China - taking stock

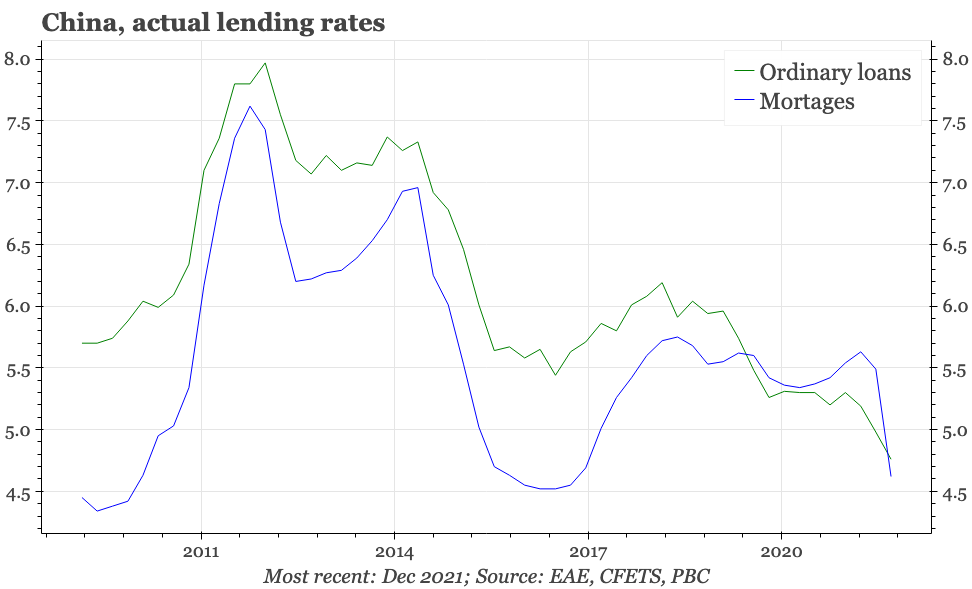

Today's rate cuts were focused on mortgages. That follows Q2, when home loan rates fell at the sharpest pace on record, and yet property remains weak. There likely needs to be more direct help for developers and consumers, and a more united policy showing from Beijing, to get the cycle going.

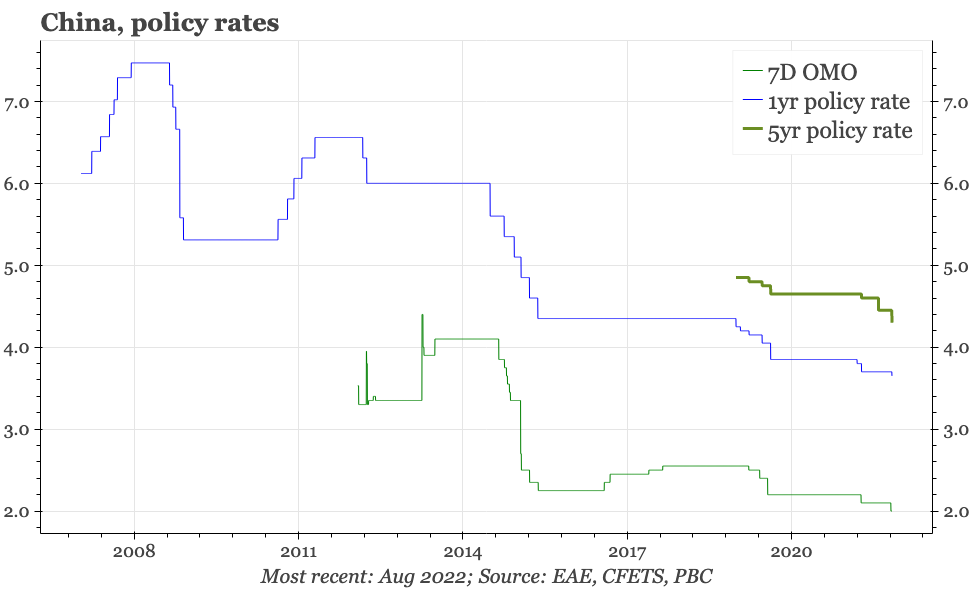

Today's monthly announcement of the Loan Prime Rate showed pass through from last week's cut in two PBC policy rates. The follow-on wasn't exact though: while the cuts for the 7-day benchmark reverse repo and one-year Medium-term Lending Facility (MLF) rates last week were 10bp apiece, the LPR today was reduced by 5bp at the 1-year level but 15bp for the 5-year maturity.

There's a bit more room for cuts in the 5-year rate, in the sense that it was cut by a cumulative total of 20bp in the 2019-20 round of reductions, compared with the 40bp of cuts then made in the 1-year. Policy priorities have changed since then. Two years ago and the government wanted to help corporates by cutting shorter-end rates, but aimed to keep longer-term rates higher to keep a floor under the cost of mortgages and so try to contain real estate inflation. With property now the (very) weak link in the whole economy, the official main mantra of policy is instead to “stabilise” real estate, which apparently means making mortgages cheaper.

In a usual cycle, the changes made even before today should have taken the government quite far towards achieving stabilisation. In the usual section announcing actual interest rates each quarter, the PBC's latest quarterly monetary policy report released a couple of weeks ago showed that mortgage rates have fallen by almost 90bp between March and June. That's the sharpest cuts in any three-month period on record. It is likely that after today's cut in the LPR that actual nominal mortgage rates in Q3 fall to record lows.

But this cycle doesn't look to be usual. The cuts in mortgage rates do seem to have had some positive impact on transactions, but they haven't led to any real improvement in sentiment in the sector: listed developer equity and debt remain fragile, and the stories of local governments resorting to increasingly extreme measures to try to boost property sales suggest the sector remains in crisis. That the quite big cuts in nominal rates are only having a mild impact on the market implies that price expectations are falling more quickly. The rise in real interest rates in turn can be seen in monetary data, which show savers continuing to move money into longer-term deposits.

At least one missing ingredient is the willingness of the central government to offer any real compromise on the three red line restrictions on developer finance that kicked off this property downturn in the first place. For almost a year now, officials have been saying that banks shouldn't be overly cautious in lending t0 property developers. Those calls haven't been enough, with the continued deterioration in conditions in the sector triggering the mortgage strike. In reaction to that, the government has been talking about using SOEs or development banks to provide finance to ensure the completion of unfinished products. But reports so far suggest these proposals continue to be made in the spirit of “not rescuing developers” or “stimulating the markets”.

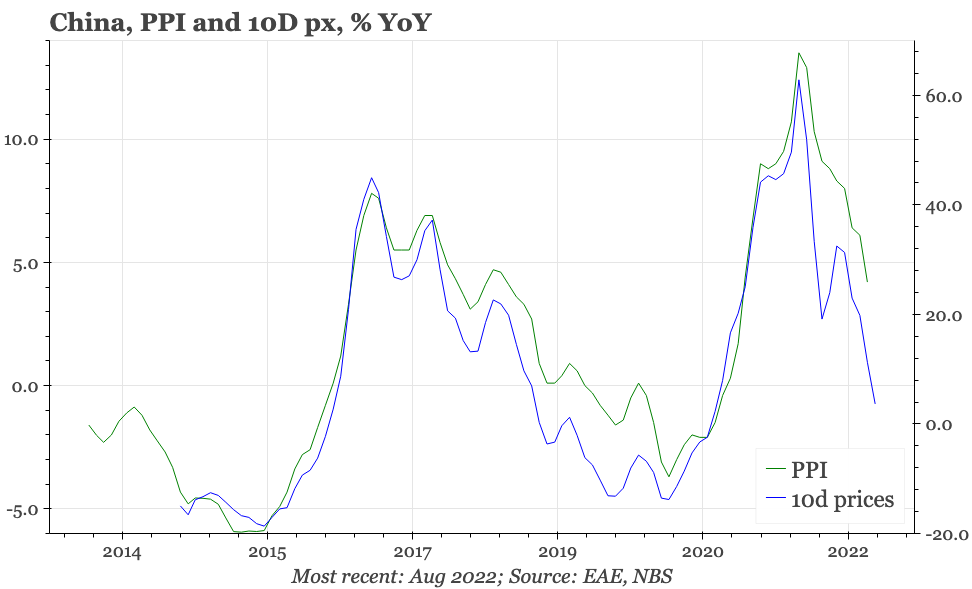

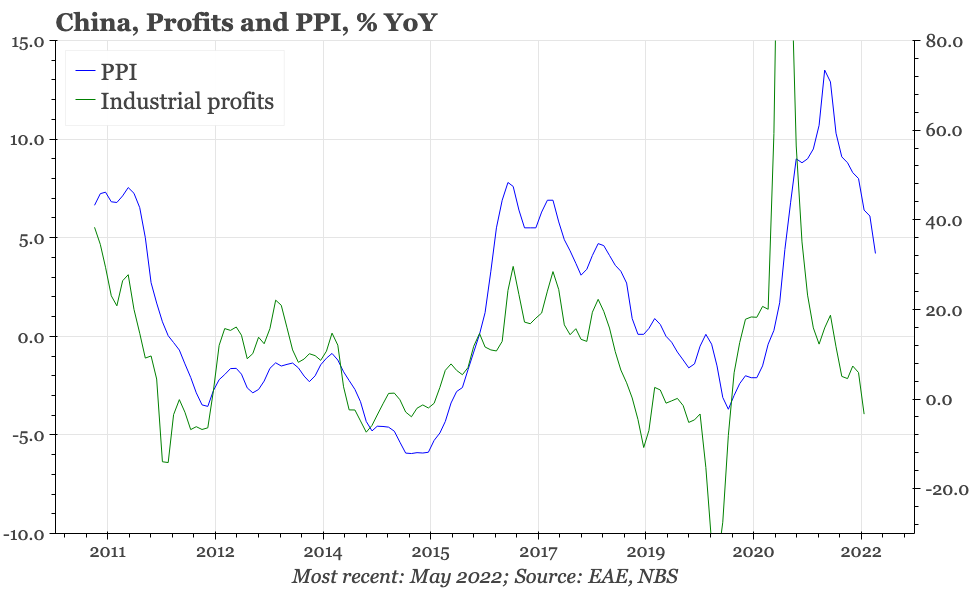

Again, the weakness of property isn't particularly new, but it is starting to matter more as other sectors of the economy begin to weaken. One example is heavy industry, with producer prices falling quite sharply, and a variety of indicators pointing to more weakness still to come. That is already depressing upstream profitability, with steel prices low enough now to cause losses in the industry for the first time in the last couple of years. The weather-related power shortages now being seen don't make conditions for heavy industry any easier. Heavy industry is important enough that this deterioration likely means a down cycle in earnings of the industrial sector as a whole.

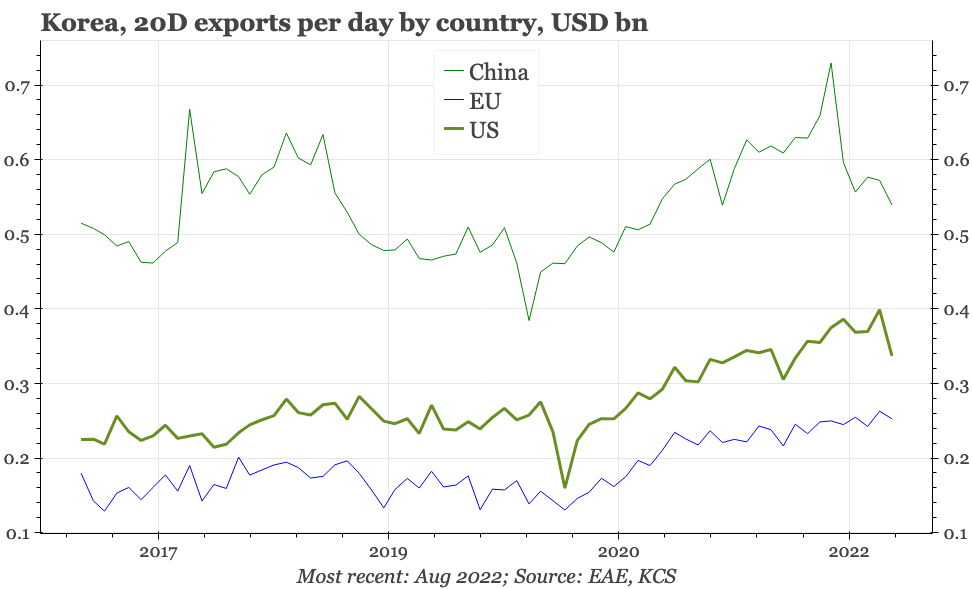

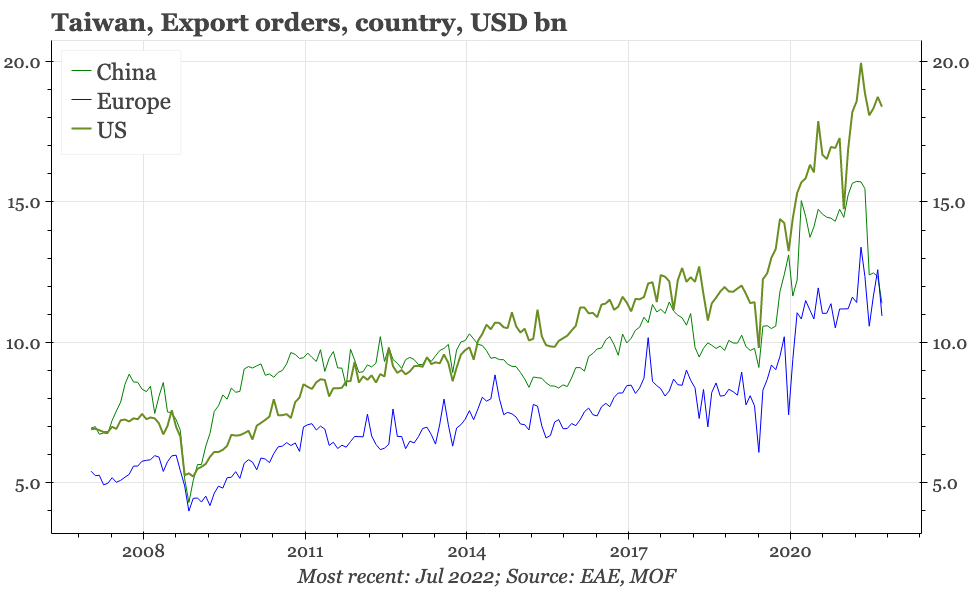

The export cycle also continues to slow. Korean export data for the first 20 days of August and Taiwan July export orders, both released today, are a sign that regional YoY export growth is at best around zero. They also show for the first time some weakness in shipments to the US. This has implications for China, given the export cycles of individual economies in Asia tend to be closely correlated.

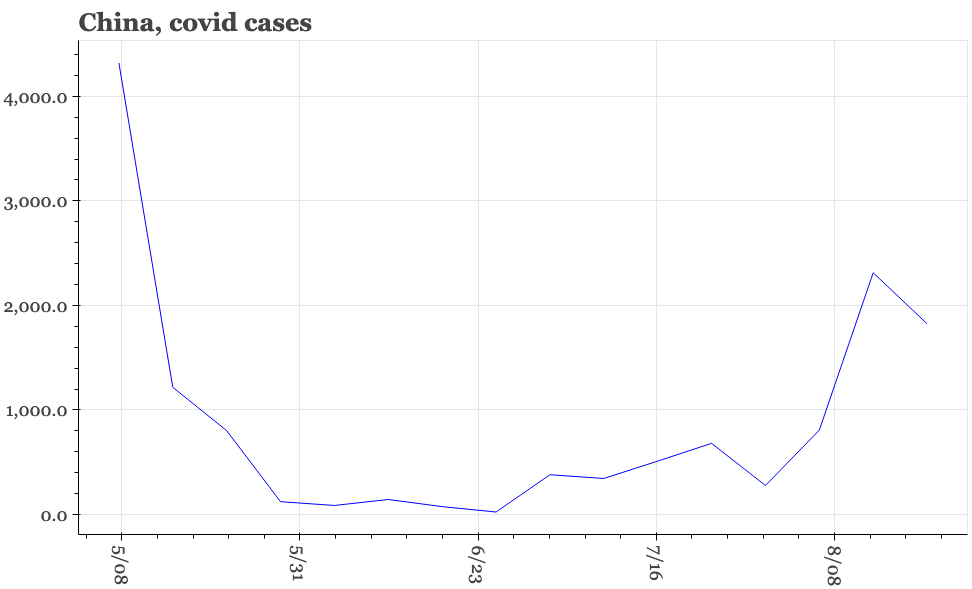

In addition, consumption continues to struggle, and is highly unlikely to turn up at least until China exits zero covid. The current stance towards the pandemic affects consumption in two ways. When there are localised outbreaks (and the nationwide case count yesterday, at almost 2,000, remains relatively high), activity in individual areas of the country is dampened by the measures local governments use to try to push the number of cases back towards zero. Even when covid numbers do fall though, consumption will likely remain sluggish: services spending in China never rebounded to pre-pandemic levels of growth even in the periods the country did record zero cases in 2020-21.

I do worry a bit that sentiment, as it was back in early June, is now overly depressed. At least to outside observers of China, the weakness in the economy, and the risks of further deterioration, are well understood. If the sentiment that premier Li Keqiang continues to express, that economic development is key, continues to be widely shared among policymakers in Beijing, then it would mean a positive policy surprise is coming. To my mind, that would be in the form of some tangible shift that finally puts a floor under property developers, and real support for households and consumption.

That is a real risk. But it isn't the base case because it isn't clear that everyone in Beijing does share Li's priorities. Indeed, in the formulation that usually appears in official statements these days the government has not one but three main aims: controlling covid, economic development, and “security”.

Academics argue that consensus around these new priorities resulted from a debate within the party over the course of the last few years. That is the way policy works in China, but it does seem the security aspect is more closely associated with Xi Jinping than Li. Perhaps the differences are more of emphasis than substance, but there's been enough in the headlines in recent days to keep alive the idea that some sort of differences of opinion do indeed exist.

So, after the quiet period as the leaders withdrew to the usual summer conflab in Beidaihe, Li re-appeared with a tour of the export, manufacturing and tech-led province of Guangdong, where he paid a public tribute to Deng Xiaoping, and spoke (as usual) about reform. Xi meanwhile went to the north-east province of Liaoning, traditionally known for heavy industry, where he talked about CCP military victories in the civil war, common prosperity, and self-reliance.

Whatever the extent of these policy differences, it remains the case that policy continues to lack real force, particularly given the extent of the downside pressure the economy is facing. Until that changes, it remains likely that the drift lower in interest rates persists. There's also a real risk of another step-down in growth at some point in the remainder of the year, which would likely destabilise the CNY and so transmit China's economic slowdown more clearly to the rest of the world.