China – taking stock

China's export market share gains show local firms remaining competitive, and that should make some individual equities interesting. But macro trends don't look strong enough to lift rates. Indeed, price indicators look more deflationary than inflationary.

Based on their rhetoric, at least, macroeconomic policymakers in China seem to be all about continuity. They came into this year wanting “stability” in the economy generally and the property market in particular, and set a rather aggressive economic growth target of 5.5%. The economy has since been hit by a big new negative shock in the form of the covid lockdowns, a shock that seems to have undermined the property market once again. But premier Li Keqiang last week insisted that the policy approach isn't changing:

Since 2020, our policies in tackling COVID-19 and other major impacts have been appropriate in scale, and we have not resorted to massive stimulus.....We will keep macro policies consistent and targeted, and continue to focus efforts on helping market entities resolve difficulties, to preserve the foundation of economic development. Macro policies will be both targeted and forceful, and well-calibrated as appropriate. We will not introduce supersize stimulus measures, issue excessive money supply, or sacrifice future interests to go after an excessively high growth speed.

That isn't to say that the government hasn't stood entirely still in the face of the covid shock. There were interest rate cuts, and the 33-point package of measures from the State Council. But Li now seems to be admitting that this won't be enough to get to 5.5% this year, saying that it is important to take a “realistic approach” and that the government would “do the best within our means to strive for fairly good results in economic development for the whole year”. The premier hasn't given up on growth, but there has been a paring back of expectations.

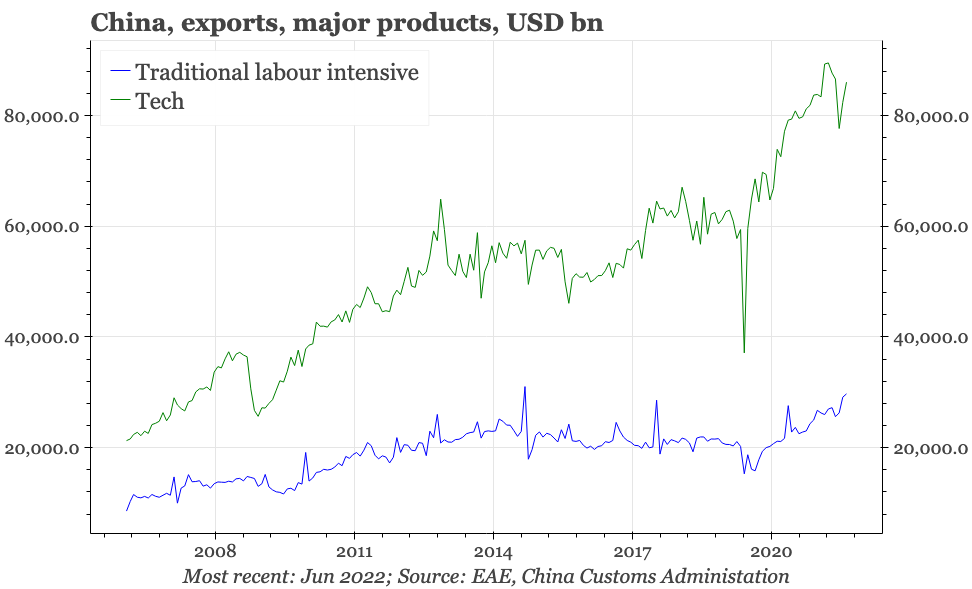

There are some bright spots in the economy. The export sector has had a remarkably strong couple of years. Undoubtedly, that's been helped by the income support enjoyed by households in DM economies, and the fact they used more of this money to buy goods than services. But China's market share, not just in DM but in EM economies too, continues to rise. In terms of products too, the rise has been fairly broad-based, with sharp increases in exports of traditional labour-intensive items like toys and furniture, as well as technology goods and – albeit from a very low starting point – cars.

With the proportion of Chinese exports made by foreign firms falling, and domestic state-owned firms not being big sellers in overseas markets, the rise in overall exports shows the rising competitiveness of Chinese private firms. This would also suggest that Li Keqiang's push to improve the business environment, by cutting red tape and taxes for the corporate sector, is having some success. Over time, this should be good for individual equities in China.

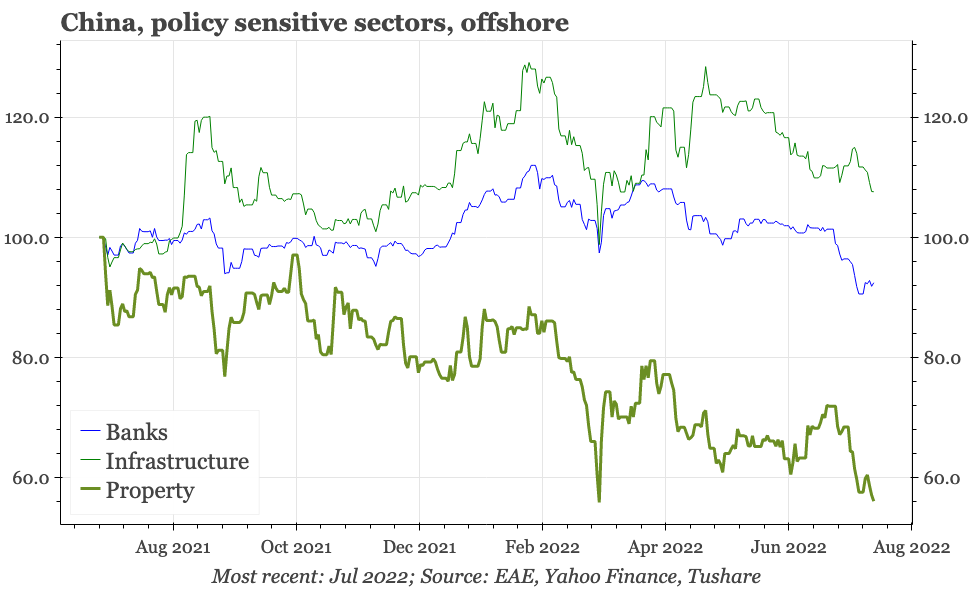

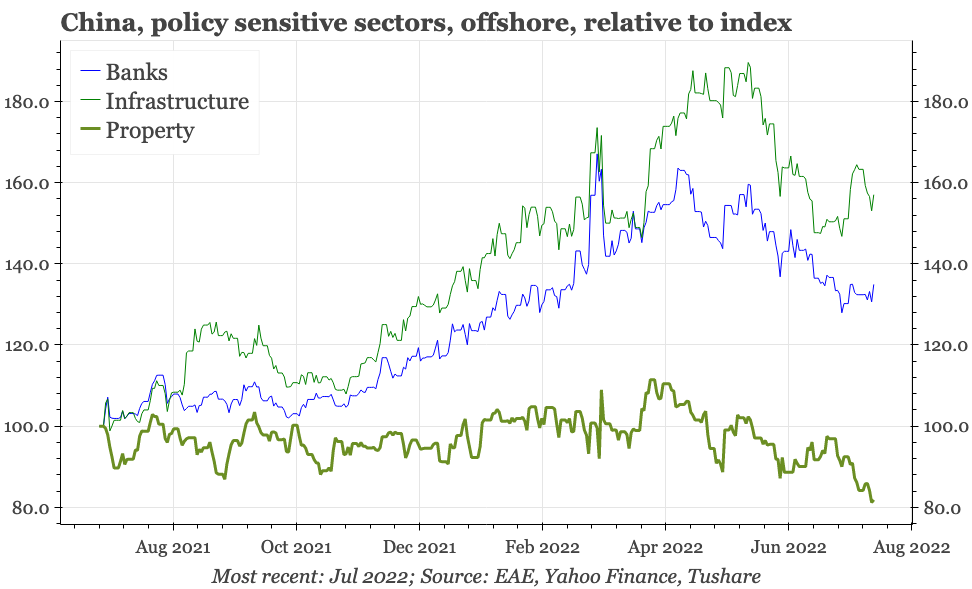

However, it is hard right now to make a bullish case for the overall economy, and thus to think that either equities overall or rates will rise much. Exports have been resilient, but seem unlikely to hold up so well as the global cycle turns. Meanwhile, domestically, the cycle still seems to lack any real upwards momentum. In equity markets, traditional policy-sensitive sectors – property, banks, and infrastructure – remain weak. Offshore listed property debt is even weaker.

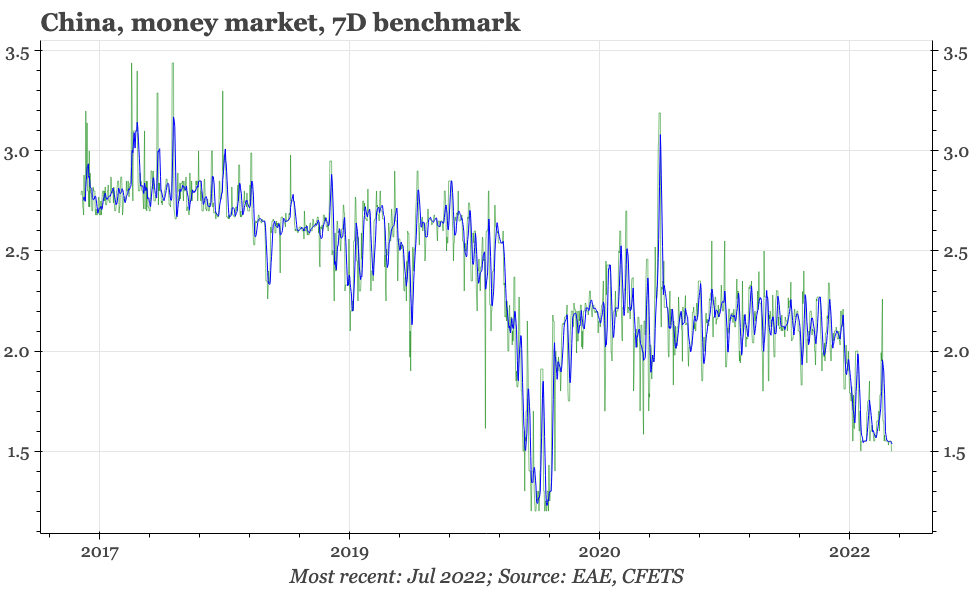

It isn't impossible that the real economic cycle can regain momentum in the face of such developments. The crisis in the offshore listed property developer sector hasn't derailed onshore financial markets, so is arguably somewhat contained. Onshore short-end rates remain very low, and corporate spreads have narrowed to around record tights. The curve has modestly steepened since the beginning of 2022.

This stability in overall onshore fixed income in part reflects the policy priority of improving the flow of money to the real economy, a push related to Li Keqiang's desire to improve the business environment for smaller firms. With property specifically, officials do say that lending to the homebuilders rose in June, while mortgage borrowing is increasing more quickly than at any time since 2019. Remarks from Li Keqiang suggests that construction of social housing – so unrelated to the usual property cycle – might be a beneficiary of the government's current “targetted” round of fiscal largesse.

That said, if the domestic cycle was really getting going, it seems unlikely that onshore financial markets would be this flat. Obviously, one source of concern for markets remains Covid-19, with the case count across the country creeping ever higher in recent weeks. But there's also other broader reasons to be sceptical about the growth outlook. Partly because of the weakness in bank equities, an onshore Financial Conditions Index has tightened a bit through July. Real estate remains a big sector in the economy, and even if the financial stresses remain confined to private developers, they are big enough to matter. Previous attempts to use social housing construction as a counter-cyclical tool have come to nothing.

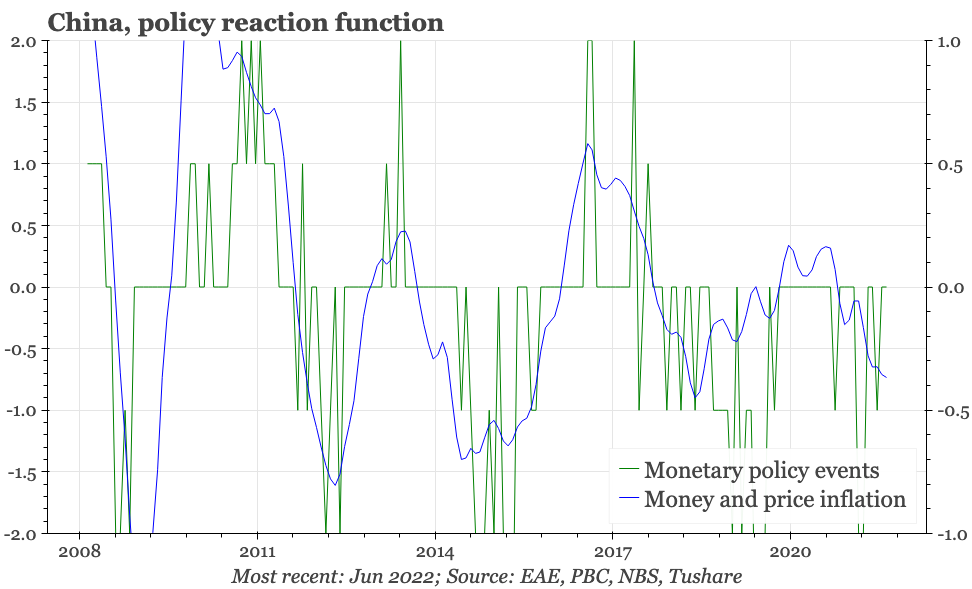

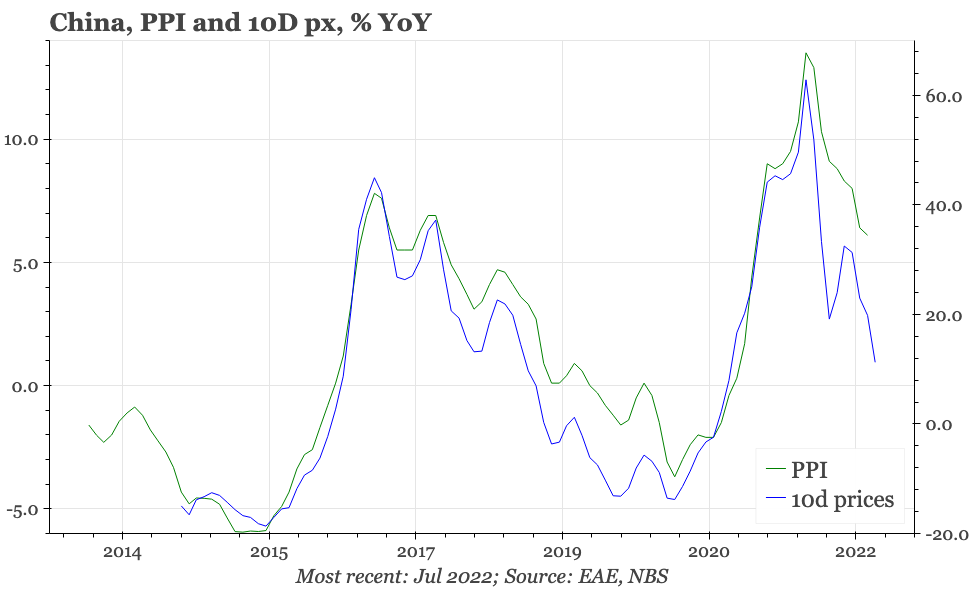

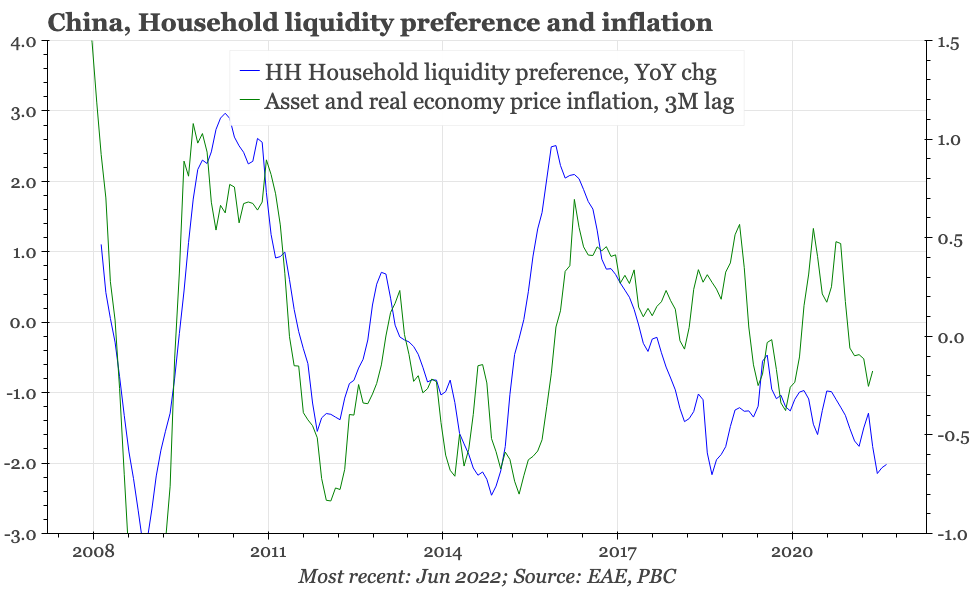

Moreover, in contrast to the inflation pressure being felt in much of the rest of the world, neither that nor reflation is evident in China. Property prices remain weak. The detailed monetary data for June at the end of last week show no turnaround in consumer liquidity preference – a useful leading indicator for overall inflation. Moreover, selected commodity prices are now falling quite quickly, indicating the recent turn down in PPI inflation has further to run.

So, overall, it feels that cycle momentum in China lacks strength. At the very short-end, rates could reverse higher on a shift in PBC liquidity management shifts. Otherwise, though, it feels like rates are quite well-anchored, with a rule of thumb based on inflation and monetary trends suggesting the PBC is likely to loosen monetary policy further. The combination would be a flatter curve.

One risk to this status quo would be more powerful macro policy, still not inconceivable despite Li's rhetoric. The two sectoral developments that would have a big impact on macro would be a change that finally puts a floor under the homebuilder sector, and any sign that the government is providing meaningful direct income support to consumers.