China - a floor?

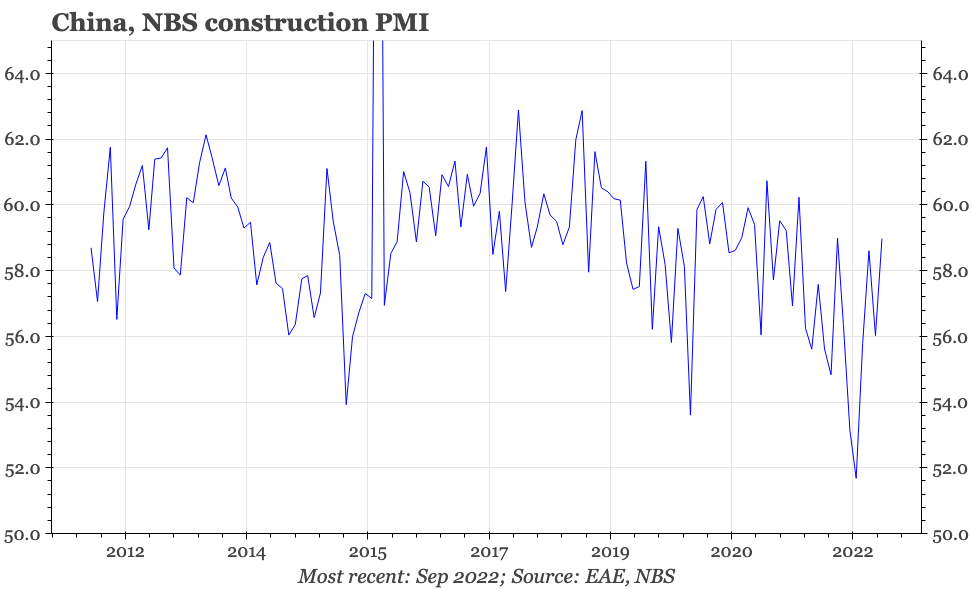

The overall tone of today's PMIs suggests that China's cycle remains weak. However, the construction PMI rose again, and with the official headline manufacturing PMI and input prices creeping up, for the first time in a few months, there is some risk that the domestic industrial cycle is bottoming.

Weak PMIs, except for construction

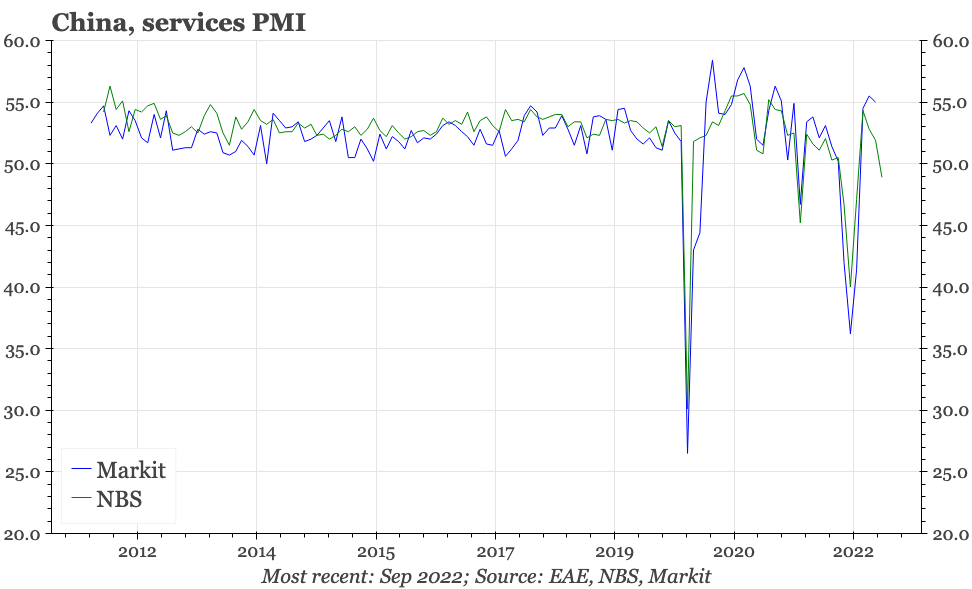

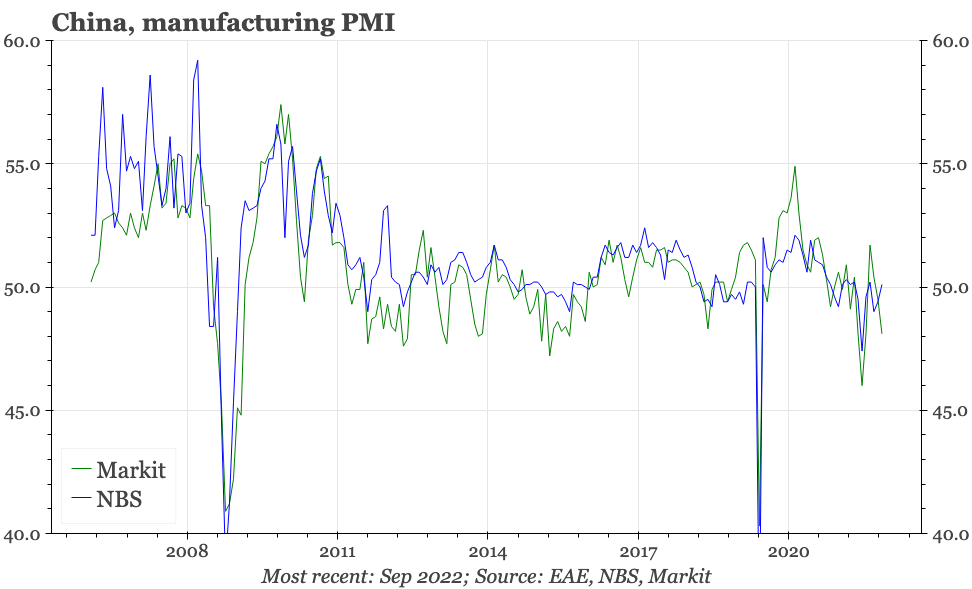

The September PMIs show that the cycle remains weak. The official manufacturing PMI did rise back above 50, but only barely, and the Caixin version weakened further from 49.5 to 48.1. The official services PMI declined for the third consecutive month, with the headline falling below 50 to 48.9. Composite output, according to the NBS, is once again barely growing. The CKGSB small business survey also fell in September.

The details in the PMIs were also mainly weak. Of particular importance for the cycle is the softness in the 6M outlook scores. In the official manufacturing PMI that was a bit stronger than in August, but still below 50. In the Caixin version, the outlook score fell by more than 3ppts to the lowest since November 2019. This sort of long-term corporate caution will be an obstacle to any pick-up in the private sector capex cycle.

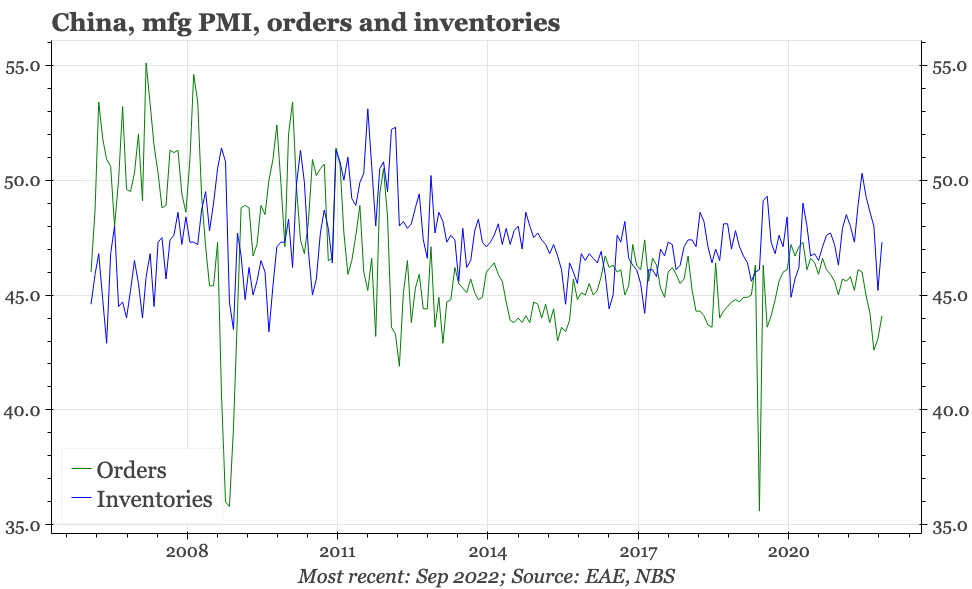

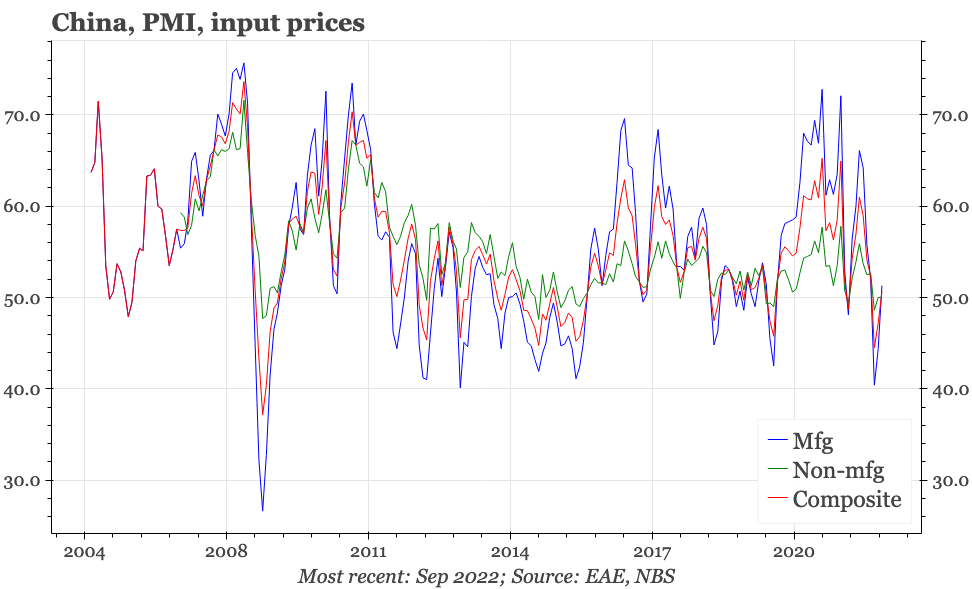

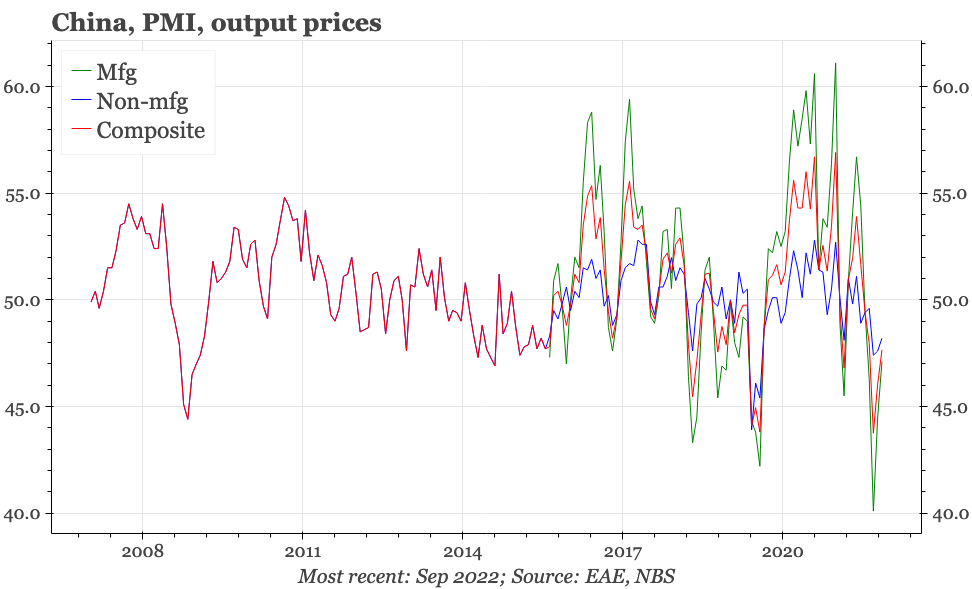

In the official PMI, new orders were better in September than August, but the score was still below 50, and the improvement in orders was more than matched by a rise in finished good inventories. Input prices did rise above 50. That's probably not a big enough increase to mean sequential PPI turned positive in September, though there could be a pause in the sharp fall of recent months in YoY PPI. However, output prices in both manufacturing and non-manufacturing remained well below 50. As before, deflation remains a bigger risk in China than inflation.

Among all this bearishness, the one positive data point was the constriction sector PMI, which seems to have pulled out of the depression of earlier this year. This is a poor quality data series, with lots of noise from month-to-month. But the construction PMI has risen for a couple of months now. The increase is perhaps an indication that the government's promised infrastructure push is beginning to show up in real demand.

Putting the rise in the construction PMI together with the modest improvement in the official manufacturing headline and the recovery in input prices, and for the first time in a few months, it is now possible to build a story that the domestic industrial cycle is bottoming. That is worth highlighting as a risk, although with property still so weak, it is difficult to be persuaded that this is indeed what is yet happening. Even if it is, the overall message of the PMIs is that more needs to be done to translate any turn in domestic construction into a broader macro recovery.

See here for more detailed charts.