China – weaker again

The PMIs suggest renewed weakening of the economy in November. That perhaps explains the accelerated pace of property easing. That loosening is an important development, but as long as China remains mired in covid difficulties, the outlook for the economy will remain very difficult.

Official November PMIs

The weakness in the official services PMI in November isn't at all surprising, given the continued covid chaos. And given that chaos is continuing, there is little reason to expect meaningful improvement either in December, or probably through Q1.

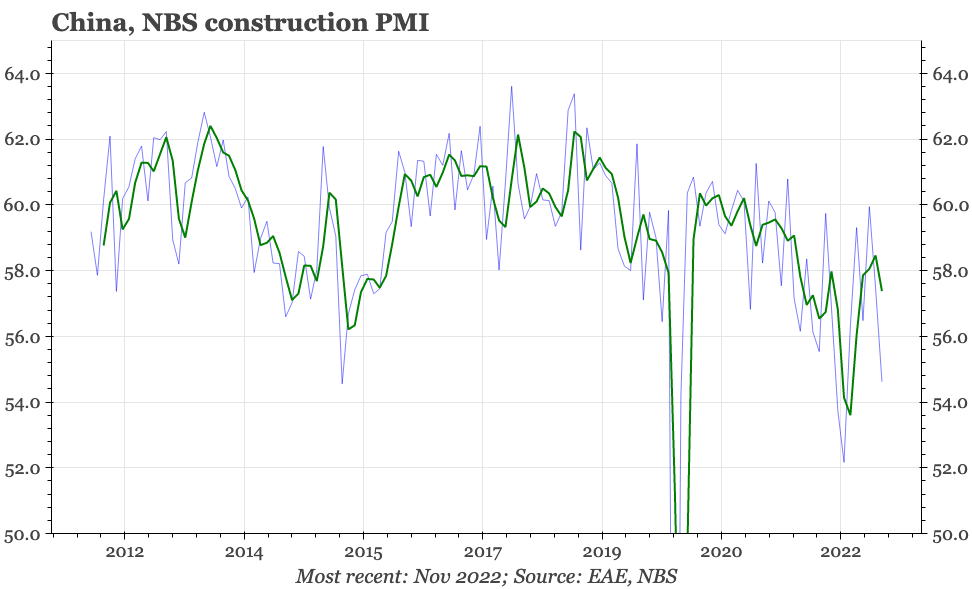

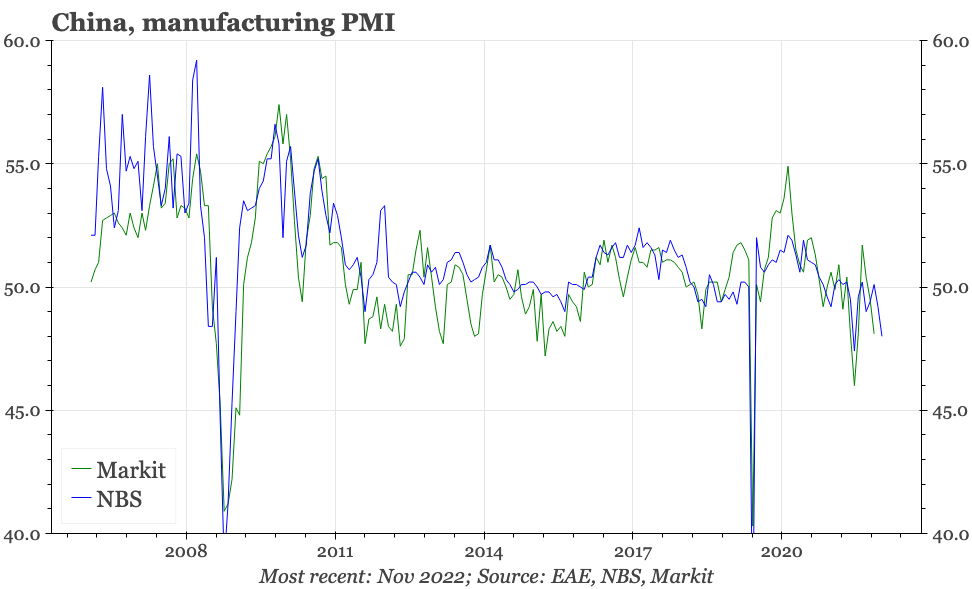

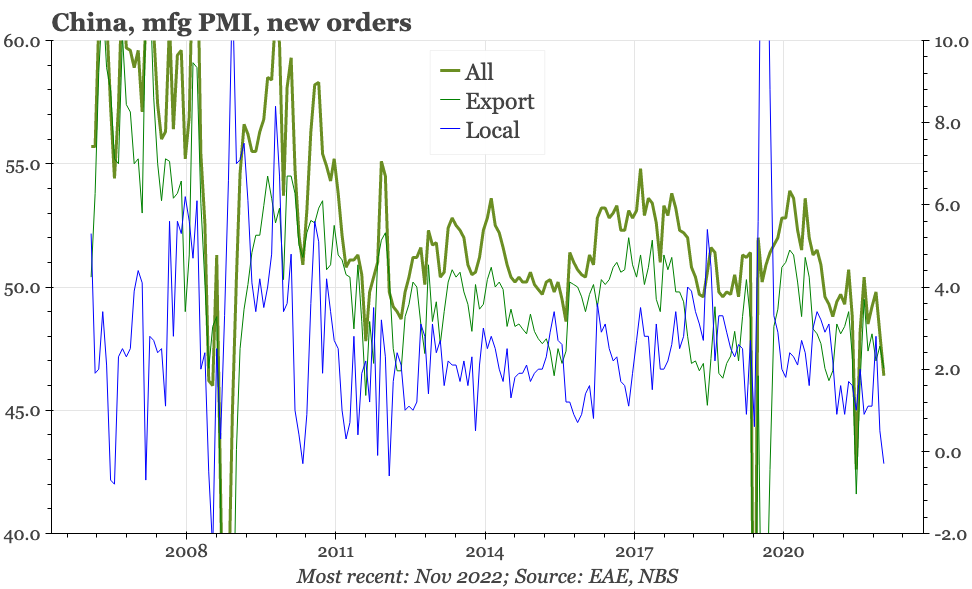

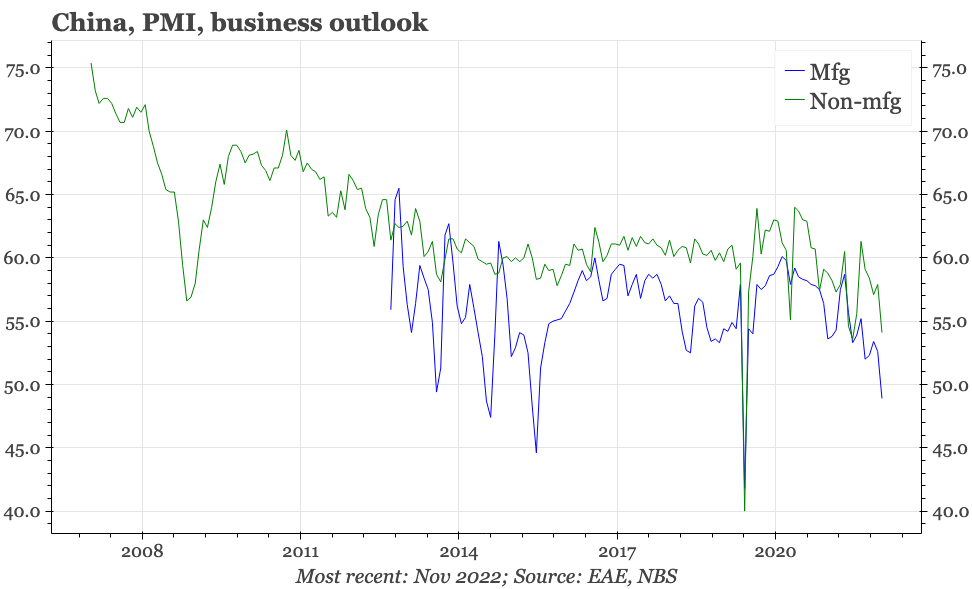

It was a bit more disappointing that other sectors showed no resilience. The manufacturing PMI fell to 48, not far off the 47.4 recorded at the time of the Shanghai lockdown in April. Domestic orders appear to have declined to the lowest since 2012. The construction PMI, which had shown tentative signs of bottoming out, weakened anew in November. It is particularly worrying that sentiment towards the longer-term outlook expressed in the PMI looks even worse than the headline.

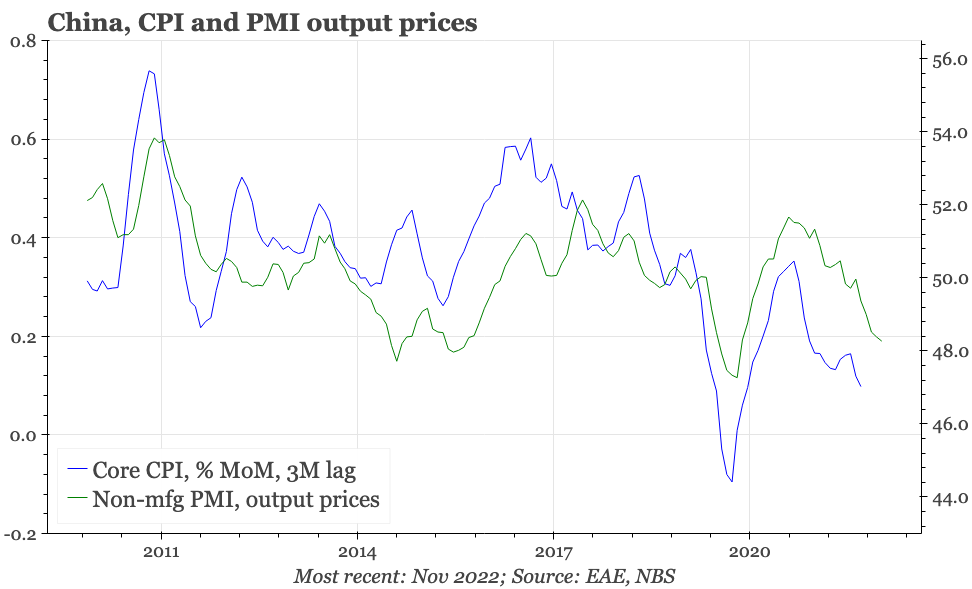

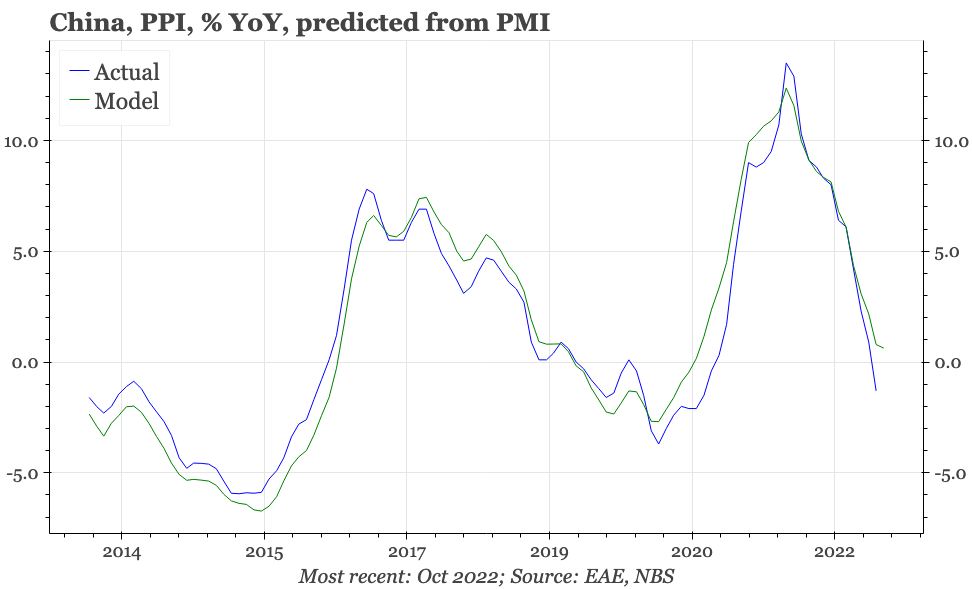

The one mildly positive development was that input prices in November didn't give up all the gains of October. That does suggest that the sharp fall-off in PPI inflation of recent months should be beginning to slow. But output prices weakened again, and that points to core CPI softening further. Overall, the deflation risk remains real, with the implication that real interest rates are still rising.

All told, after some tentative signs of bottoming through the end of Q3 and into Q4, this month the PMI points to clear renewed weakening of the cycle. The ongoing difficulties caused by covid policy are clearly weighing on growth, but whatever the reason, the PMIs suggest the government's stimulus efforts of recent months haven't been powerful enough.

This background perhaps probably explains why the pace of property easing has been stepped up in November. This accelerated loosening has gained some traction, producing a decent bounce in financial market sentiment towards property developers. That is encouraging, but is from a low level, and it is difficult to see it translating into much real economy momentum while consumer sentiment continues to get hammered by zero covid. So while the property policies do represent a shift, the outlook for the economy remains very difficult.