China – is that it for deflation?

In October, headline PPI fell back into deflation, and CPI inflation eased quite sharply too. But there are signs that China is nearer the end of this deflation shock than the beginning.

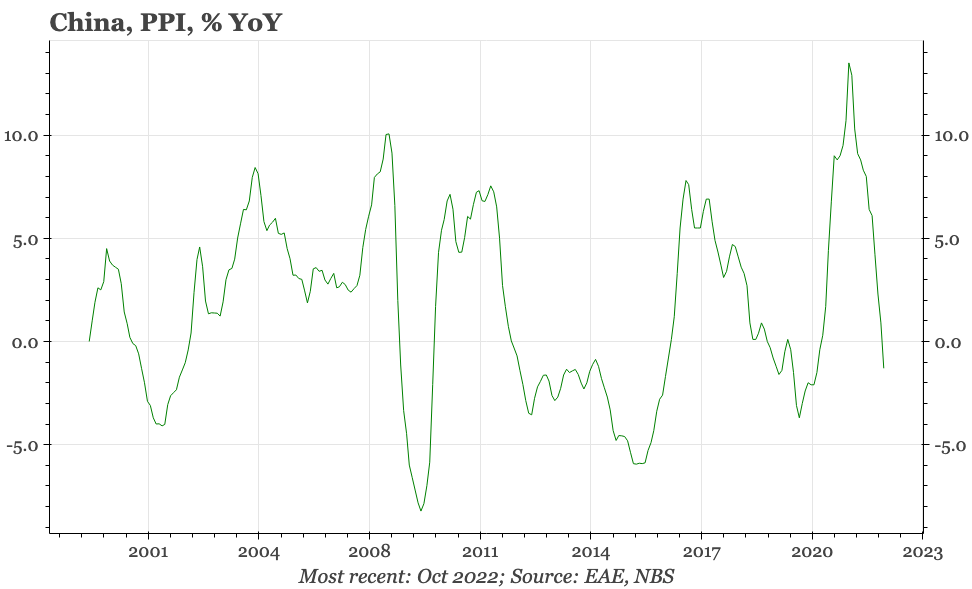

October PPI and CPI

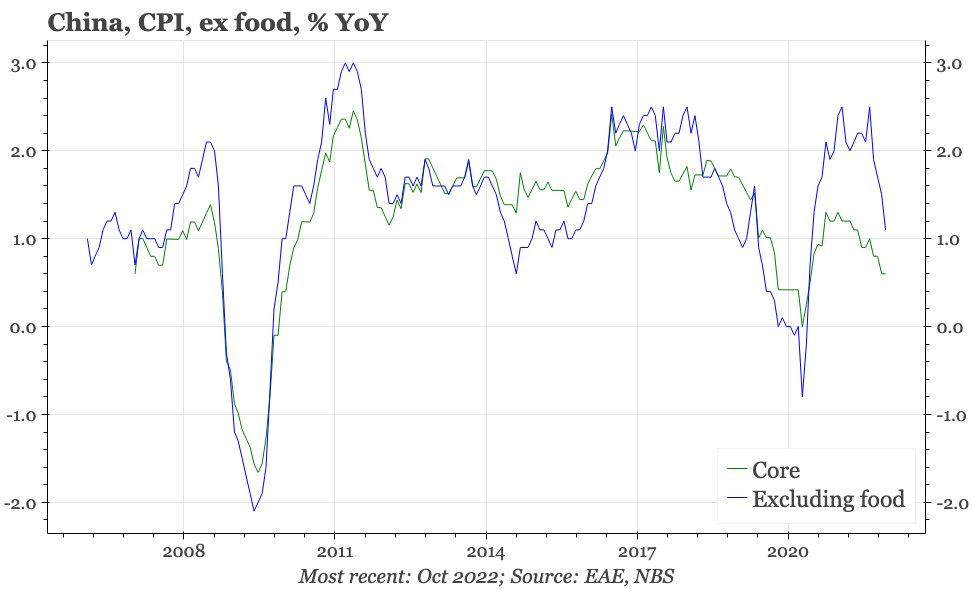

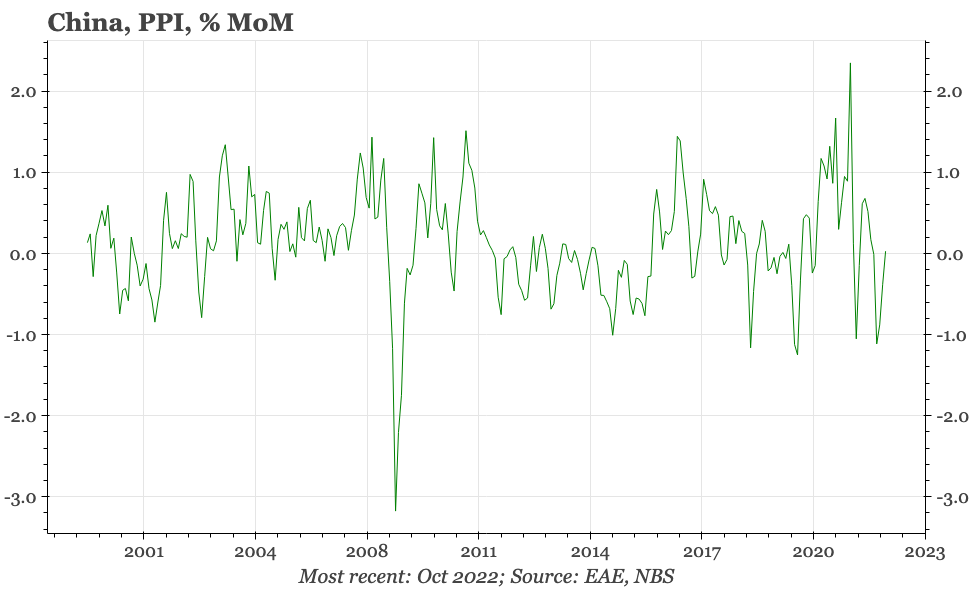

On a MoM basis, China has been in deflation for a while. For PPI, that phenomenon is now showing up in the headline YoY data, which in October was down -1.3%. Core CPI has been falling MoM too, and although it picked up a touch in October, overall CPI inflation fell back from 2.8% YoY to 2.1%, as both food and energy prices rose less quickly.

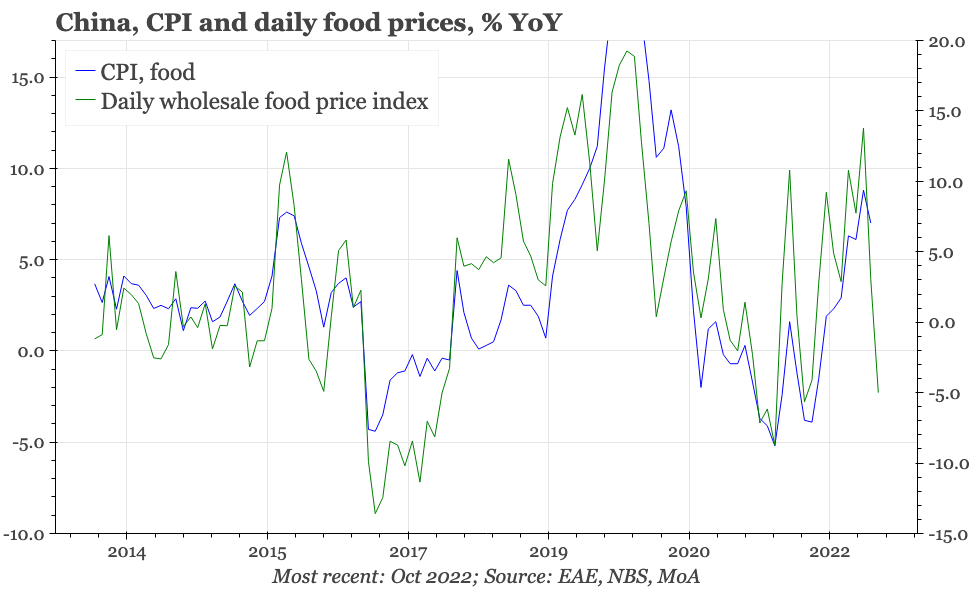

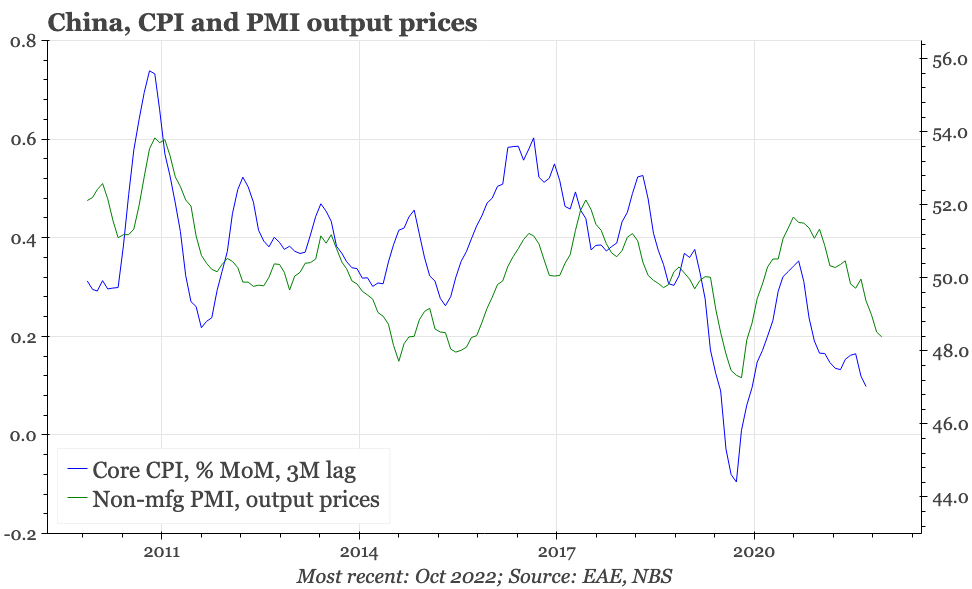

Leading indicators for the short-term are mostly all pointing down. PPI deflation should deepen, and core inflation should ease further, too. It is looking in November that food and energy price inflation will soften as well, though with these, there is a bit more uncertainty.

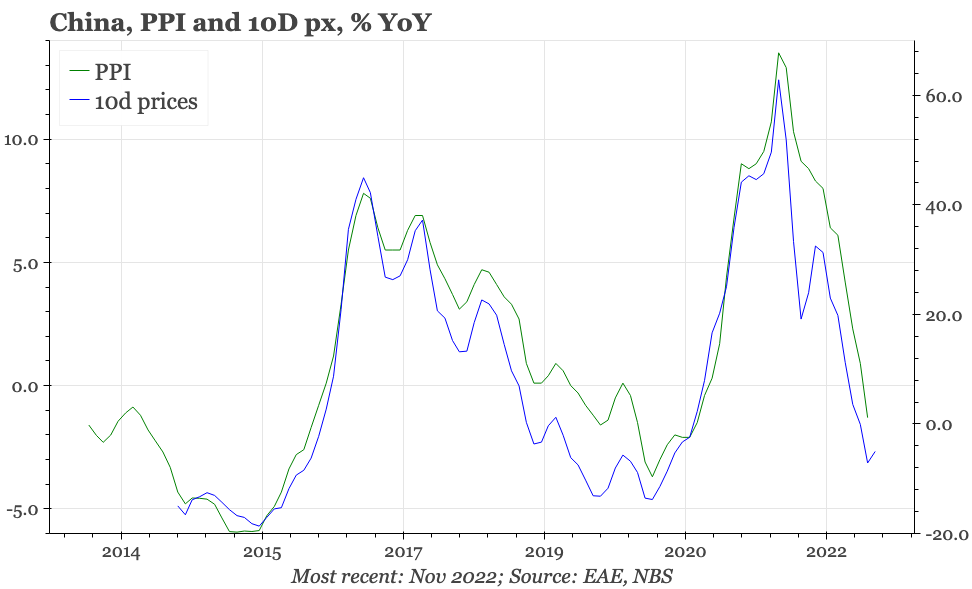

Media, and perhaps the market, will likely all be full of commentary about deflation in China. But there are actually some signs that China is nearer the end than the beginning of this negative price shock. On a MoM basis, PPI deflation bottomed out in July. The NBS's series of upstream prices, published every ten days, has started to turn up on a YoY basis. The same is tentatively true of the USD and Chinese construction activity.

This is all linked with signs that the industrial economy could be bottoming out. So for price momentum to strengthen, this cyclical recovery needs to be validated and gain momentum. Until that happens, it is unlikely that there will be a shift away from the current easy monetary policy.