China – backward looking

Inflation was soft in November, but with the exit from covid dramatically changing the short-term outlook for the economy, these price data are backward looking. Just how much core CPI can now rise will be indicated by inflation expectations and liquidity preference.

November inflation

On a headline basis, November price data confirm the message of October: China is back in deflation. For input prices, there had been signs in the last couple of months that the sharp fall-back in inflation that started in late 2021 had begun to lose momentum. Those signs were important, but with underlying core inflation very weak, they weren't sufficient to point to a recovery in overall nominal growth.

A big reason for the weakness of CPI was the drag on aggregate demand caused by the government's covid policies. It remains likely that the early months of China's exit from zero covid will be messy for both society and the economy. But the direction of travel now seems clear. The eventual ending of many of the covid restrictions will remove the weight that had been depressing activity, and with property policy reversing too, inflation is likely to pick up again through 2023.

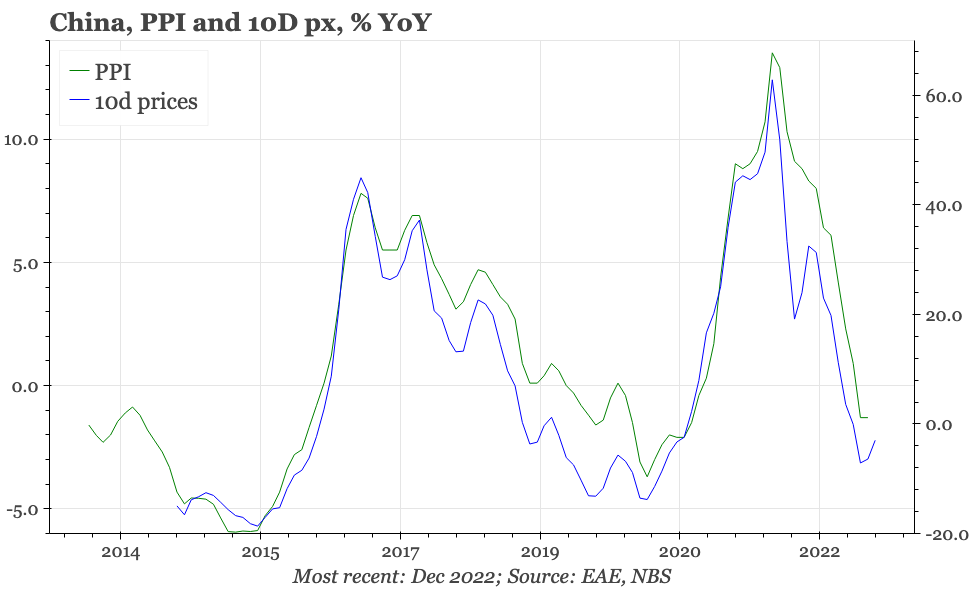

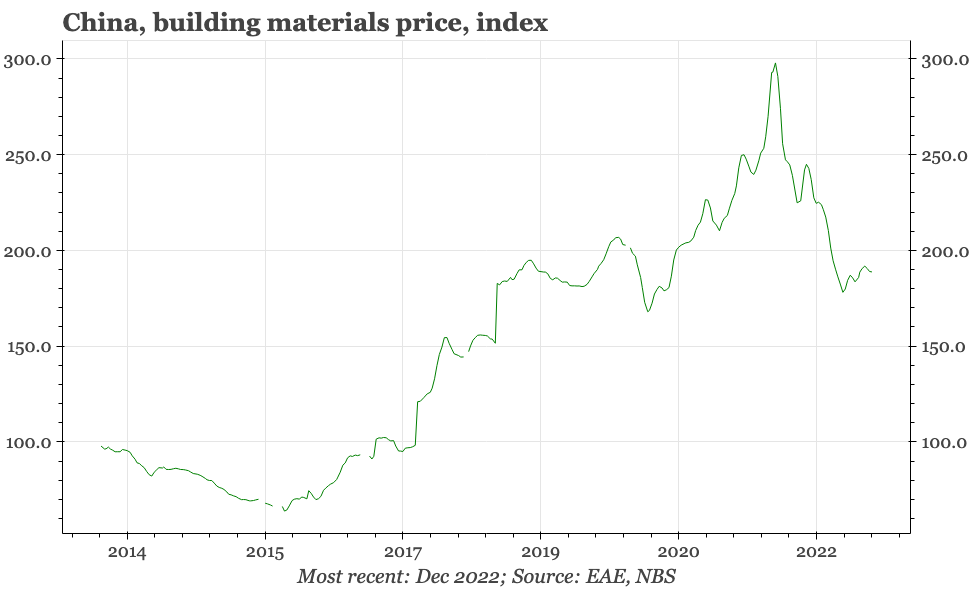

PPI fell -1.3% YoY in November, but that was unchanged from October. On a MoM basis, PPI picked up slightly in the month. That rise had already been seen in input prices in the PMI in December, and other slightly longer-term indicators – the NBS's 1o-day industrial price series, the USD, and even domestic construction activity – are now starting to point to a lift in PPI in the coming months.

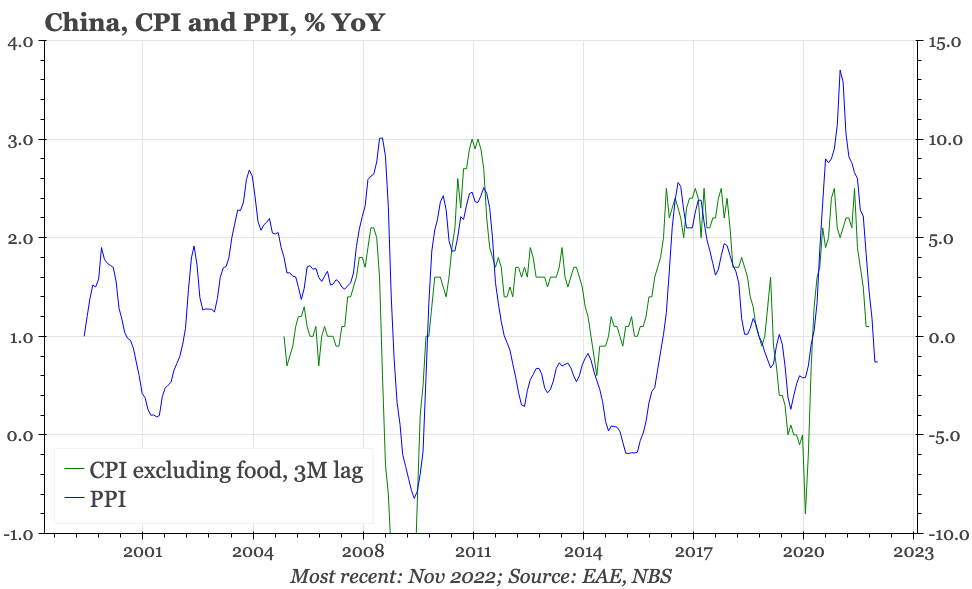

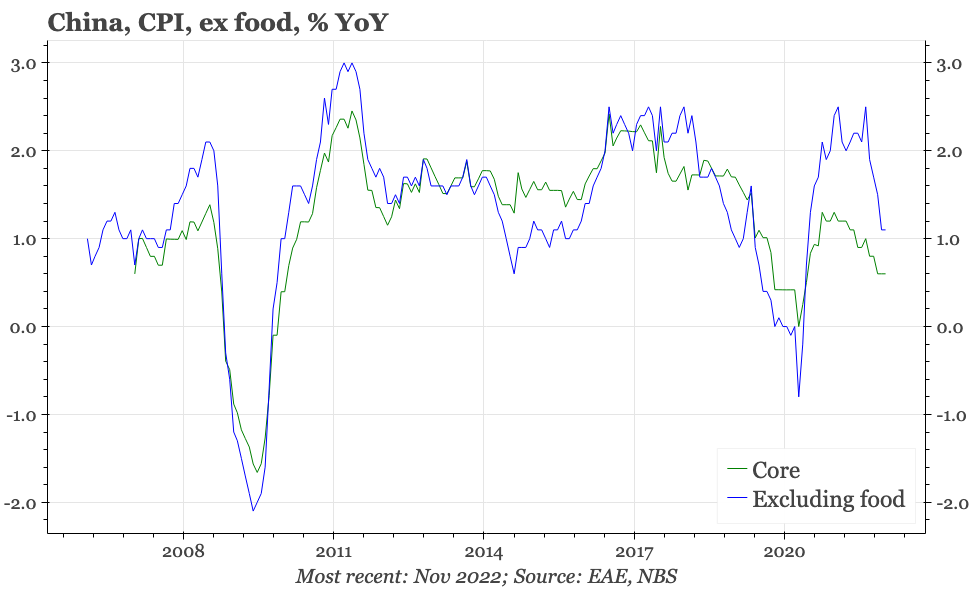

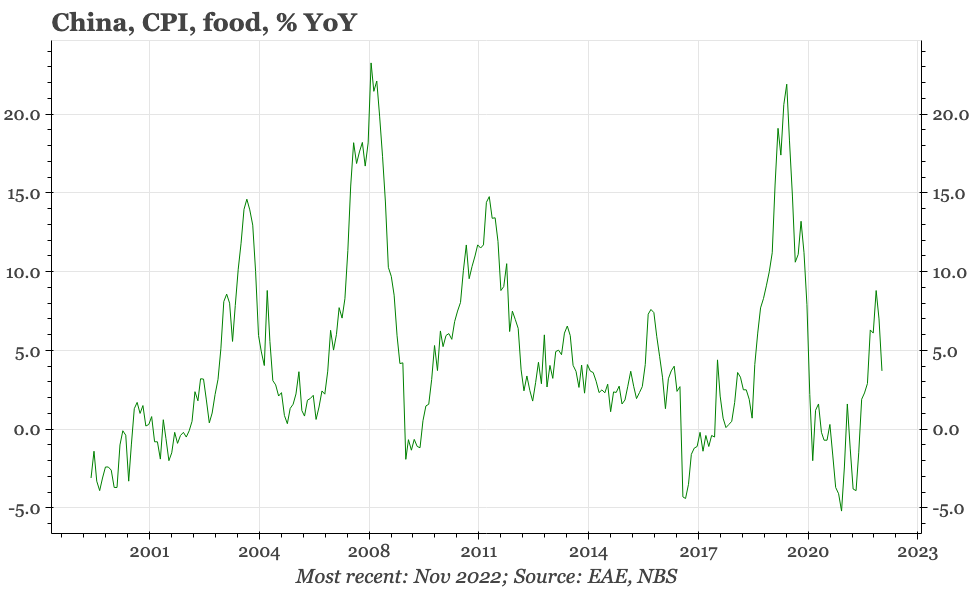

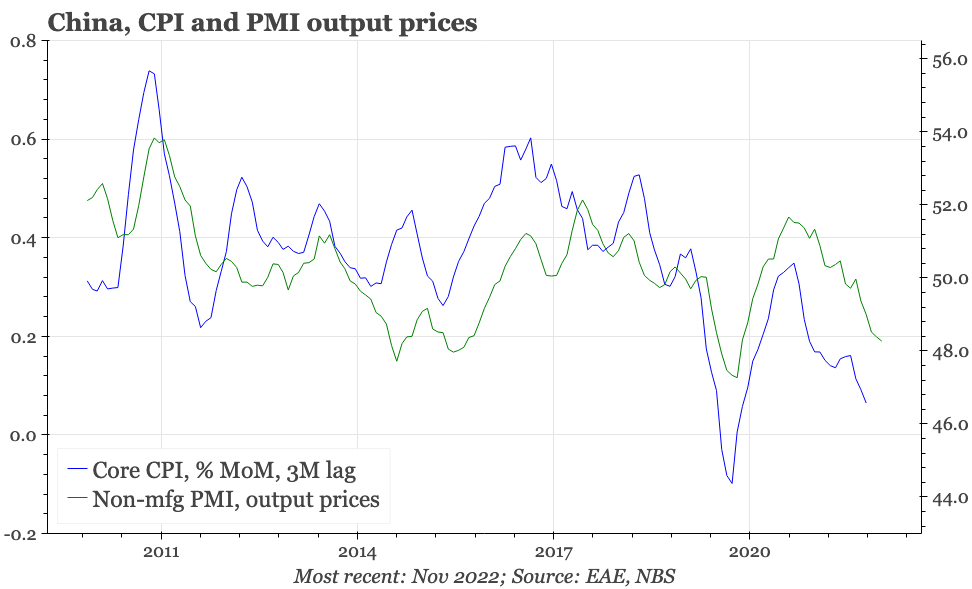

CPI inflation dropped to +1.6% YoY in November, down from 2.1% in October, and the lowest since March. That was driven by a fall-off in food prices. Core CPI on a YoY basis was just 0.6%, the same as in October. The level of core prices was unchanged in the month. Output prices in the PMI suggest that this very weak momentum in underlying inflation continues, but again, that will likely now change as activity picks up again.