Subscribers Only

China – stronger nominal momentum

1) Goods and services output growing ~5% is enough for Beijing; 2) money and credit growth don't suggest a lot of change in that underlying trajectory; 3) nominal momentum is improving, with an end of PPI deflation now a real possibility; 4) the likelihood of further monetary easing is falling.

Subscribers Only

China – semiconductors lift exports

Exports in YoY and SA terms were strong in Jan-Feb. That looks too good to be true, and I'd expect new year distortions won't totally disappear until March. Still, one trend that looks real is the rise in chip exports, as China benefits from the same semi super cycle lifting the rest of the region.

Subscribers Only

China – the end of deflation

Deflation momentum continued to lessen in February, a trend that will now be given a further boost by global oil prices. But with this shift in the direction of deflation being driven by external factors, it isn't based on the sort of improvement in domestic growth that is needed for sustainability.

Subscribers Only

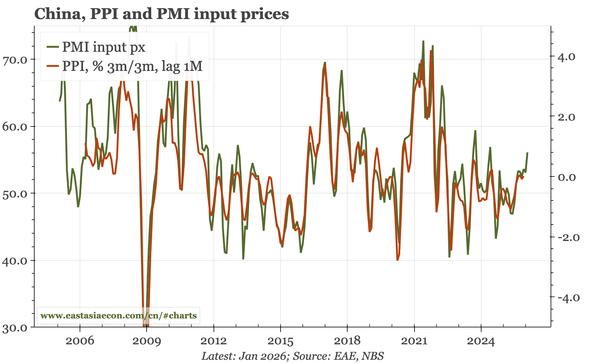

China – PMIs diverging more than usual

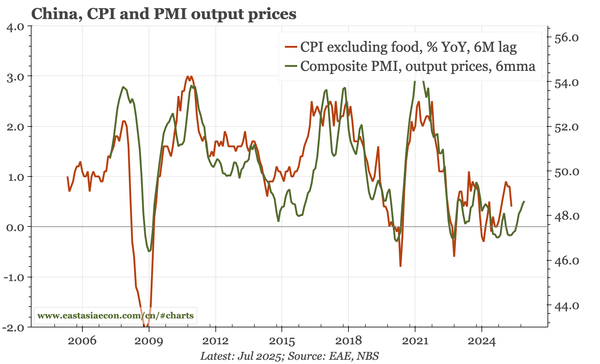

The S&P/RatingDog PMIs suggest an economy that is finally recovering. The official PMIs, by contrast, indicate continued sluggishness. I am inclined to think there is no change, at least until the LNY impact fades. The one common theme is firmer input prices, even before an energy price shock.

Subscribers Only

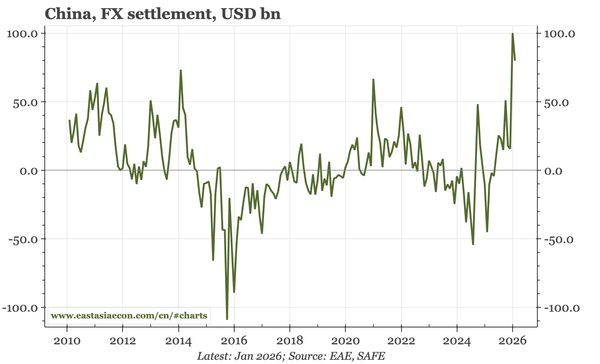

China – big inflows, sluggish domestic

January fx settlement data suggest large fx intervention for a second consecutive month. One reason is the CA surplus, which other data today show widened in Q4. Another is interest rates which are more stable, even though monetary trends aren't changing much, and property prices continue to fall.

Subscribers Only

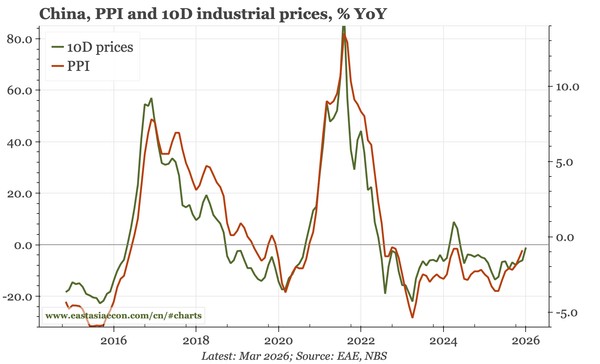

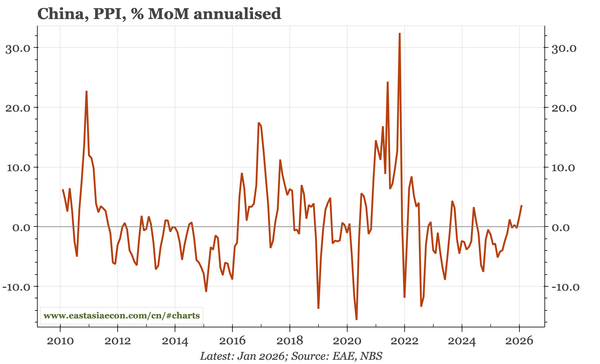

China – PPI up again

CPI inflation softened in January, but it always does when the new year holiday falls in February. PPI has less seasonal distortion, and rose MoM in January for the second consecutive time. The GDP deflator is likely to improve again in Q1. This is about external factors, but deflation is lessening.

Subscribers Only

China – some nominal momentum

Today's official PMIs were below 50. That shows the domestic economy is weak – though the data were likely pulled down by the coming holiday. More interesting was the further rise in prices in manufacturing. That change relates to USD/global prices, but does suggest an upturn in nominal momentum.

Subscribers Only

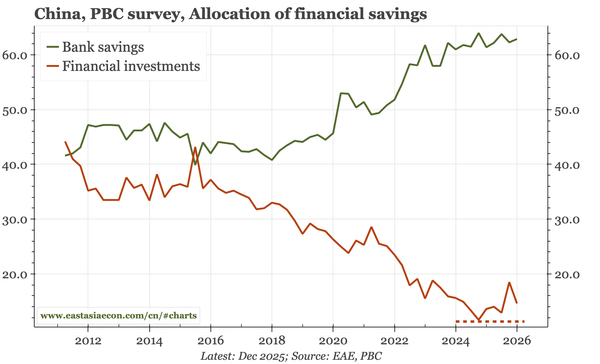

China – the end of the flight to safety

Like the actual monthly deposit data, Friday's PBC Q425 depositor survey shows a slowing of the flood of household savings into the safety of bank deposits. The structural deflation pressure caused by the collapse of real estate activity and the chaos of the covid lockdowns is beginning to ease.

Subscribers Only

China – nominal pick-up

Most important for markets is today's Q4 data is the pick-up in the deflator and nominal GDP, which external trends suggest can run further. In terms of the details, the data show two big discrepancies: collapsing FAI v industrial stability, and falling retail sales v rising consumption share of GDP