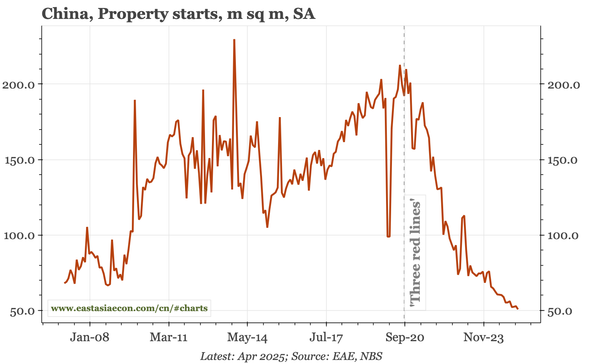

Public Post China – still no sign of property momentum After a clear improvement from September, property price deflation since December has settled at an annualised pace of around -1.5%. Sluggish mortgage lending isn't pointing to a further recovery from here. On these official data, average prices are now down 6% from the peak in 2021.

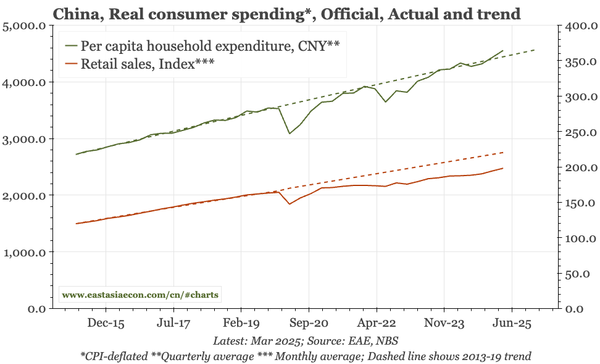

Public Post China – policies to boost consumption The second of two videos on consumption, an issue that is even more important given the economic damage that will be inflicted on China by the tariffs. It is impossible to imagine Beijing supporting western-style consumerism. But there is still a way for economic policy to boost consumer spending.

Public Post China – five consumption myths The first of two videos on consumption. This one looks at recent trends, arguing spending has been stronger than often realised. It still isn't high enough, especially given the huge shock from Trump's tariffs. So the second discusses policies that would boost consumption further.

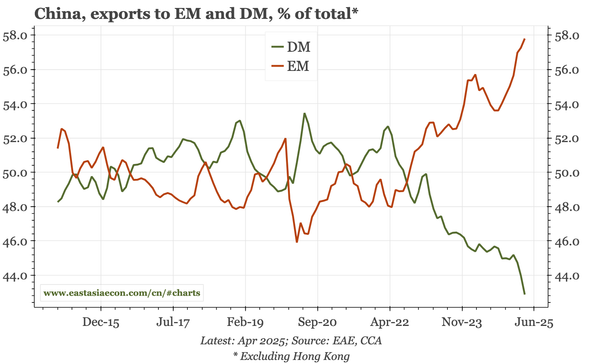

Public Post China – three post-tariff themes Yesterday's tariffs are close to a worse case scenario for China, and are a big negative shock when the cycle is already weak. Three things strike me as important in what happens next, both for China's economy, and for its global influence: consumption, imports, and the currency.

China – not undergoing Japanification In recent months, I've been doing quite a lot of work on Japanification. I summarised the arguments in this opinion piece for The Wire China.