China - monetary indicators still mixed

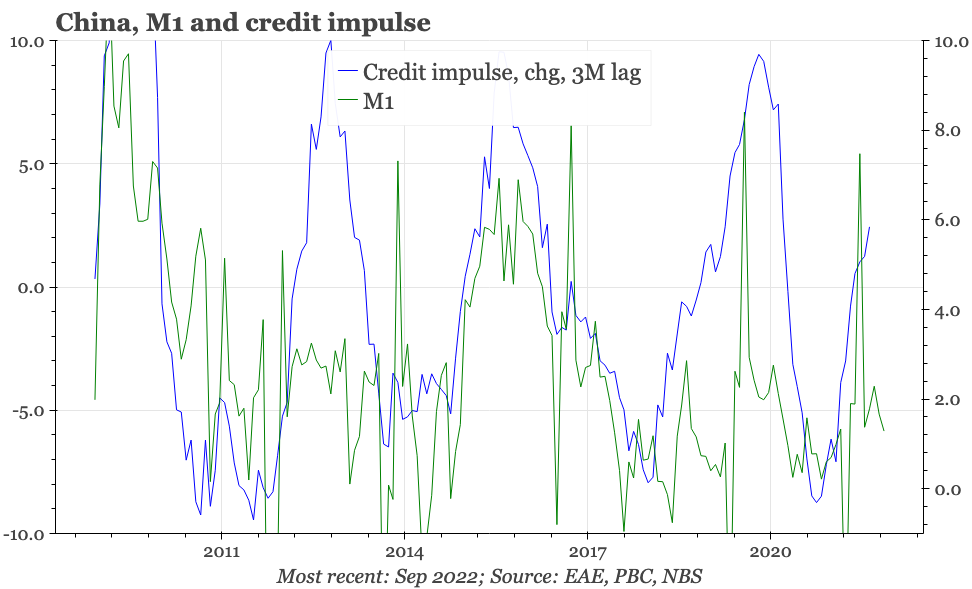

With September's monetary data suggesting a further fall in liquidity preference and M1 growth, it still doesn't look like the economy is poised for a turnaround. But it is starting to feel like the risks around the cycle are less to the downside than they have been for the last few months.

September monetary data; PBC Q3 bank survey; PSL restart

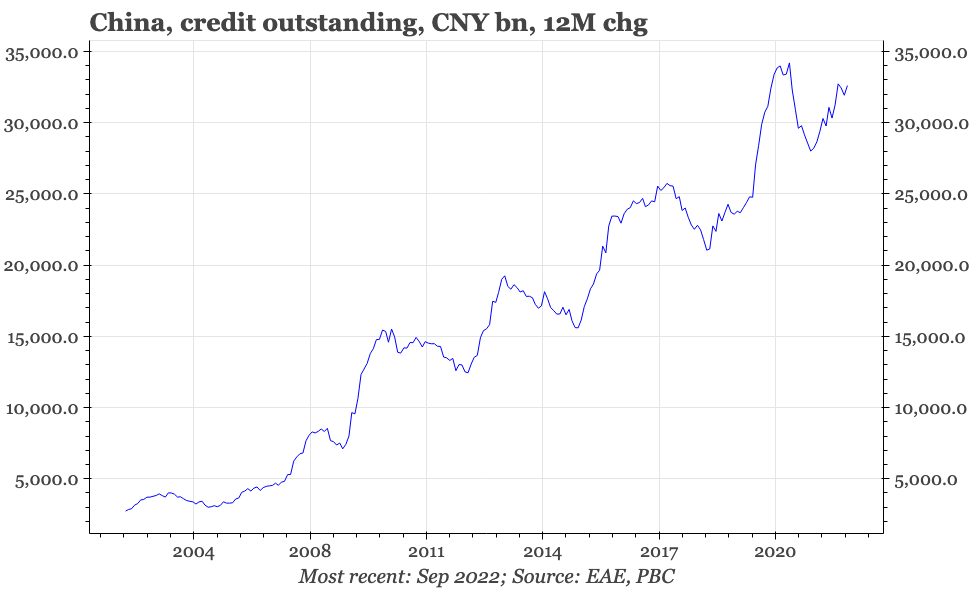

Monetary data in September were stronger than market expectations, but the details were more mixed. Sequential growth in total credit did tick up, but not by enough to lift the average of the last three months, which dropped back to an all-time low. On a 12M cumulative basis, credit growth stalled in Q3. This clearly is nothing like the sharp rise in credit growth that helped drive the recovery out of the first Covid-19 lockdowns of 2020.

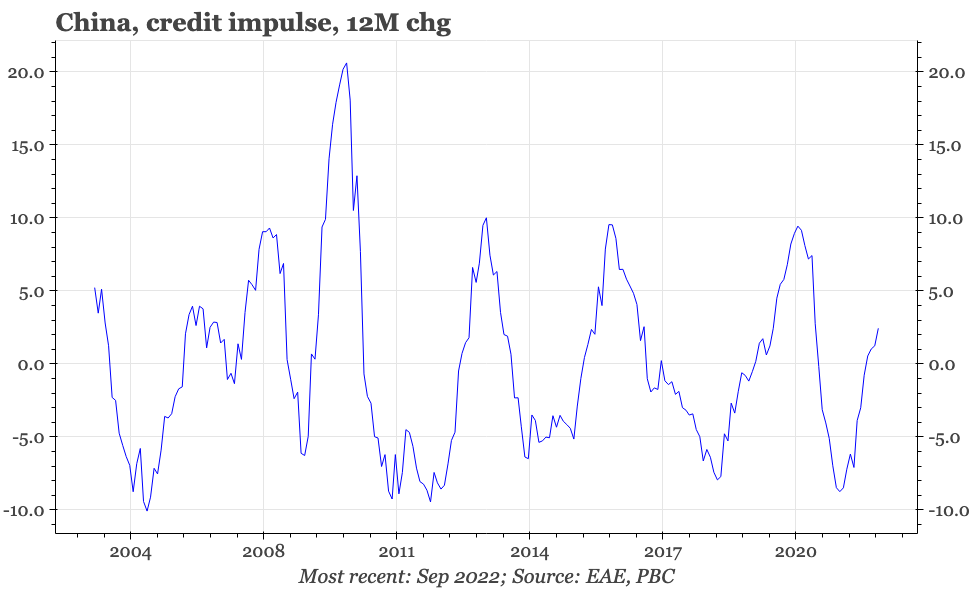

If there is a silver lining for economic growth, it is that the impact of credit growth these days might be somewhat bigger than the headline data suggest. With nominal economic growth so weak, and the stock of loans outstanding so large, even an anaemic absolute rate of credit growth should still be strong enough to lift the credit impulse. That does seem to be happening, though we'll need the release of the official Q3 GDP data (delayed because of the congress) to know for sure.

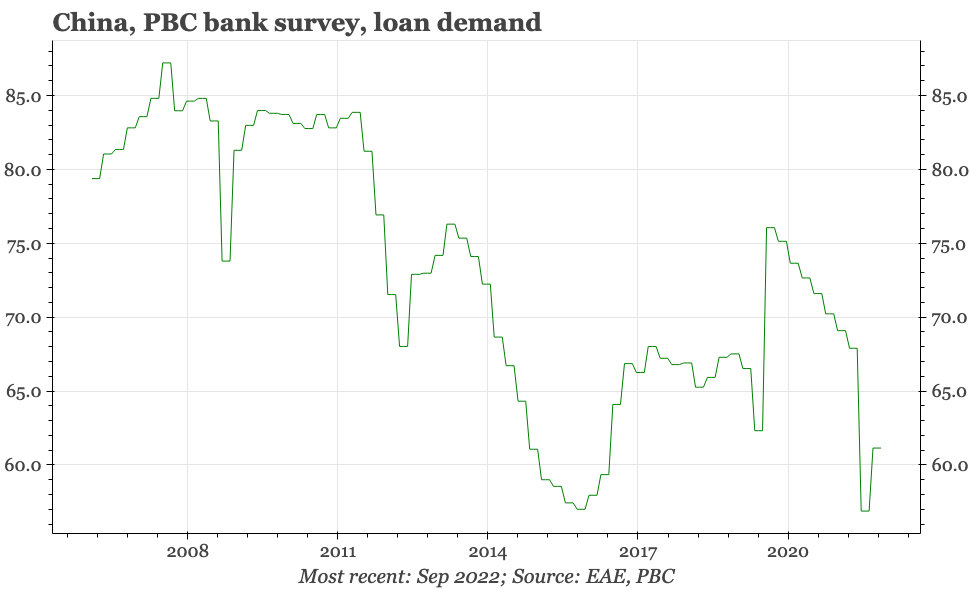

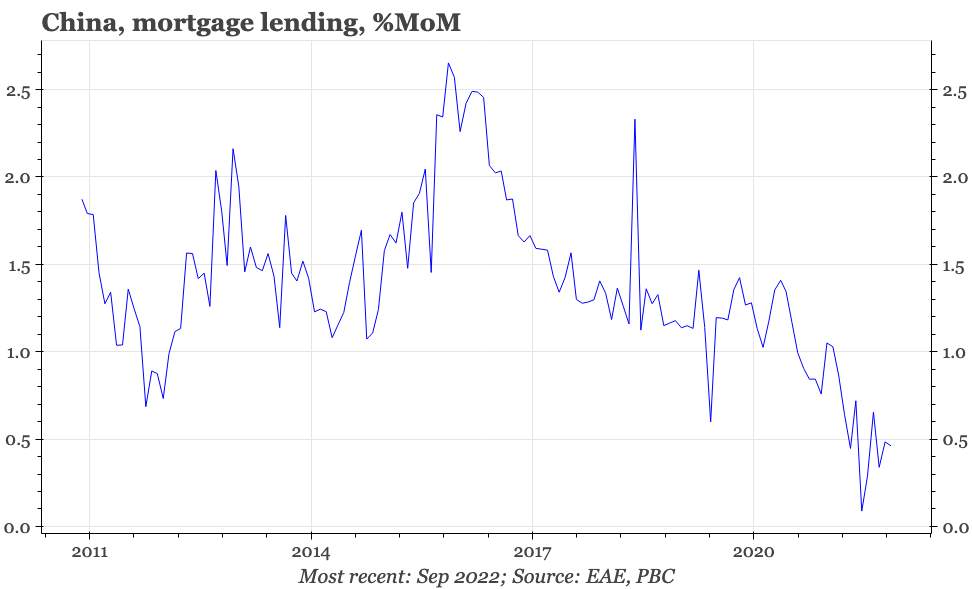

Policymakers have been trying to push up credit growth, by pressuring banks to lend, and by trying to revive demand for credit. These efforts are bearing some fruit. The monthly credit data are now starting to suggest that mortgage lending has bottomed out, and in the PBC's Q3 survey, bankers reported a rise in demand for credit. All that said, the message from both indicators is that while things are no longer getting worse, there's also no real signs of a turn for the better.

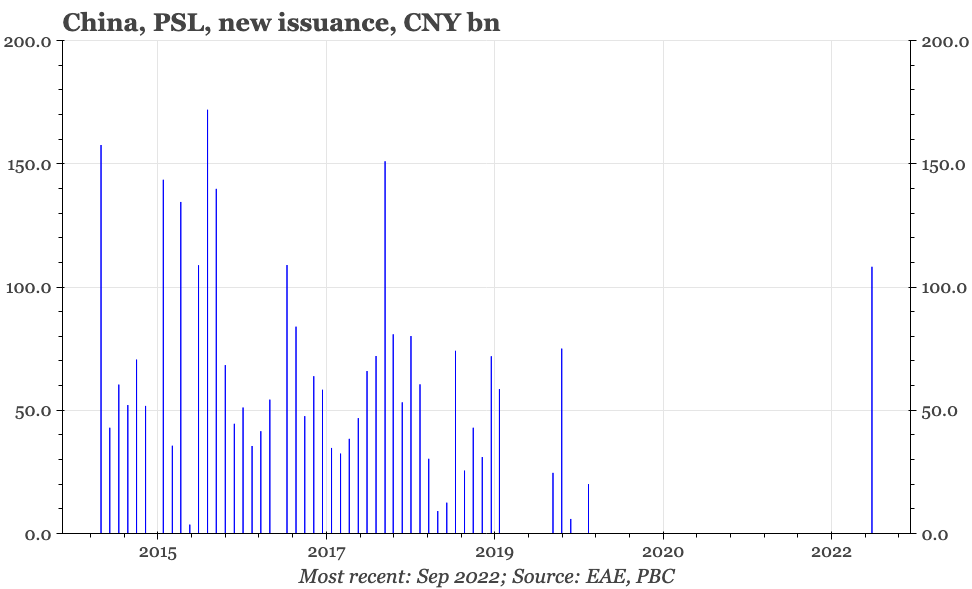

All these trends no doubt were behind the stronger easing that occurred through September. There was the well-publicised stepping up of property market easing, with yet more mortgage rate cuts, but also tax exemptions. Local media are now reporting that some mortgage rates are below 4%, down from 5.5% at the end of 2021, which looks to be the sharpest cuts on record. There was also the more opaque restarting of the PBC's Pledged Supplementary Lending scheme.

One of the PBC's (many) vehicles for lending to financial institutions, the importance of PSL is as a specialised facility for lending longer-term to China's three policy banks. While the news of the restarting of the scheme appeared without fanfare in the bare-bones PSL statement published monthly by the PBC, its revival has triggered a lot of discussion. That is because the first wave of PSL lending in 2015-16 helped drive a big recovery in the property market.

This time around the focus seems more on infrastructure, but still, it is another sign that policy is pushing harder. With September's monetary data suggesting a further fall in liquidity preference and a fall-back in M1 growth, it still doesn't look like the economy is poised for a turnaround. However, it is starting to feel like the risks around the cycle are less to the downside than they have been for the last few months.