China – May credit data

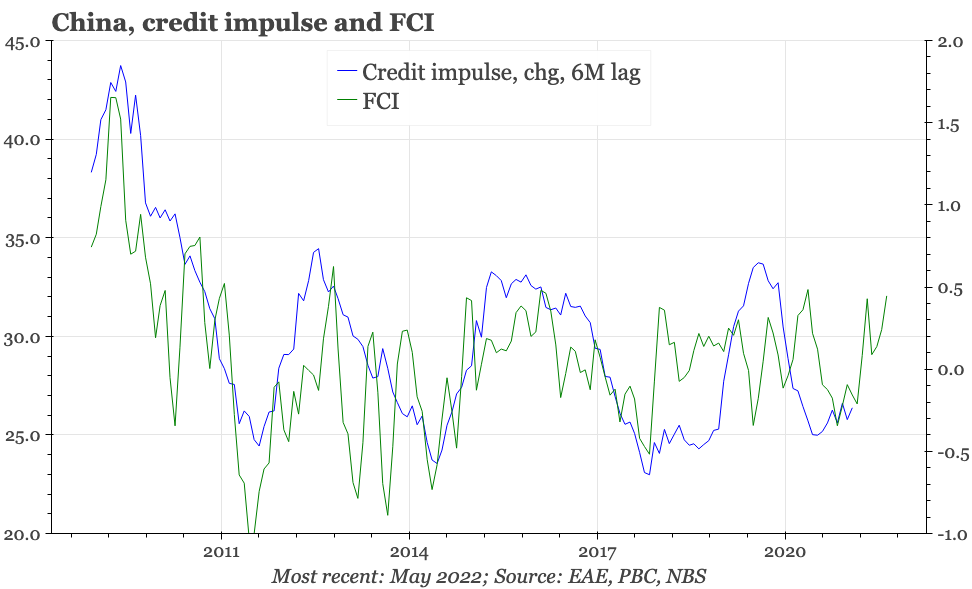

Just as the overall sentiment has passed through peak pessimism, so the credit cycle has lifted from the trough. But the credit data in May were mixed, and absent the emergence of a significant source of demand, the upside for credit is likely limited.

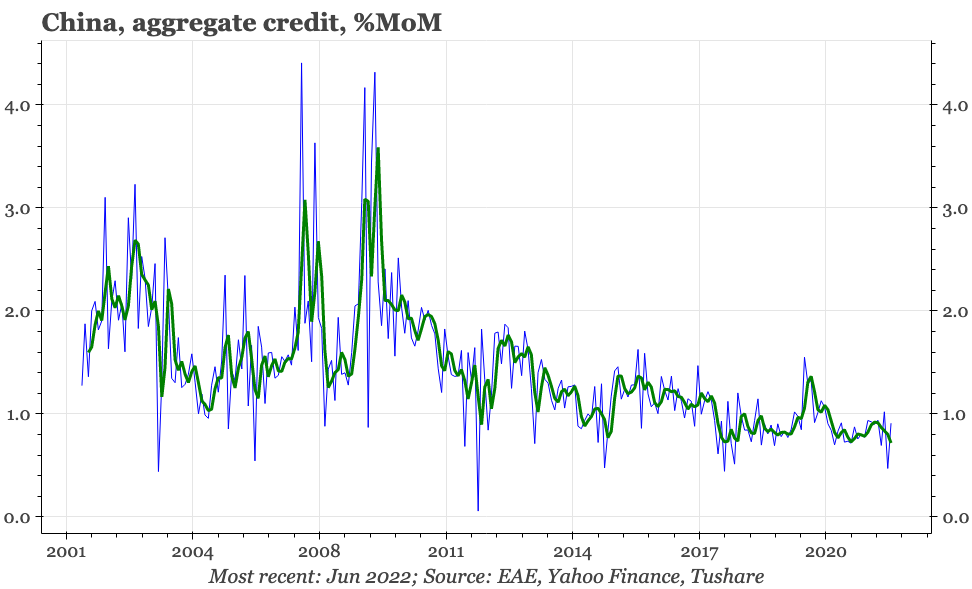

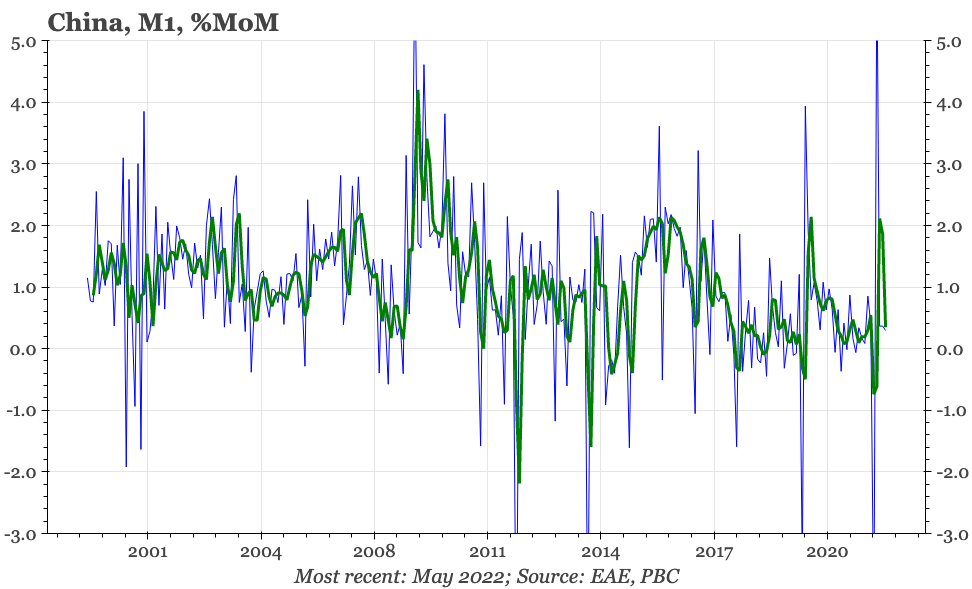

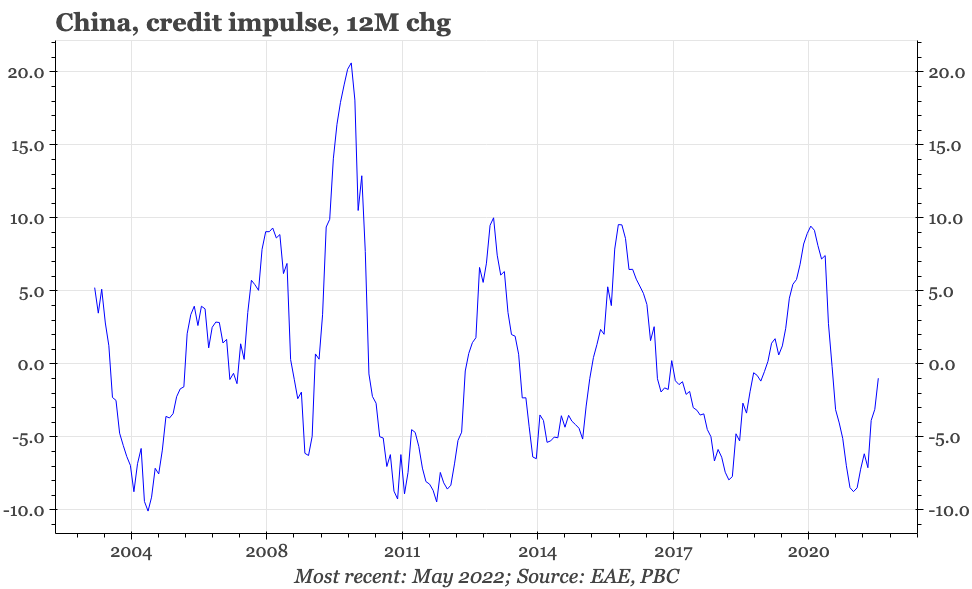

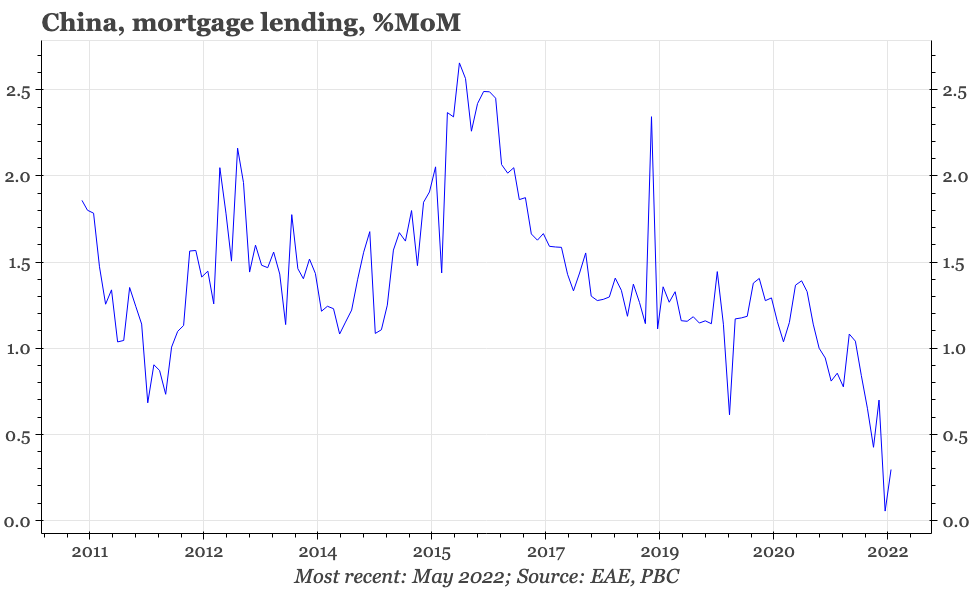

The credit and monetary data in May were mixed. Credit growth reversed the slump of April, although not by enough to cause a bounce in the downwards trend of the last three months; the credit impulse rebounded, but the April surge in M1 fell back; mortgage lending growth remains close to record lows, despite a tick up last month.

Probably, this mixed picture should be expected, given the cross-currents in the economy and policy. Activity data in May were still feeble, with the economy likely still contracting. Clearly, that wouldn't have been good for credit demand, though interest rates also fell, which might have incentivised some borrowers to seek new loans. The weak economy would also have put off some lenders from issuing new credit, but at the same time the government has been putting a lot of pressure on banks in particular to act counter-cyclically.

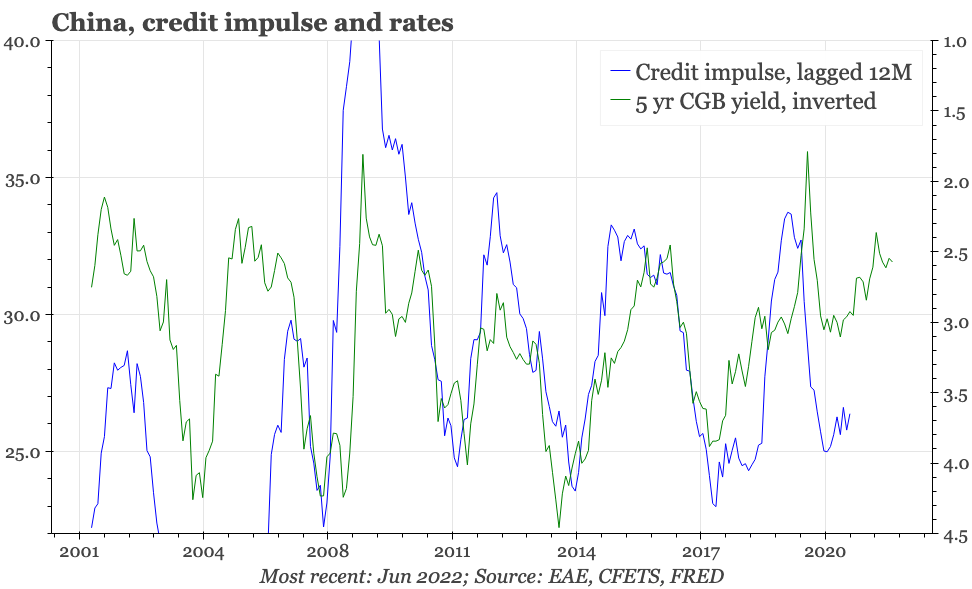

As long as Covid-19 restrictions ease further, then credit growth should lift more from here, boosted by a better alignment of economic activity and policy. There's a few indications that the bounce in credit could actually be quite big, given the low level of interest rates and the looseness of FCI. However, it seems unlikely such a significant rise in the credit impulse materialises without a clearer sign of recovery in end-user demand, in the form of property, infrastructure, exports, or consumption.