Subscribers Only

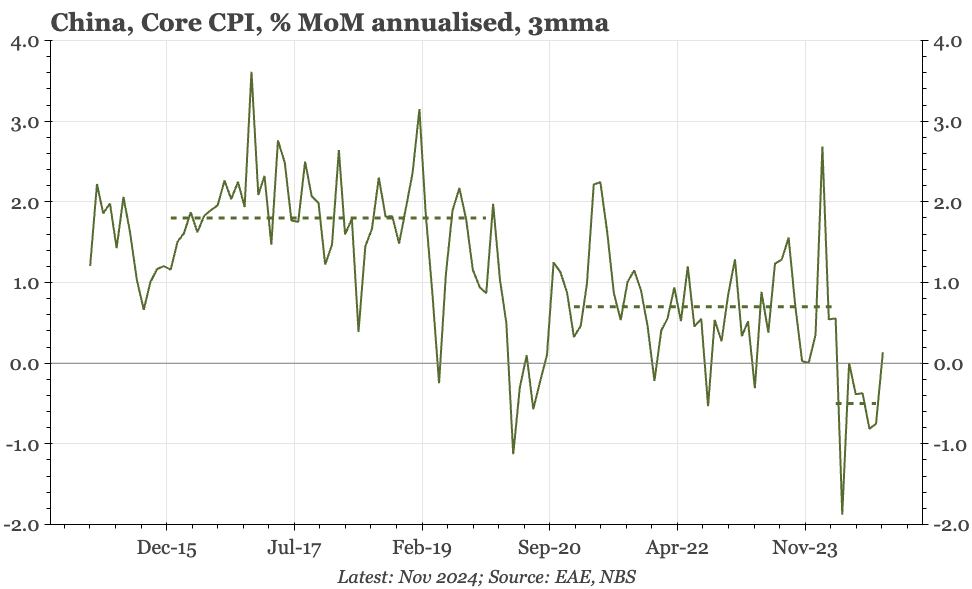

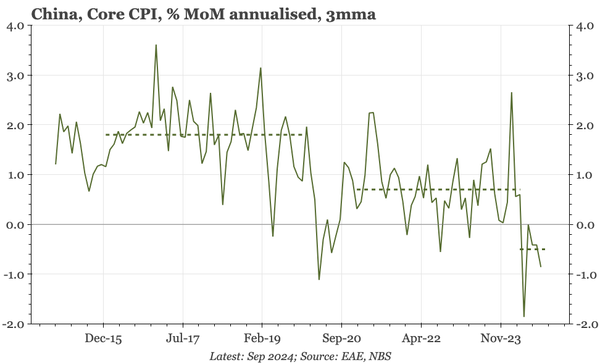

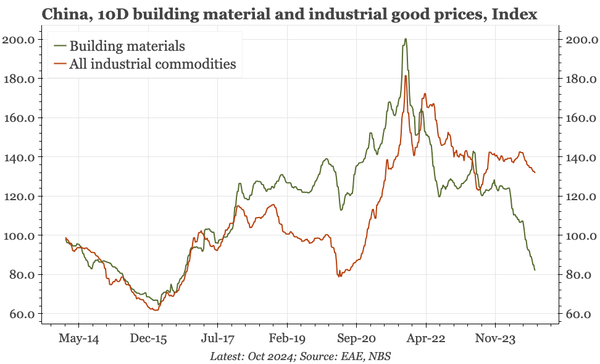

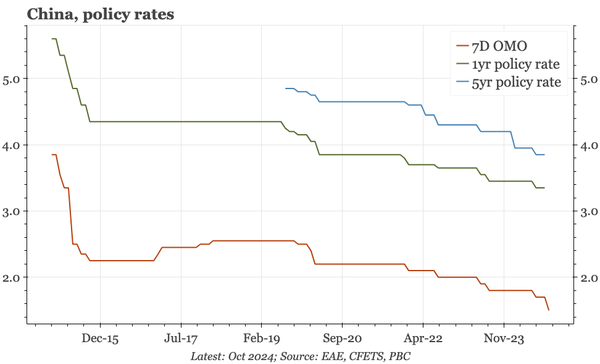

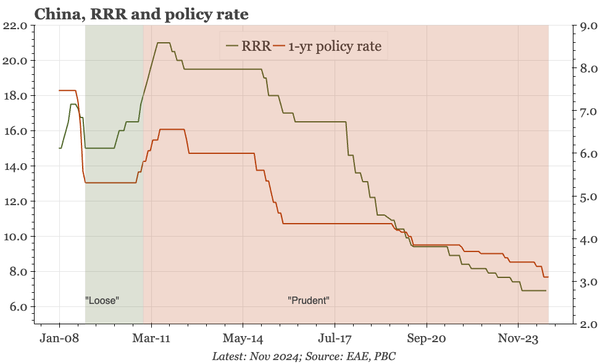

China – what might "moderately loose" mean?

A "moderately loose" stance seems encouraging. But effecting that isn't straightforward, given nominal rates and the RRR are now so low. Rather than nominal, policy needs to work on price. That can be done by PBC BS expansion that addresses property inventories, or fiscal policy that raises demand.