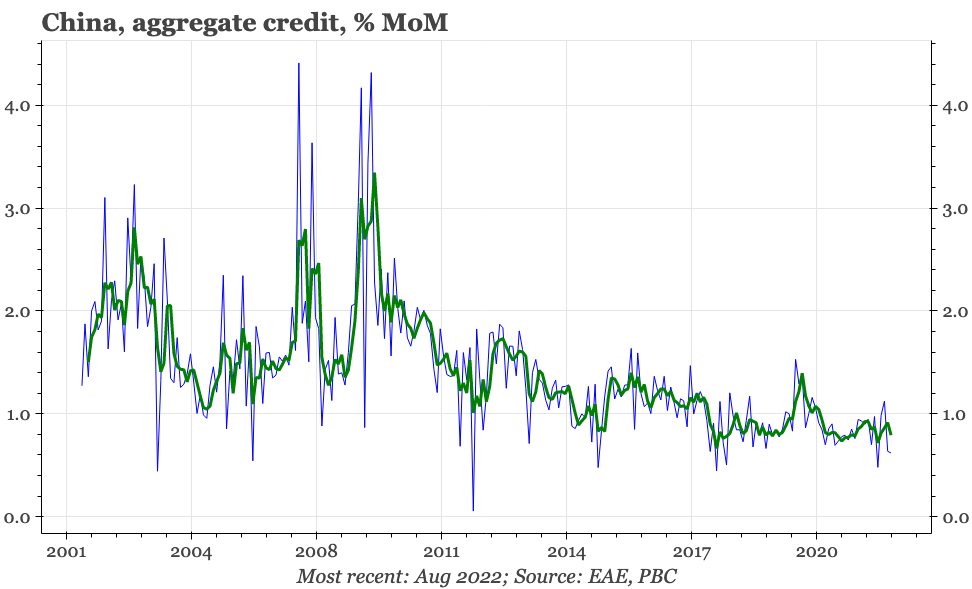

China - August credit data

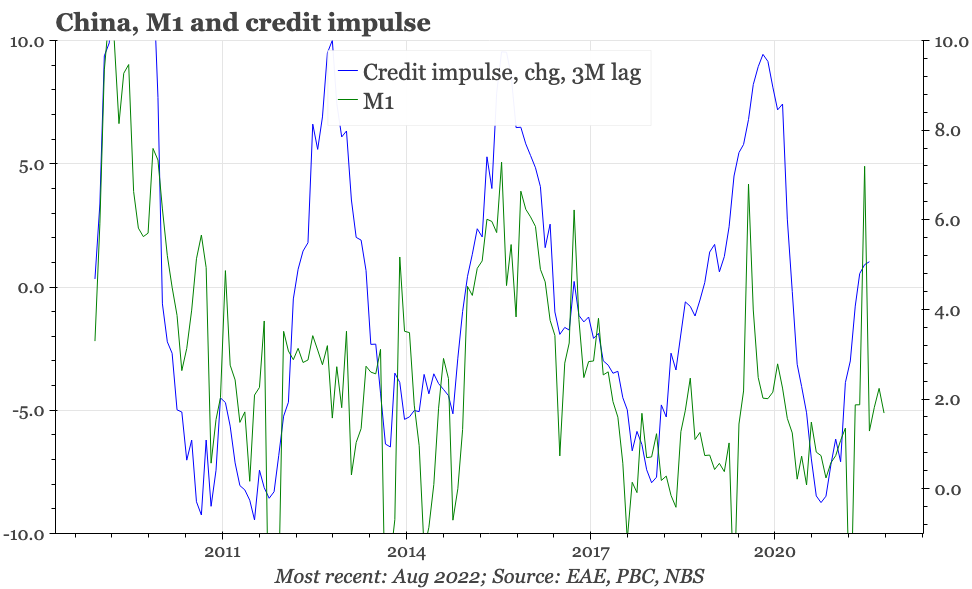

Monetary data in August remained weak, with little reason to suggest any upturn in the macro cycle.

China's economy might be going through the same sort of lockdown stress experienced in 2020, but there is nothing like the policy support that was offered then. Two years ago, credit growth accelerated above 1% MoM for around six months. This time, the pick-up lasted for just two months, and after starting to fade in July, credit growth slowed again in August.

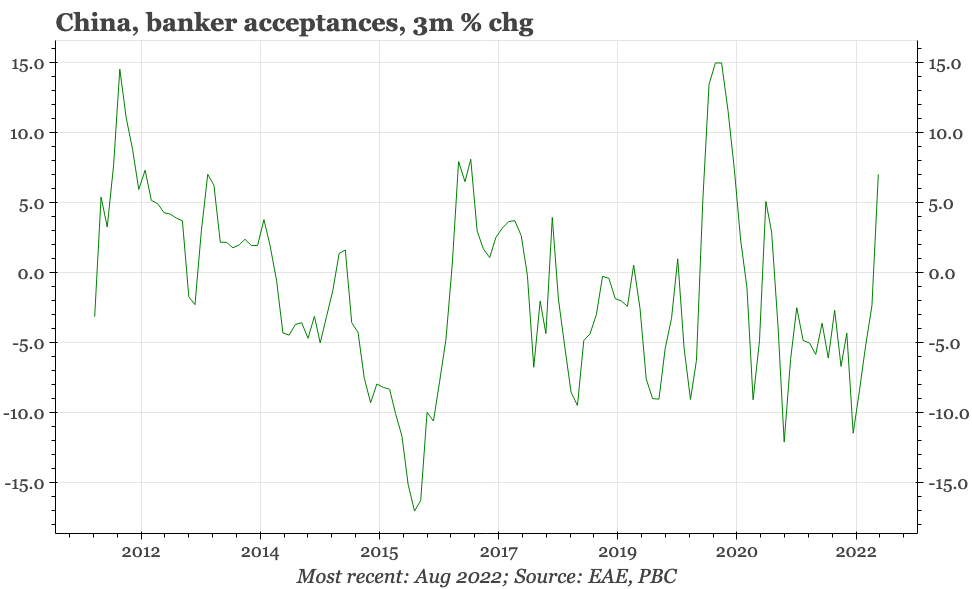

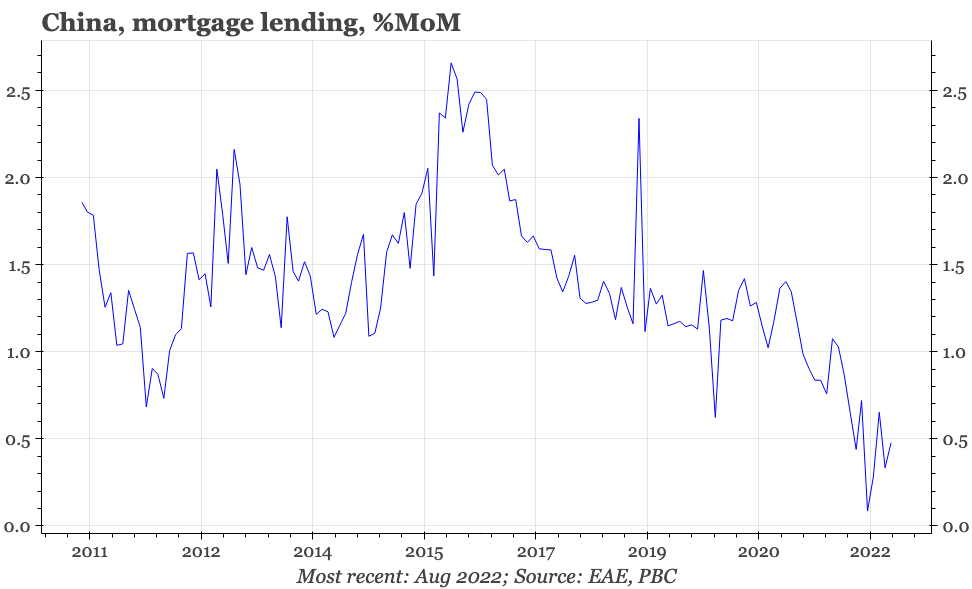

Most of the details last month were also weak. Credit growth would have been lower still had it not been for a bounce in banker acceptances. That is often seen at the beginnings of credit upturns, but also tends to occur when banks are struggling to reach lending targets through more traditional channels. M1 growth slowed again in August, pointing to a lacklustre credit impulse going forward. According to the data available so far, corporates continued to put more money into time deposits, which points to rising real interest rates and capex caution. In terms of household borrowing, mortgage growth remained weak.

There were two details to offset mildly the overall negative tone. Shadow banking loans did show stronger momentum, which perhaps shows some liberalisation of credit towards property developers. And while our rough calculation suggests the credit impulse fell, that could be revised up depending just how bad nominal GDP growth is in Q3.

An upwards revision in the credit impulse has a flipside: leverage in the economy, which policymakers had been intent on controlling, is rising once again. For now, then, the economy seems stuck in the worst of two worlds. Stimulus in ineffective, leaving the cycle weak, while debt is rising, creating a worsening structural story.

More charts can be seen here (they take a few seconds to load)