China – tentative signs of a floor

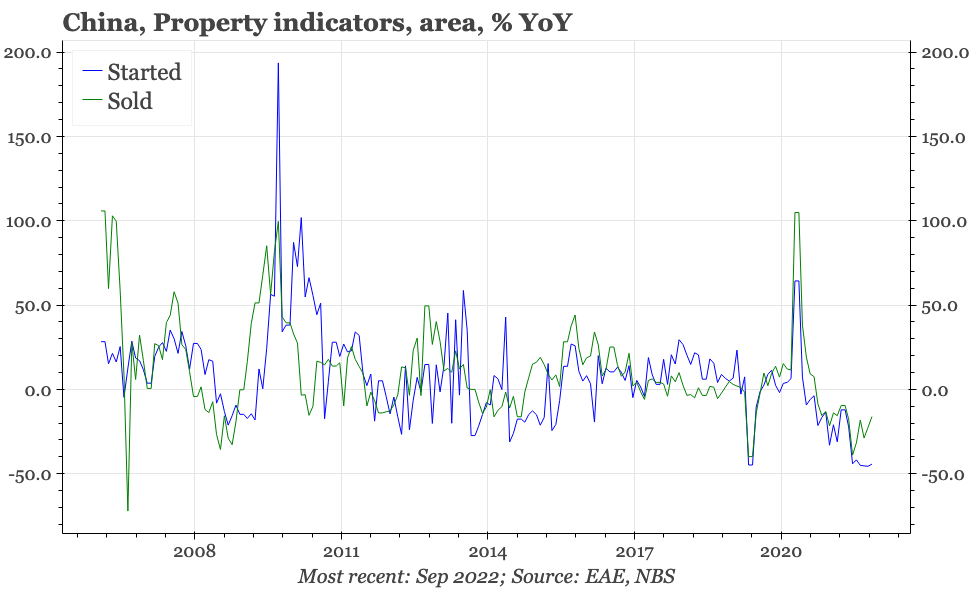

There are signs that the economy is bottoming, in the form of property sales, excavator sales and, to a lesser extent, property starts. These though are tentative, and need to strengthen before concluding the economy is through the worst.

Q3 GDP and September activity; September foreign trade

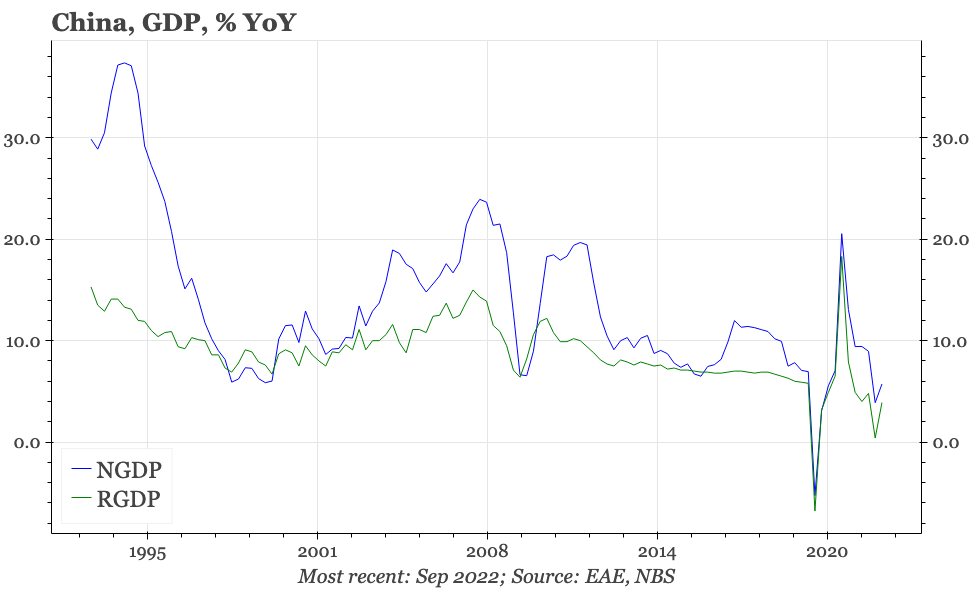

Q3 data were above market expectations, though that's done nothing to help investor sentiment towards China. That could be because there isn't much confidence in the quality of economist consensus forecasts (and why should there, if there is no confidence in the quality of the underlying data) though a more obvious trigger was the 20th Party Congress. Xi's total takeover, the national inexperience of the new premier, and the talks of wealth taxes coming out of the meeting are all undoubtedly unnerving.

That all said, at least in terms of the economic cycle, the economic data do look a touch better. I'm not at all sure about how the GDP data are produced (China doesn't publish the sort of detailed quarterly national accounts data that are usual elsewhere), but our tracker suggests the 3.9% YoY reported growth in Q3 was at least consistent with the official data for industrial production and retail sales.

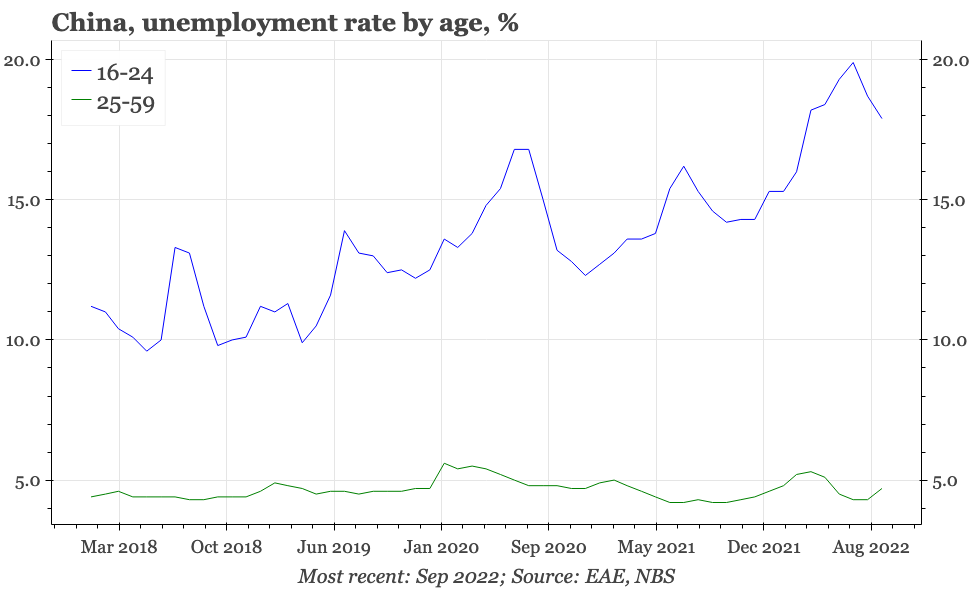

As has been usual in China since the Covid-19 pandemic began, it is the industrial sector where there's more sign of growth. Growth in both IP and retail sales ticked up in September, but the strengthening in IP was by far the more obvious. Youth unemployment did fall in September, but that is probably seasonal. The foundations for retail sales look poor as long as zero covid remains in place – and there were zero hints at the Congress of any change. In fact, the outlook for retail sales looks poor even if zero covid ends, given the rising probability that the government's containment policies have imparted long-lasting structural damage on Chinese consumer sentiment.

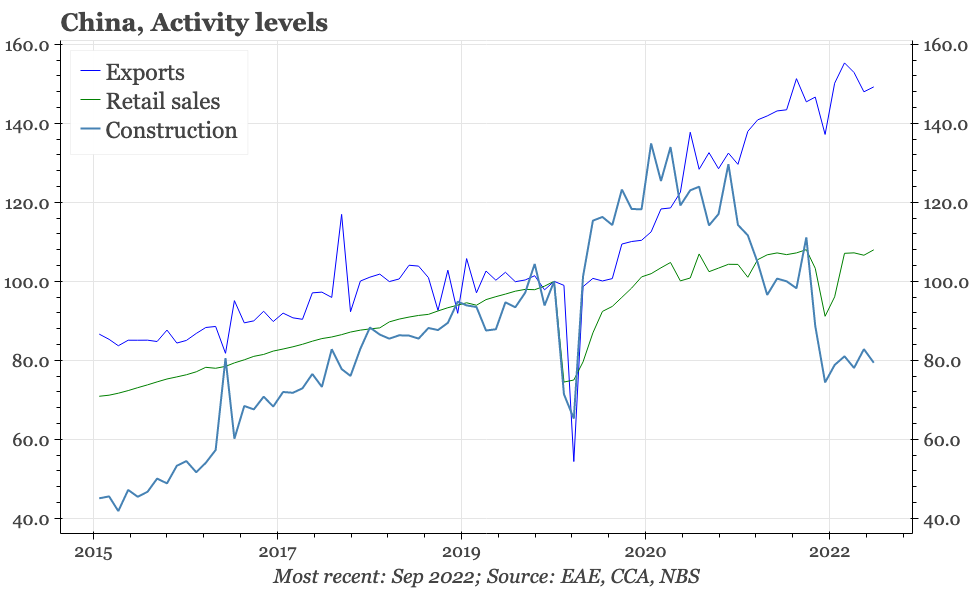

It isn't plain sailing for the industrial sector, either. Particularly since 2021, IP has been supported by external demand. But that is now fading. Exports in September ticked up in USD terms from October, and demand from DM remains surprisingly resilient. But YoY growth in external shipments did soften again in September. Imports of components also dropped, and both that and regional indicators continue to point to export growth falling below zero in the following months. The one exception to that might be in auto shipments, which surged again in September.

As exports slow, then growth in IP and the economy will be increasingly dependent on domestic demand. Given this, it is significant that China's construction cycle shows tentative signs of bottoming. That can be seen in excavator sales, property sales, and, to a lesser extent, property starts. These developments should get a further lift from the accelerated easing of policy pursued by Beijing since September.

None of this is to conclude that China's domestic industrial cycle is out of the woods. Financial markets suggest there's still been no turnaround in the fortunes of the listed property developers. That imposes a ceiling on how far any recovery in construction can run. Consistent with that, while not getting worse, excavator sales haven't lifted much. Property starts are only improving in YoY terms; sequentially, the trend is still down. The continued weakness of construction continues to point to further declines in imports, and as long as the domestic cycle is this soft, there remains the risk of a financial accident that pushes the economy lower still.

So, the argument wouldn't be the worst is yet over, just that the risks around the economy are a bit more balanced than they have been for a while. To think that there is a more material improvement, the indicators would include not just the construction data strengthening, but also: an easing of the financial pain facing developers; a lift in broad liquidity preference in the economy; and a rise in domestic commodity prices.