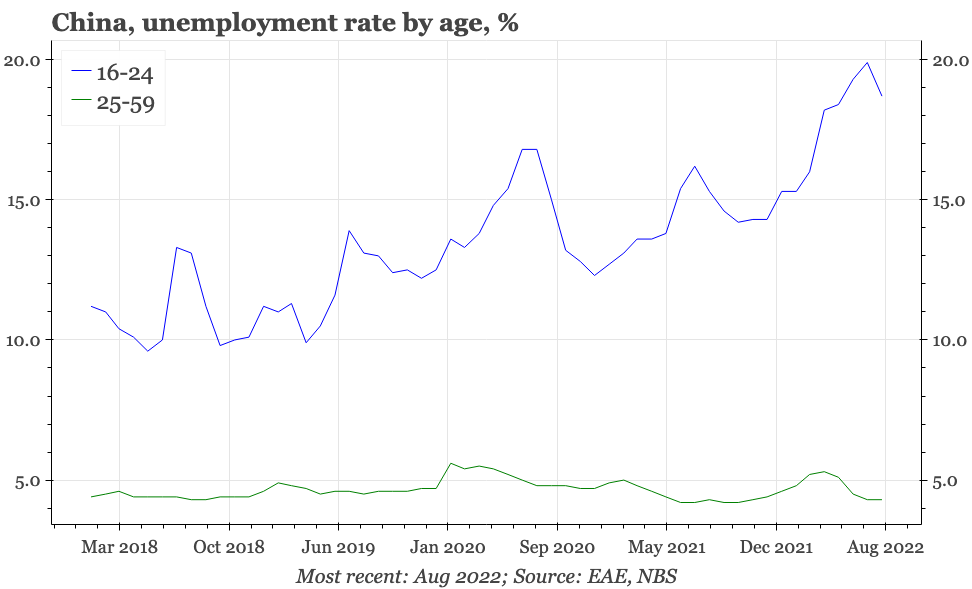

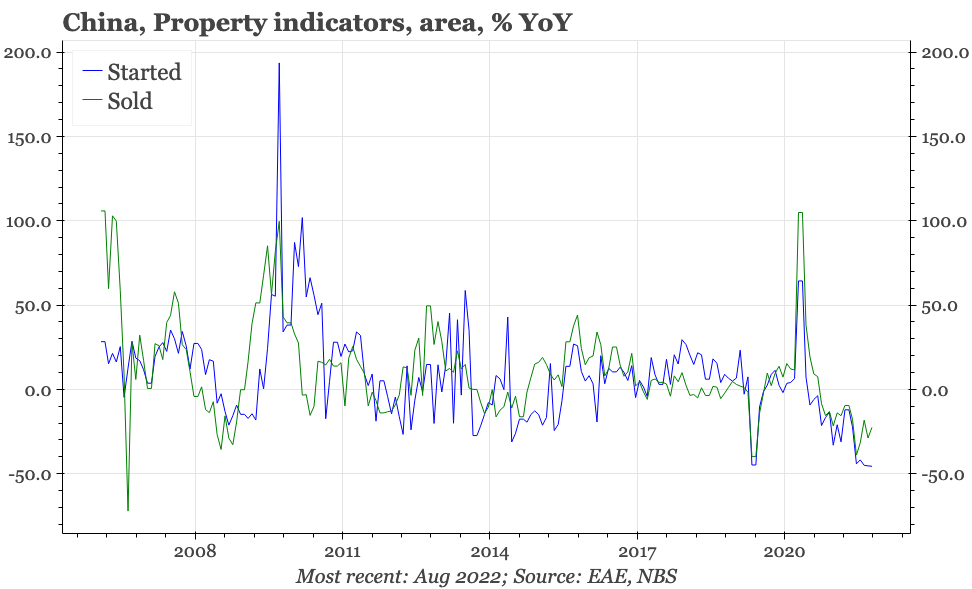

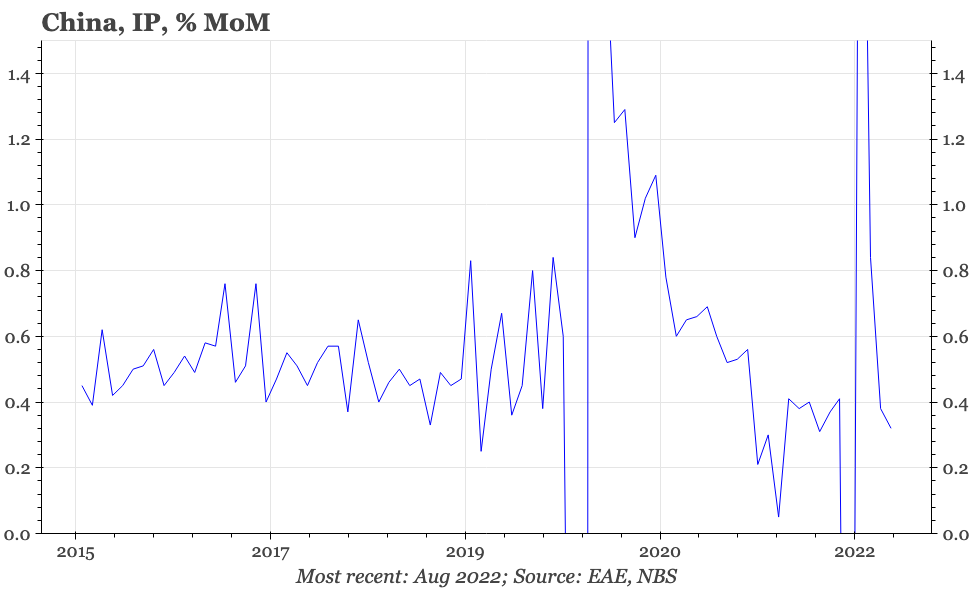

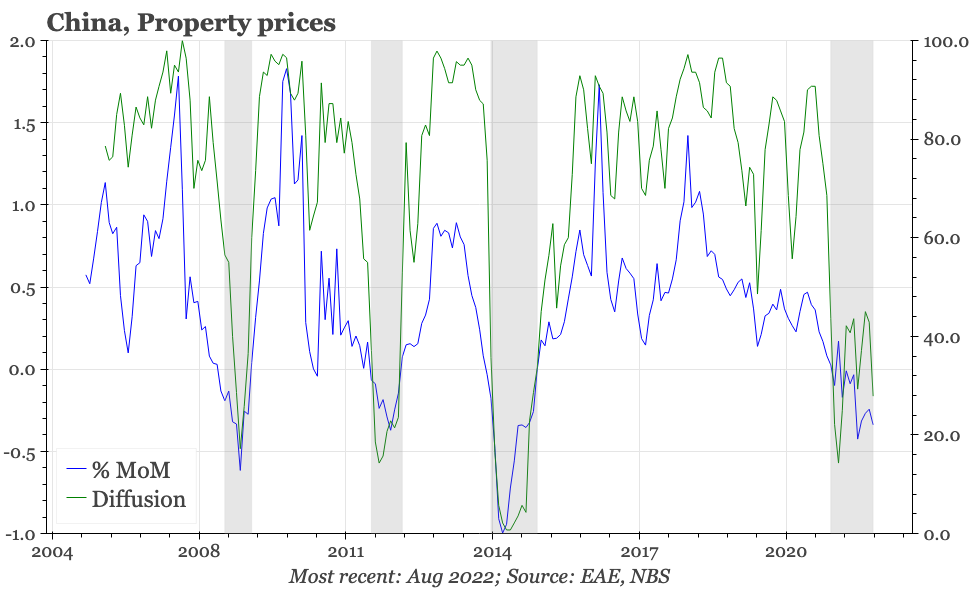

From the official data, it is possible to make an argument that the economy is bottoming out. In August unemployment fell for the fourth consecutive month, the YoY change in property sales and Industrial Production continued to recover from the April lows, and on the same annual basis Fixed Asset Investment growth edged higher for the first time this year.

Our tracker points to a rebound in GDP growth, albeit not yet above 5% YoY. It is also true that senior government officials are running around trying to ensure that the data continue to recover, with the latest initiative being this week's cut in deposit rates.

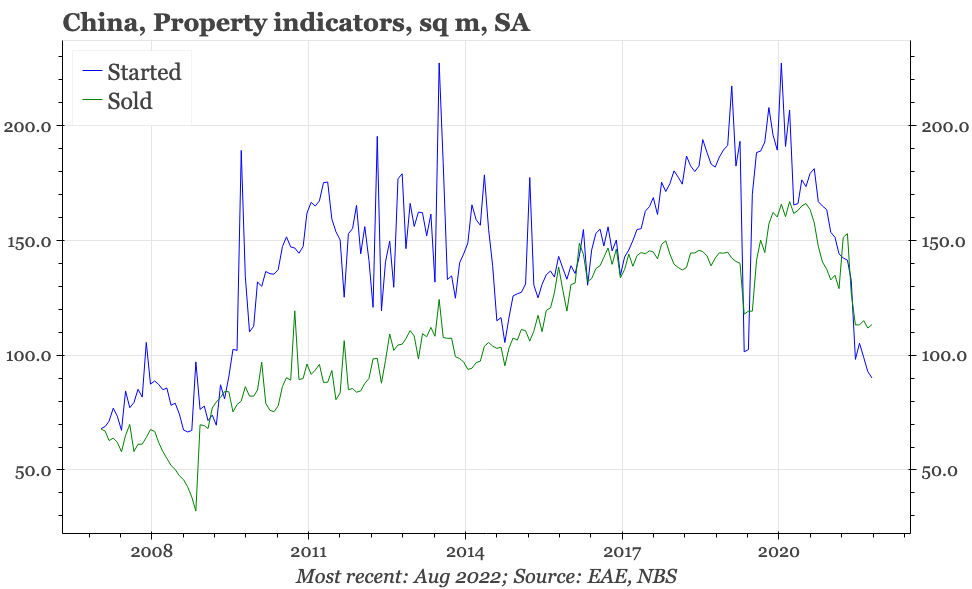

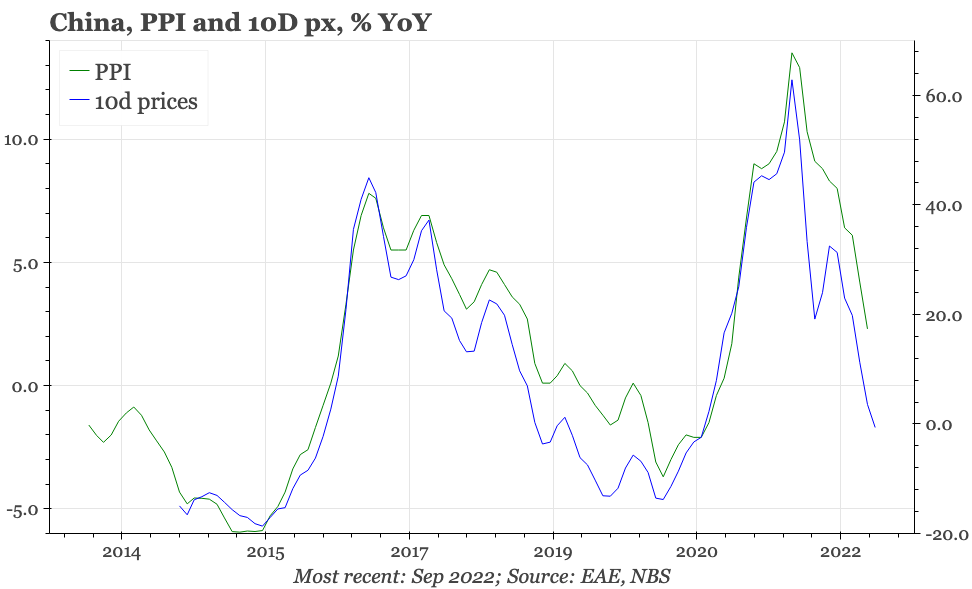

But if this is a floor in the domestic industrial cycle, it doesn't feel like a very firm one. In absolute terms, property starts fell to a new low in August, a development that will continue to spill over into overall construction for some months ahead, Property price deflation last month accelerated. On a MoM basis, IP slowed, and annualised sequential growth in FAI is running at less than 5%. Upstream prices so far through September are pointing to PPI inflation slowing again this month.

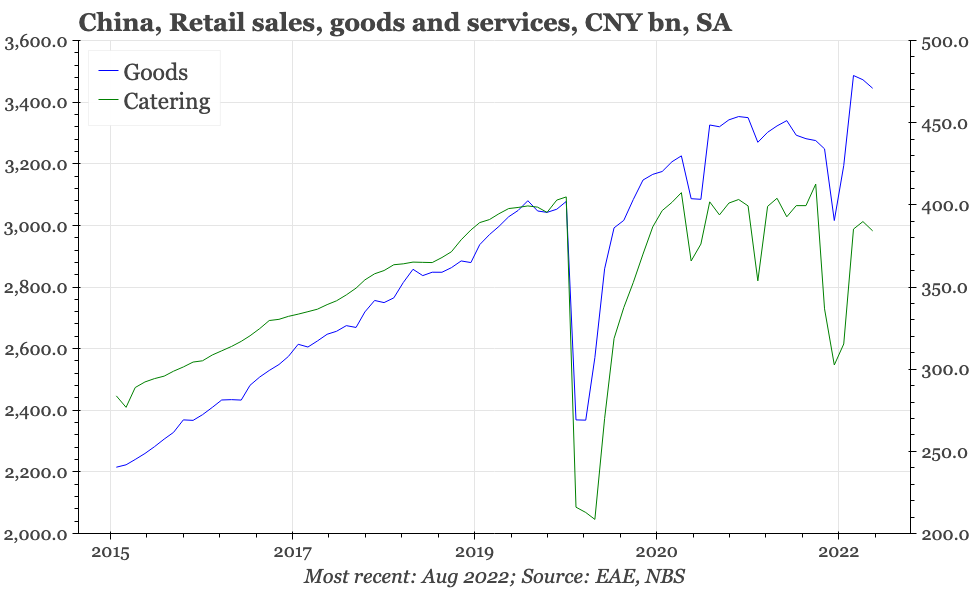

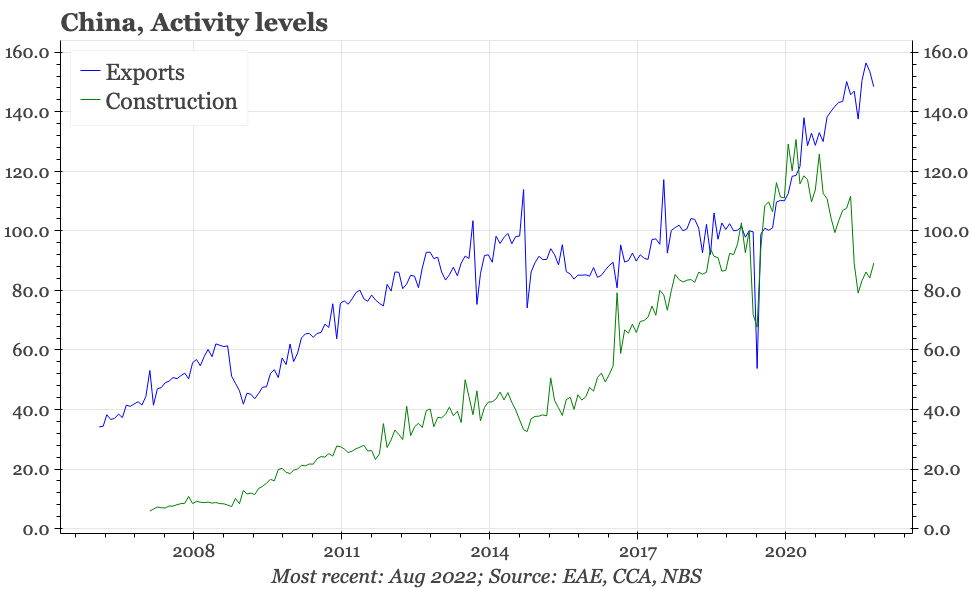

Our GDP tracker has bounced largely because of the jump in the services PMI, but retail sales momentum and Covid-19 lockdowns don't look supportive of that continuing. It also remains likely that exports, which through early 2022 supported growth as construction activity collapsed, are now starting to fade. Overall, there has been a recovery in the national economy out of the Shanghai lockdown, but given all the headwinds, it doesn't feel that the government has yet done enough to really turn the economy around.