Subscribers Only

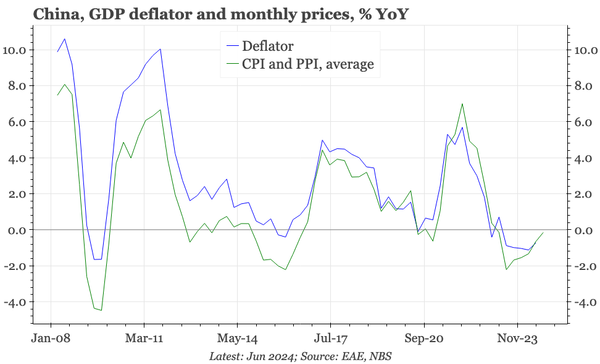

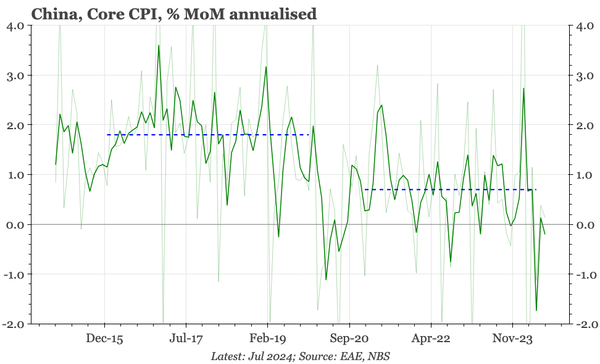

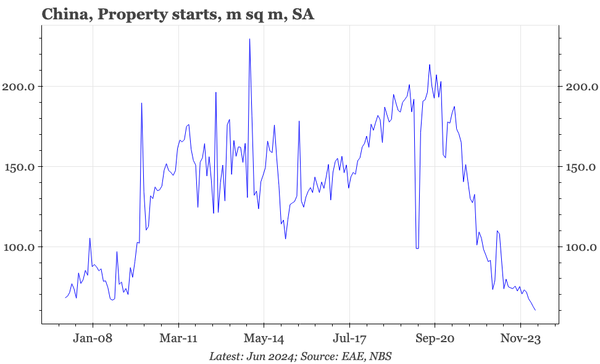

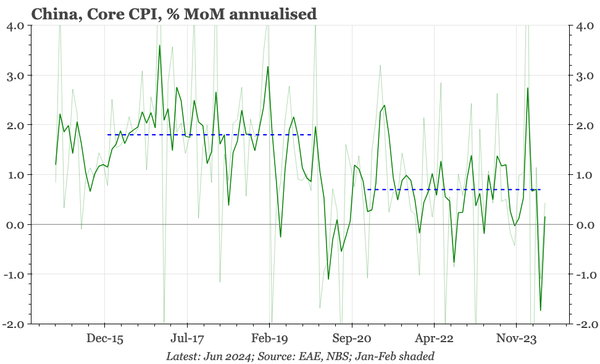

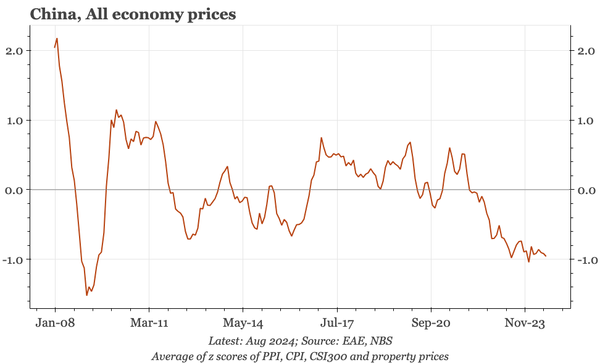

China – still stuck in deflation

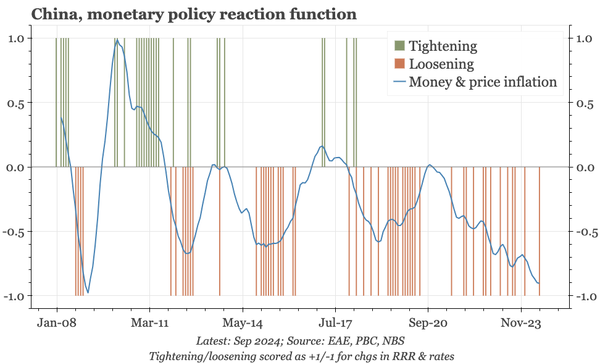

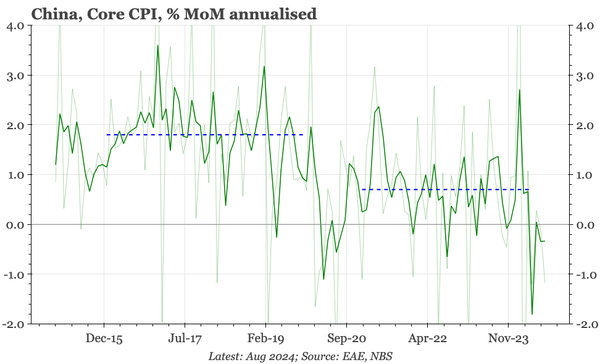

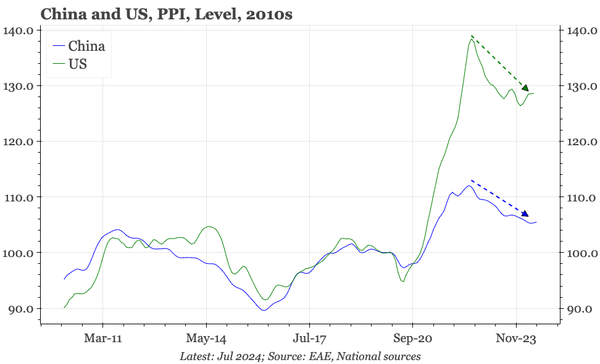

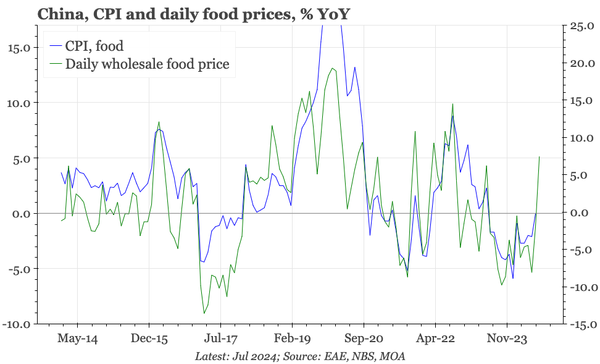

Today's industrial price data for the first 10 days of September and property prices for August show intensified deflationary pressure. Yesterday's monetary data were weak. The PBC said yesterday that it will focus on price stability, but it also said it has plenty of other things to do as well.