China - credit better than the headlines

The monetary data aren't bullish, but are more constructive than the headlines suggest. That's because credit growth outside of government borrowing is rising. This keeps alive the possibility that China is through the worst, though such an interpretation is a stretch as long as M1 growth is weak.

October credit data

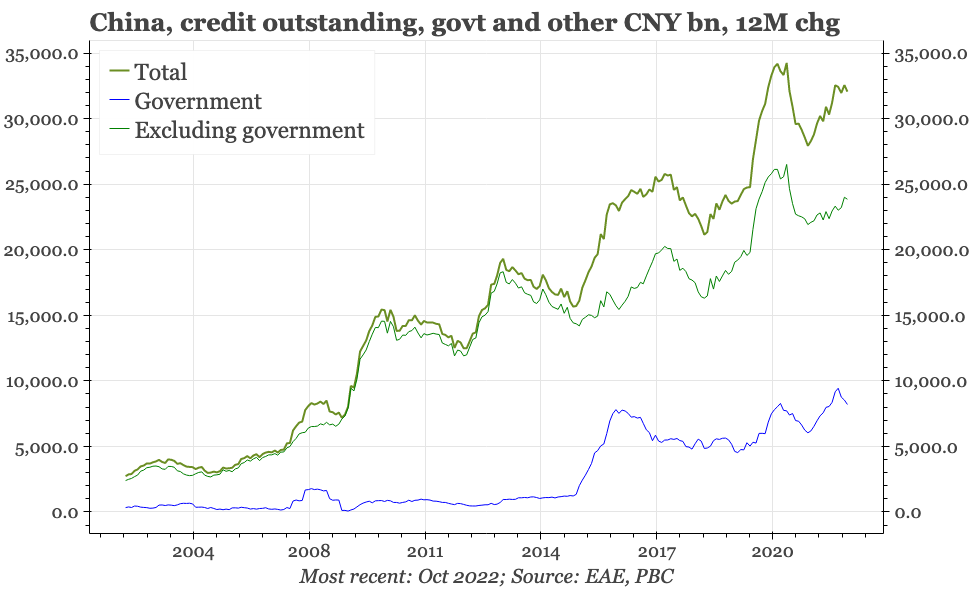

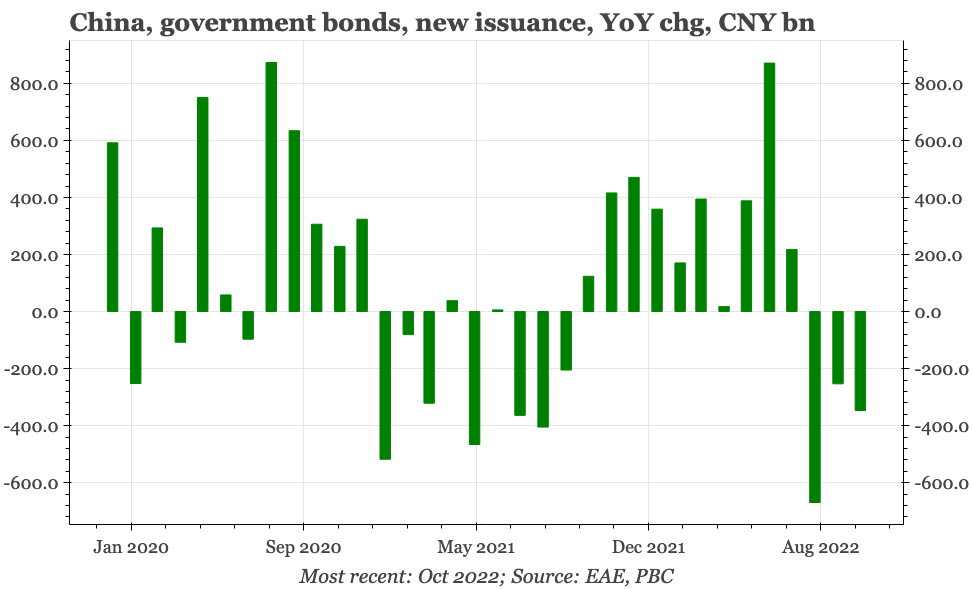

On a headline basis, money and credit growth was again soft in October. Indeed, in absolute terms, the rise in total credit that began in October 2021 peaked out in back in June, and doesn't show sign of rising again. The reason is government bond issuance, particularly local government special bonds. The annual quota for selling those was front-loaded in 2020 to get the economy going after the covid-induced sudden stop in the first quarter; was delayed to later in the year when the economy was doing well in 2021; and was again concentrated in the early months of 2022 as the economy once again fell into trouble. So, the peak is issuance this year is now in the past, and the fall-off is weighing on aggregate credit growth.

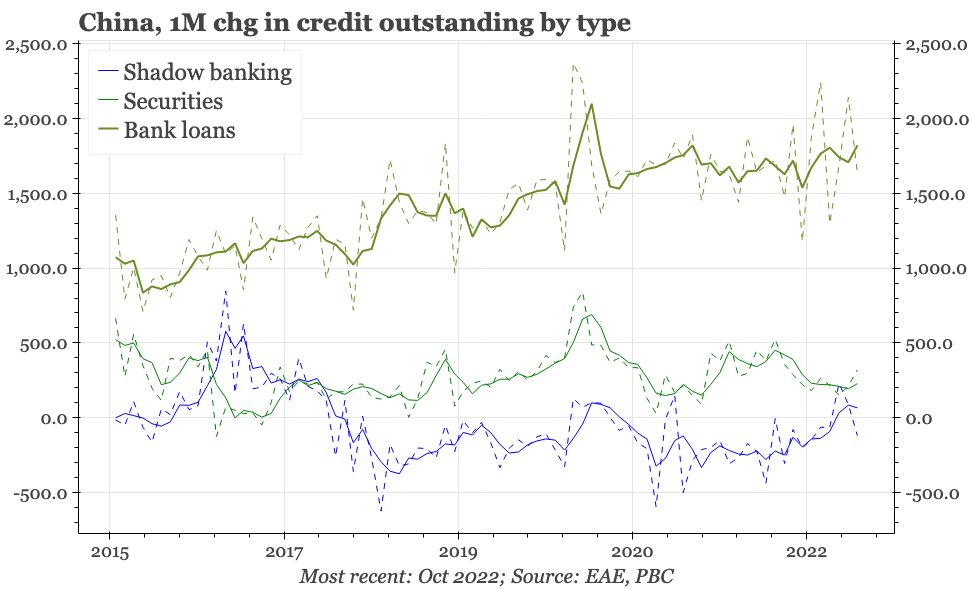

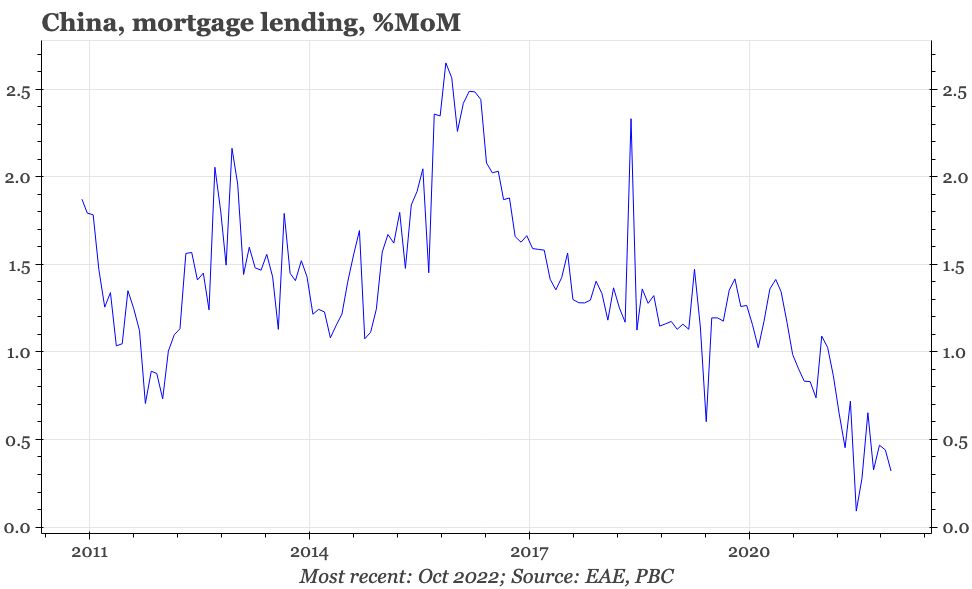

Outside of government issuance, though, the upturn in credit momentum that started in late 2021 appears to remain intact. Traditional loan growth is volatile from month to month, but the mild step-up from the end of Q2 this year has been retained. Shadow banking is also contracting less quickly than it had been. Mortgage lending slowed again in October, but not by enough to totally negate the bottoming out that appeared to be going on through the summer.

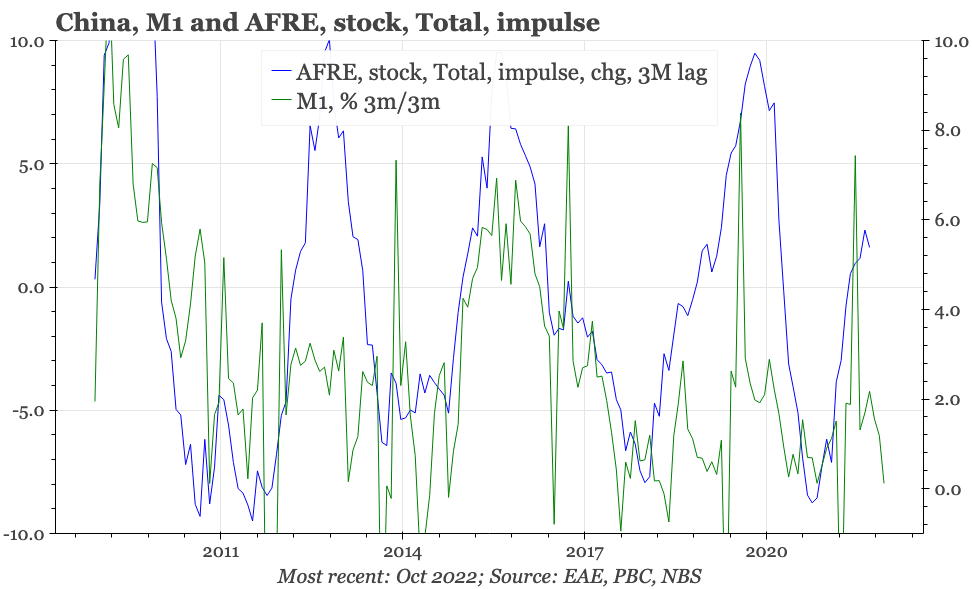

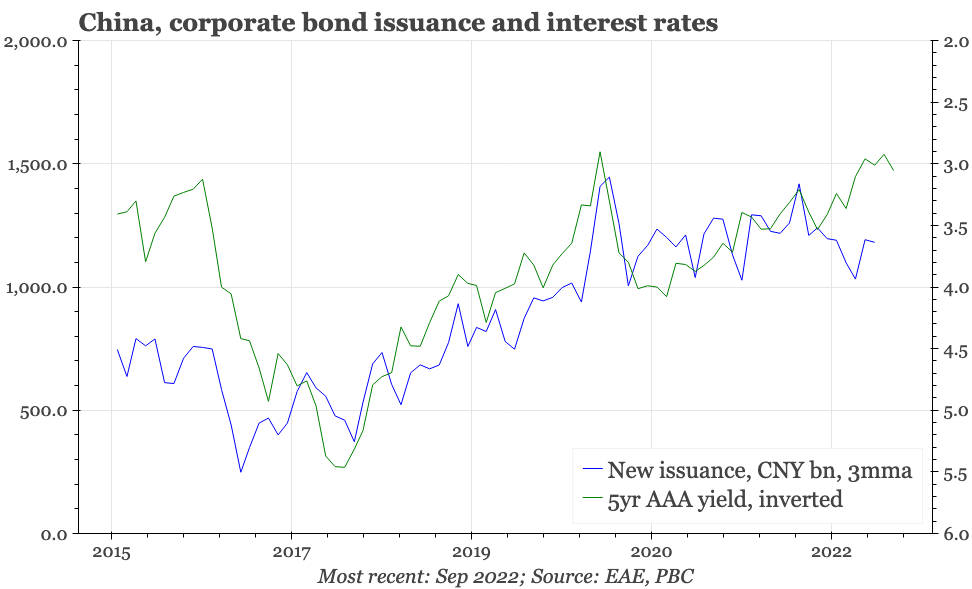

These indicators are important, but only suggest at best that the cycle could be bottoming. To have more conviction about that, and certainly to think China's cycle and financial system are clearly through the worst, other details need to start moving up. Sequential momentum in M1 seems to have stalled again, which matters because that is usually an indicator that the overall credit impulse is about to fall. Given that decline in M1, it perhaps isn't surprising that the preliminary cut of the data suggests companies are continuing to move money into time deposits, which again, isn't a sign of bullishness. Corporate bond issuance also looks soft relative to the low level of rates.