Subscribers Only

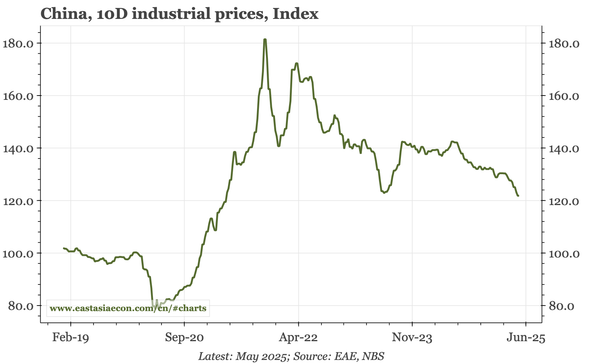

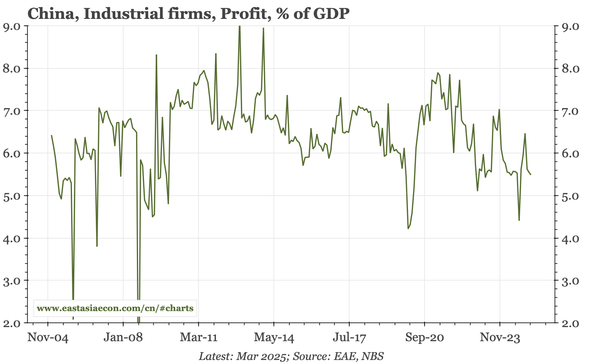

China – deflation isn't just about industrial over-supply

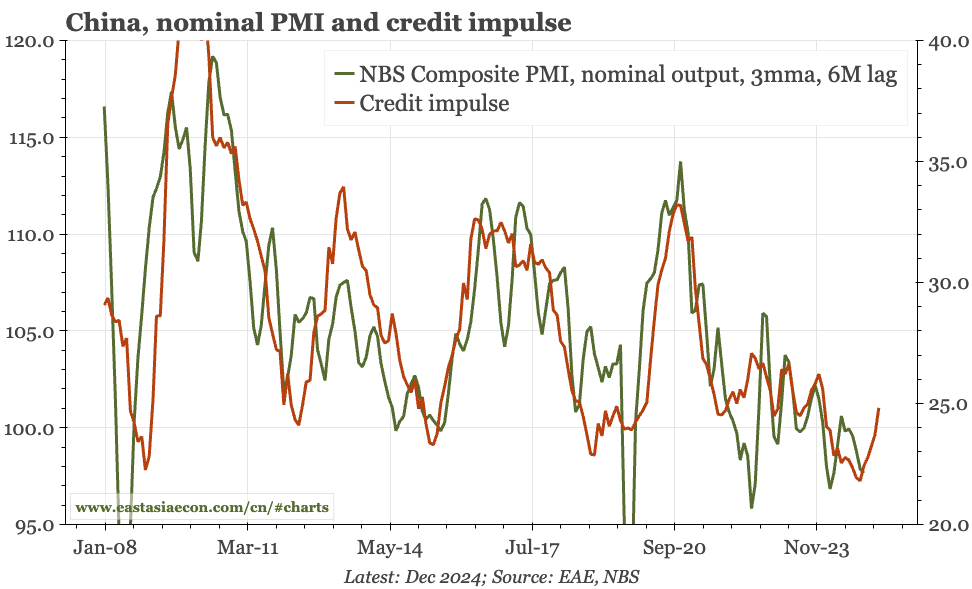

Markets have perked up on hopes that officials will tackle over-supply. But belated publication yesterday at 8pm (!) of the PBC's quarterly opinion surveys is a reminder that business involution isn't the only challenge. Household price, income and employment expectations all continue to fall.