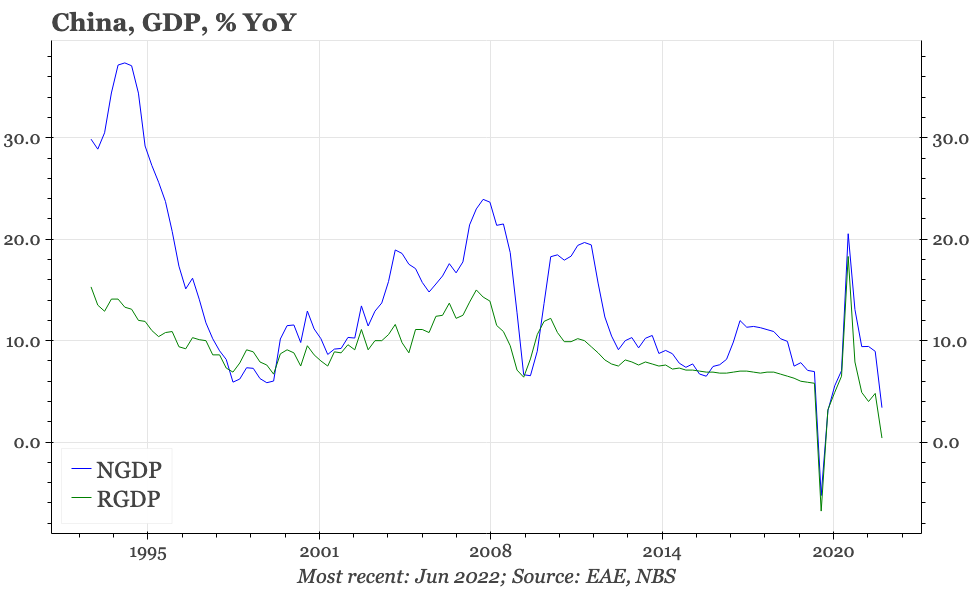

China – Q2 GDP

June data improved, and in July the economic indicators will likely be stronger again. But it doesn't feel like the conditions are yet in place for a sustained recovery in economic momentum through 2H. Indeed, it feels like there is a rising risk that the recovery runs out of steam.

GDP data are always backwards-looking. That's especially true when there was a lockdown of a major part of the economy early in the quarter that has since been relaxed. If there are more lockdowns, then a repeat of the very mild growth officially recorded in Q2 seems likely. Otherwise, the trajectory should be somewhat stronger.

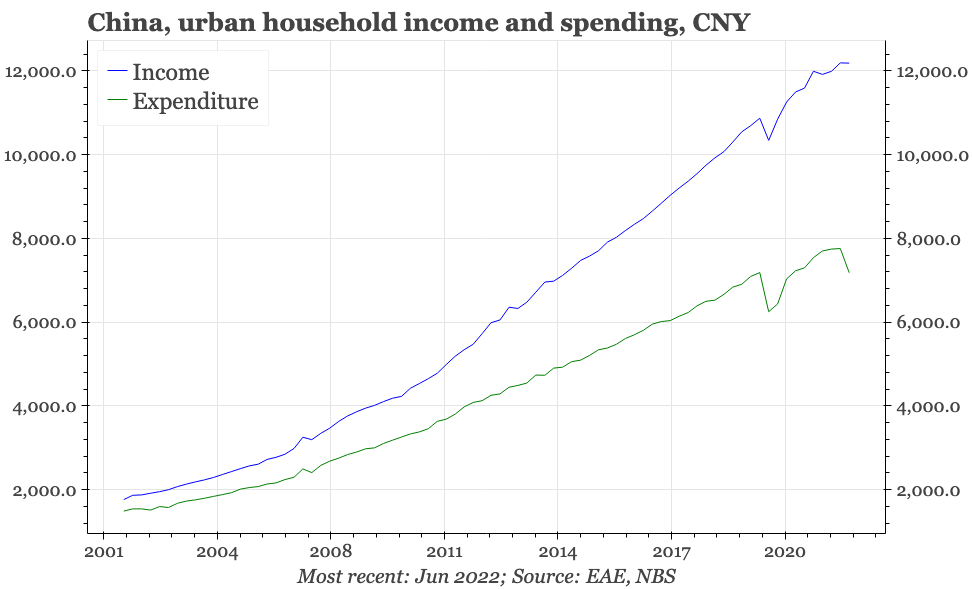

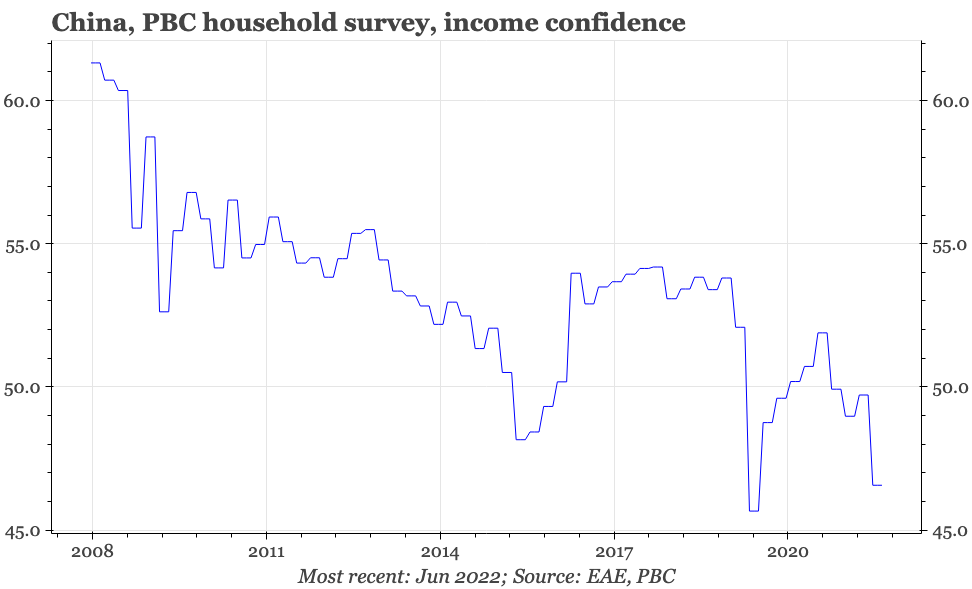

Of course, developments in an economy in one period do impact what happens in that economy thereafter. In this respect, the one interesting detail today was that nominal GDP growth held up better than it did in the first covid lockdowns of early 2020. Related to that, household incomes, which contracted in the first covid crisis two years ago, have this time around remained more stable. So, the scarring caused to the economy by the Shanghai lockdown is perhaps not as serious as suffered during the Wuhan lockdown of 2020.

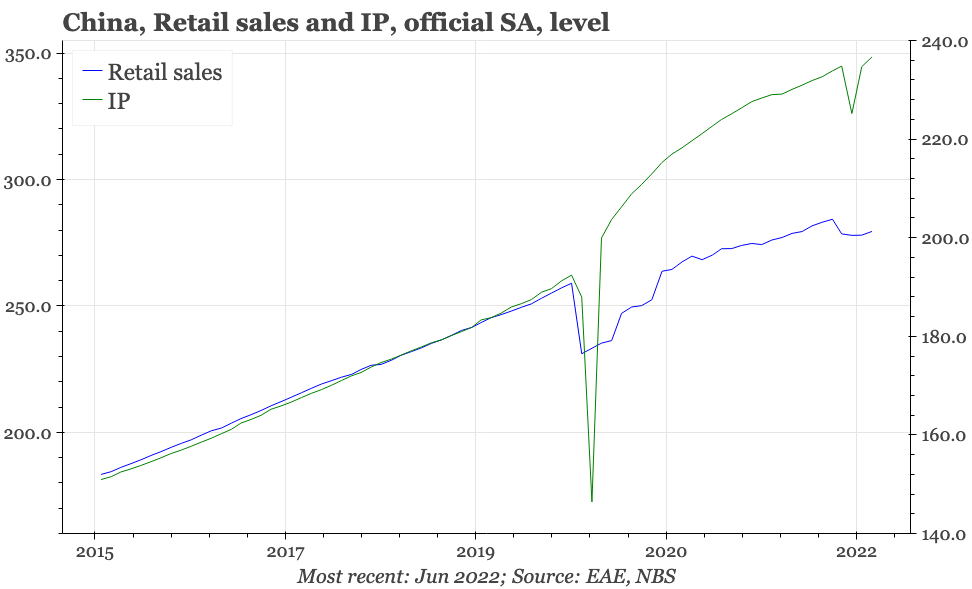

Today's data also did suggest that June data was better than April-May, with retail sales notably stronger last month. In terms of consumption, it is reasonable to think there's more upside in the very short-term as activity normalises. The government is also promising to spend more on infrastructure, so June's official 1% MoM rise in fixed asset investment also seems likely to be an indicator of things to come.

Probably, then, the July data are stronger again. But it doesn't feel like the conditions are yet in place for a sustained recovery in economic momentum through 2H. Indeed, it feels like there is a rising risk that the recovery runs out of steam. There are three main reasons.

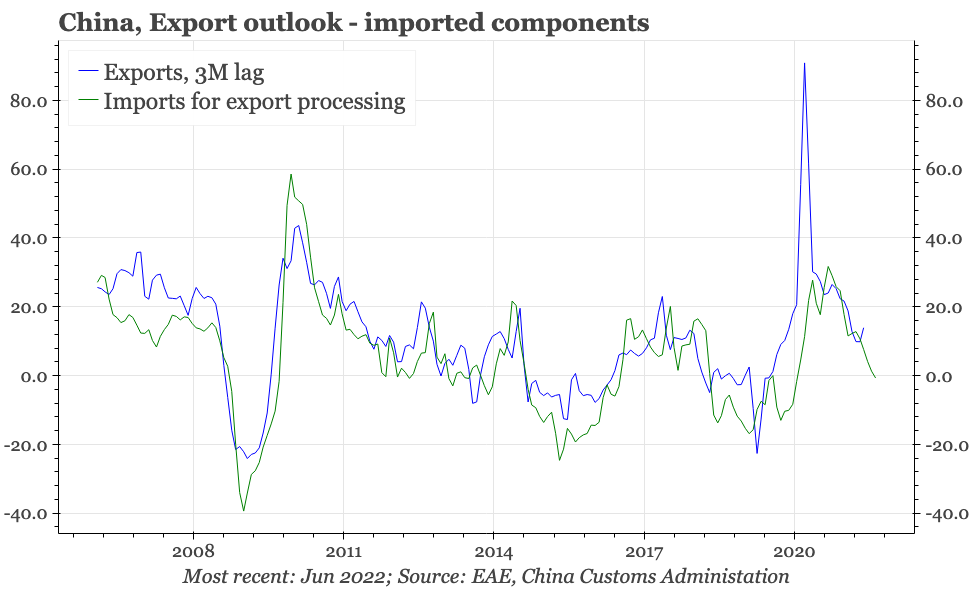

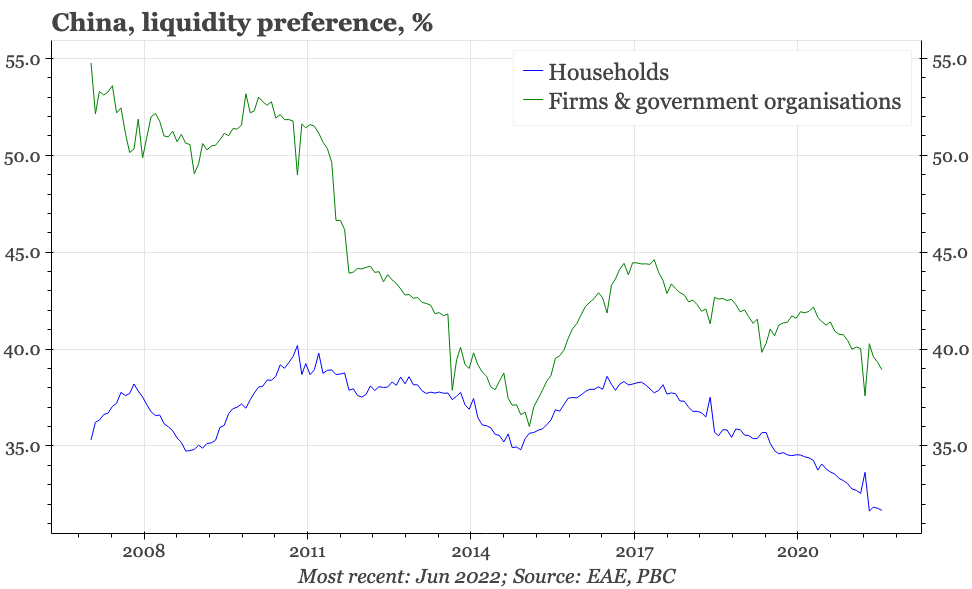

Industry. The industrial economy is outperforming consumption and services, which is what happened after the Wuhan lockdowns in 2020. But two years ago and the recovery in industry was helped by a boom in exports and a willingness of companies to spend. Similar dynamics aren't apparent this time. The trade data early this week show exports slowing, while the monetary data show that at least in June, liquidity preference in the corporate sector was still falling.

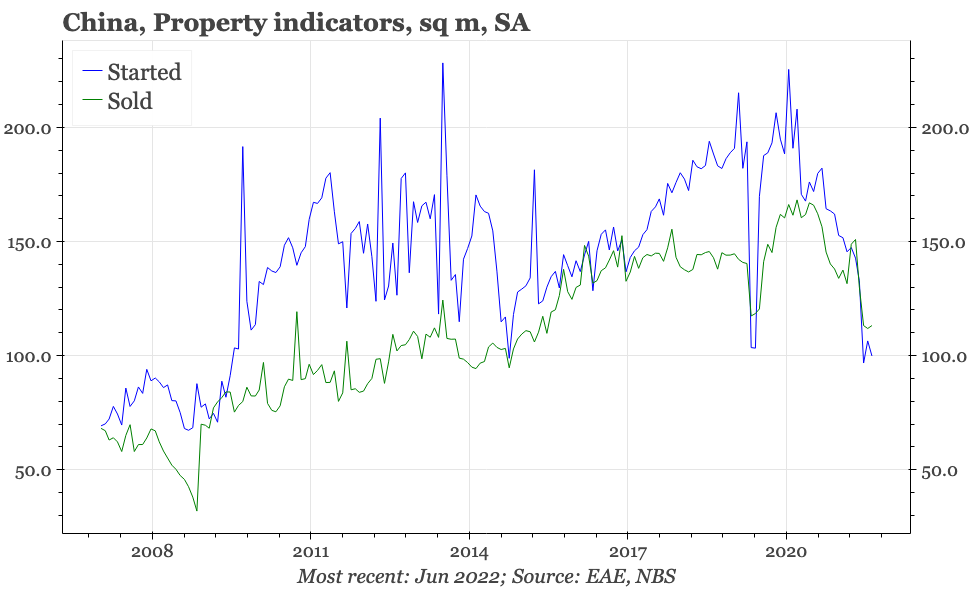

Property. Real estate sales did stop falling in June, but didn't start to rise, and housing starts remained very weak. More important still, the financial crisis that has enveloped the homebuilder sector since 2021 is if anything continuing to worsen, with debt and equity markets continuing to sell-off. Against this backdrop it will take a very strong rebound indeed in housing sales for property construction to grow at all, let alone to replay the sort of rebound in seen in 2020.

Consumption. Finally, beyond a natural rebound in activity as lockdowns end, it is difficult to see consumption rebounding in a more fundamental way. Before these latest lockdowns, most indicators suggested that consumption had taken a step down since 2020: consumer confidence, retail sales and household income growth had all failed to regain the strength seen in 2019. With cyclical policy continuing to focus on corporates and investment rather than households, there's little reason to think that consumption will now suddenly strengthen.

Of course, the government is keen for economic recovery to continue, and there are plenty of levers that the authorities can pull. But f0r the recovery to become sustainable, it still feels like two things need to happen: first, something that finally puts a floor under the crisis in the developer sector; and second, direct policy support for consumption.