China – softer again

Property prices and sales, investment and retail sales all deteriorated in July. It is at least possible to argue that the worst of the drop in property activity is now completed. That creates room for second-derivative improvement, but even that could be offset by slowing manufacturing capex.

Prices

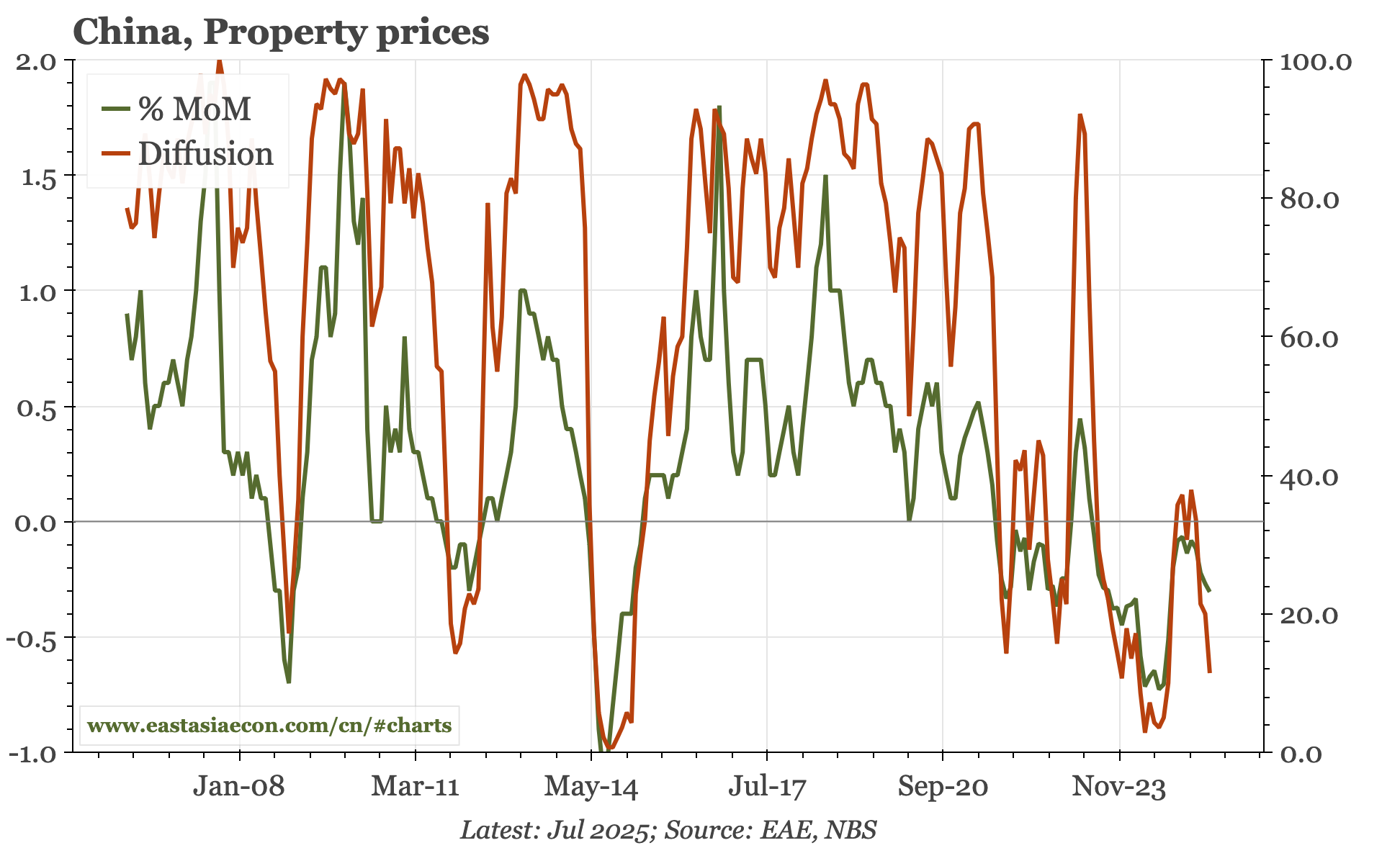

Property price deflation once again accelerated in July. Based on official data, average nationwide primary property prices are now back to the same level as early 2019 – though the fall in reality has likely been bigger still.

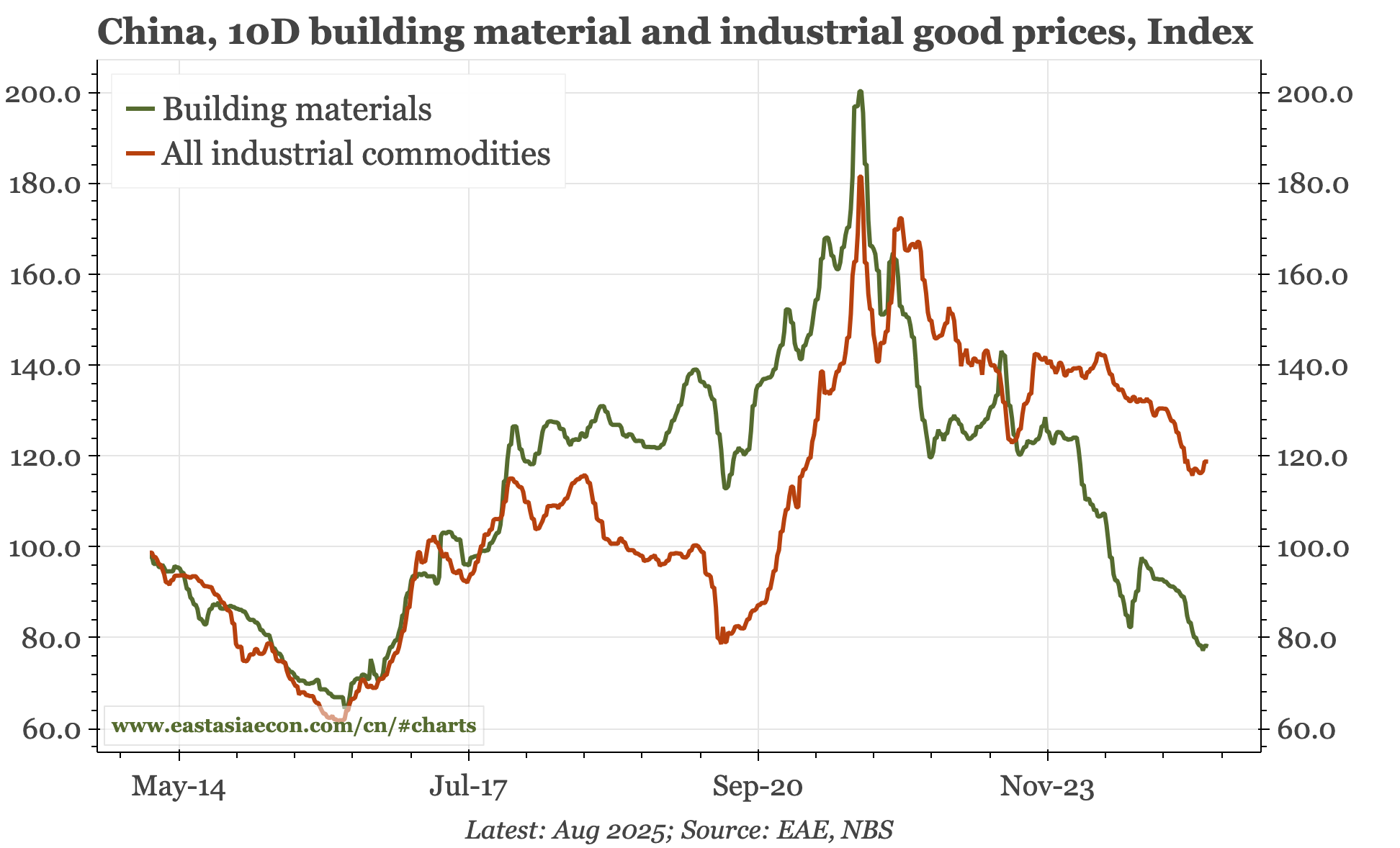

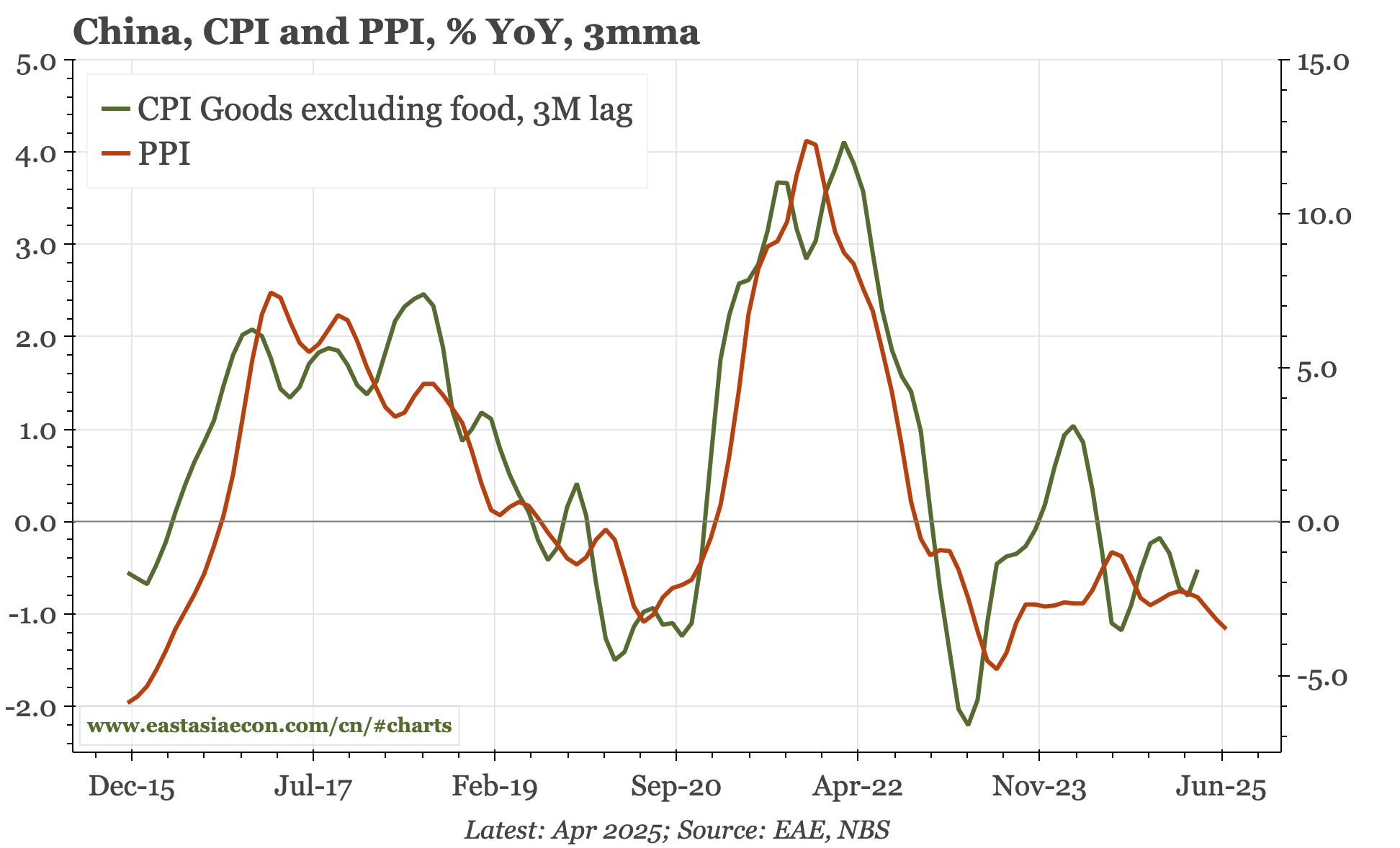

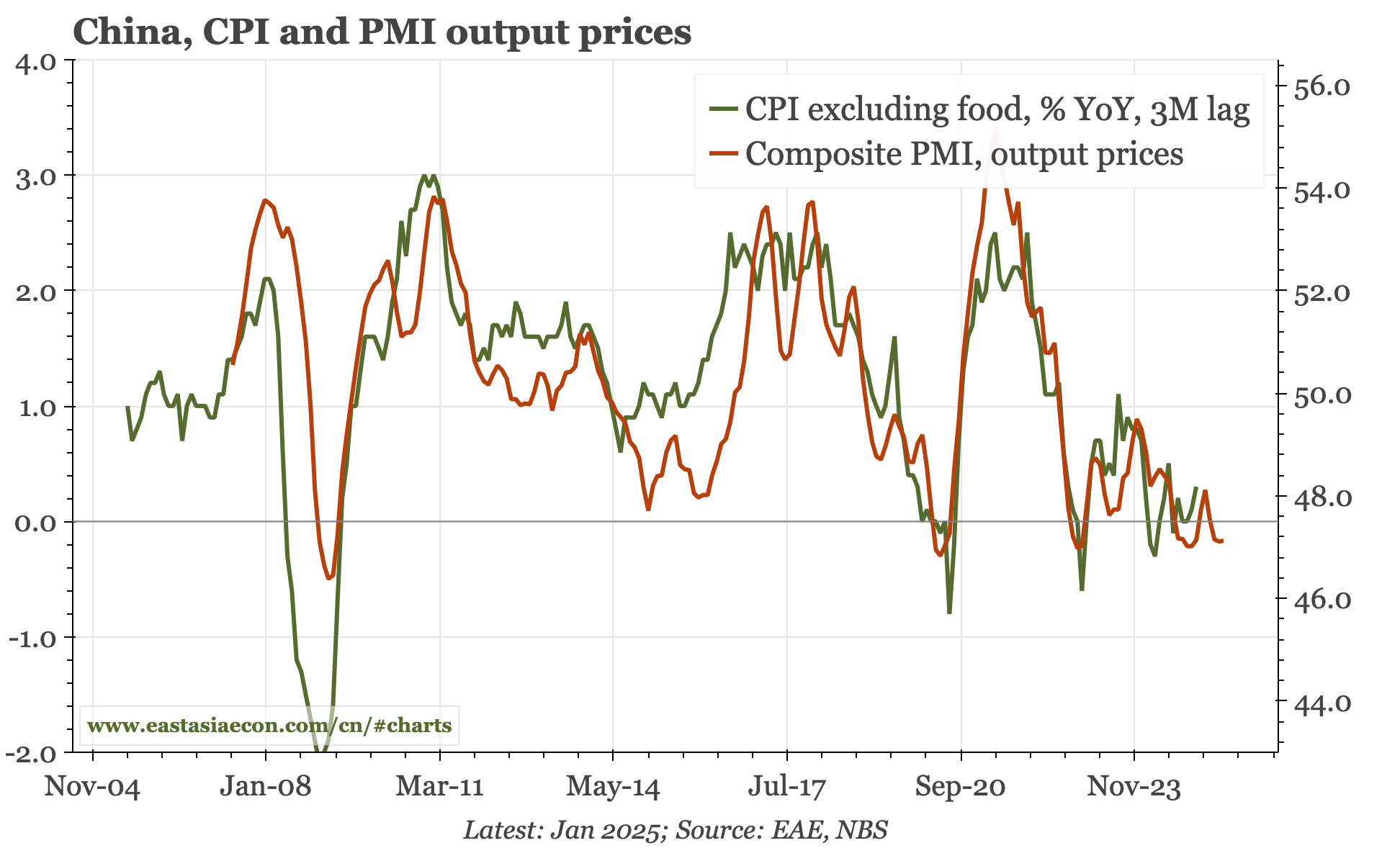

With equities rising and PPI and CPI not changing much, all-economy deflation isn't worsening. But nor does it show any improvement. High-frequency data so far through August show a very mild rise in upstream commodity prices, but again, not one that is big enough to signal a change in direction.

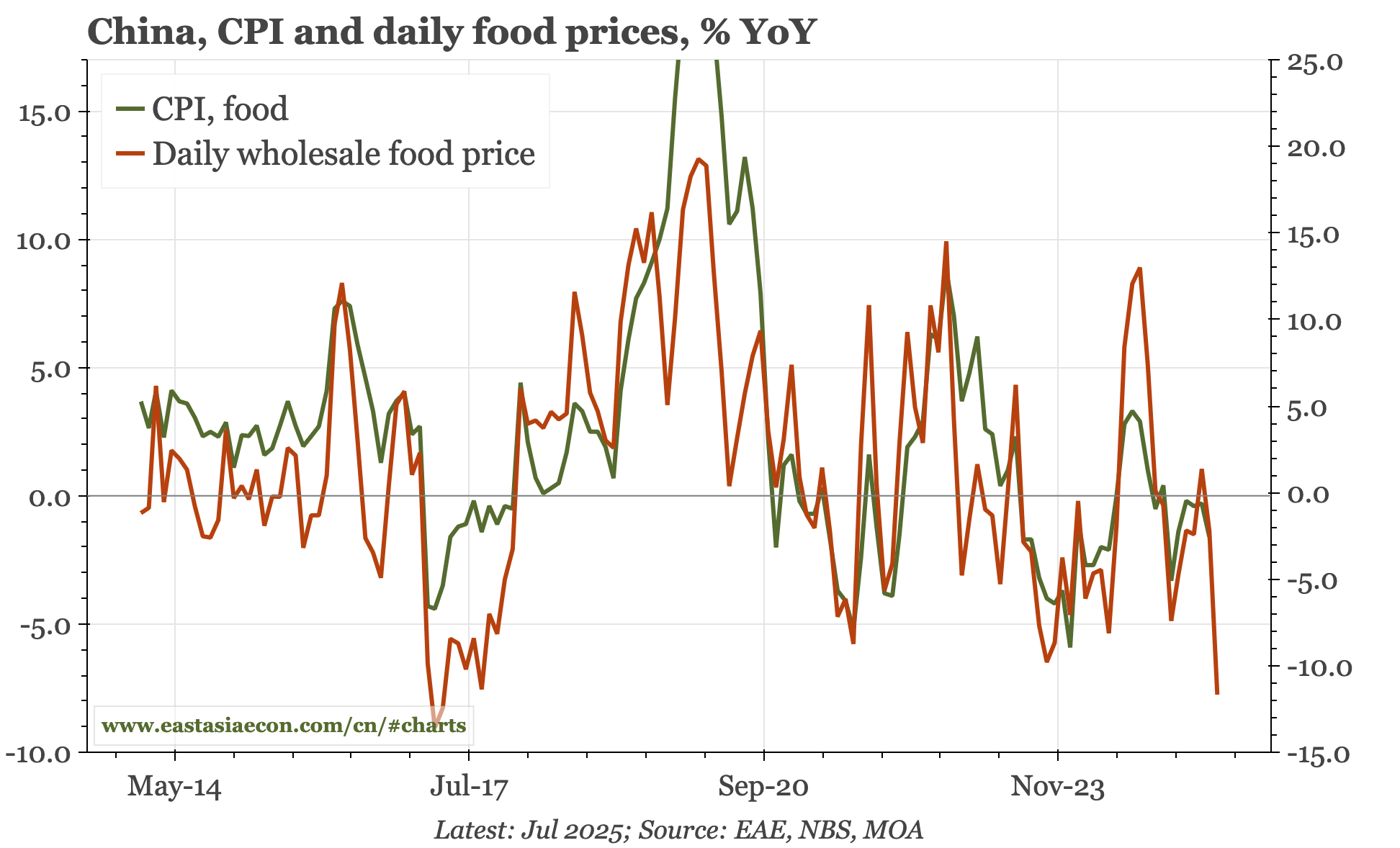

Wholesale daily food prices, meanwhile, continue to weaken, signalling that food prices in the CPI will likely fall in August. Both PMI output prices and PPI point to continuing declines in other components of the CPI. All told, the deflationary pressure in the economy isn't shifting yet.

Activity

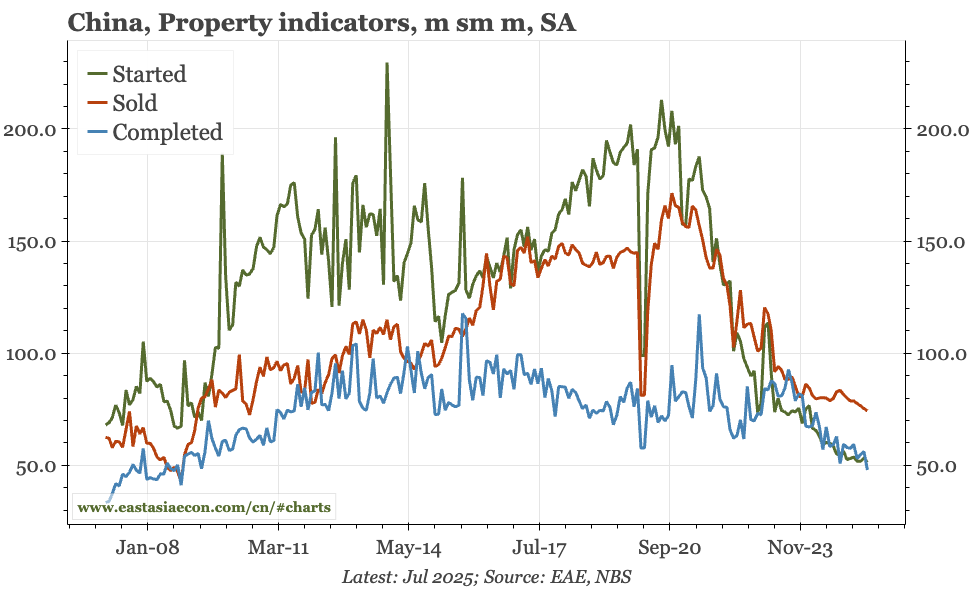

Housing starts do look to have bottomed out, at a level that is a remarkable 75% below the peak of 2020. But it is still difficult to get excited that the overall property market really has reached a floor. After the spurt in early 2023 completions have since been falling. More worryingly for the cycle, property sales continue to record new lows.

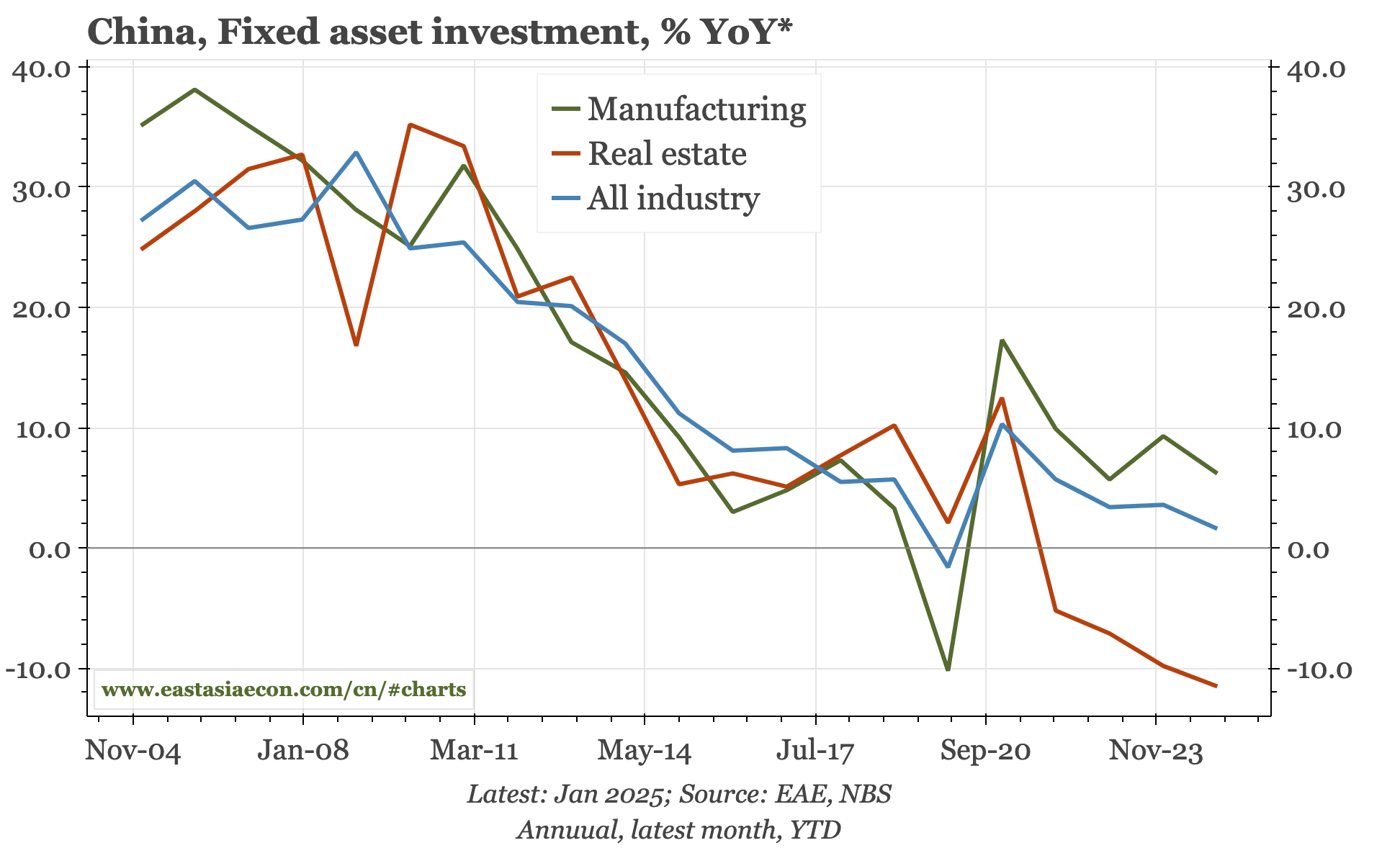

Reflecting that, property investment continues to weaken, dropping -11.5% YoY in the first seven months of 2025, down from -9.8% in the same period of 2024. The rise in manufacturing investment, an acceleration that had helped offset the weakness in property, is now also slowing. If the government is serious about tackling "involution", manufacturing investment should have more downside from here.

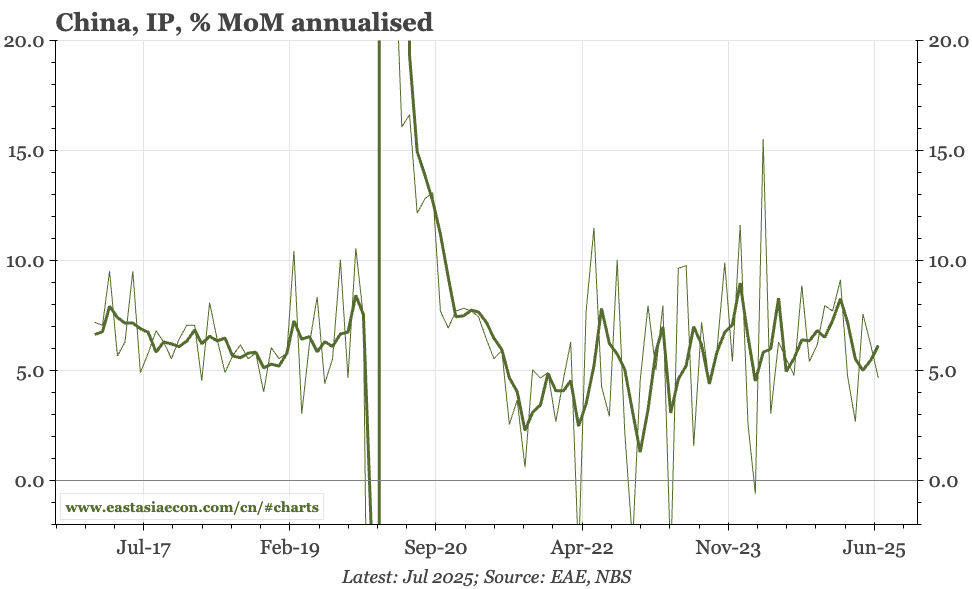

The weakness in domestic construction and investment is a big headwind for domestic industry, though export growth has remained strong. As a result, MoM industrial output growth is running at a bit over 5%. That is down from the pre-covid run-rate, but still reasonably firm. However, IP growth did pick up strongly in 2H24. With that base effect, there is downside risk for headline YoY growth in IP 2H.

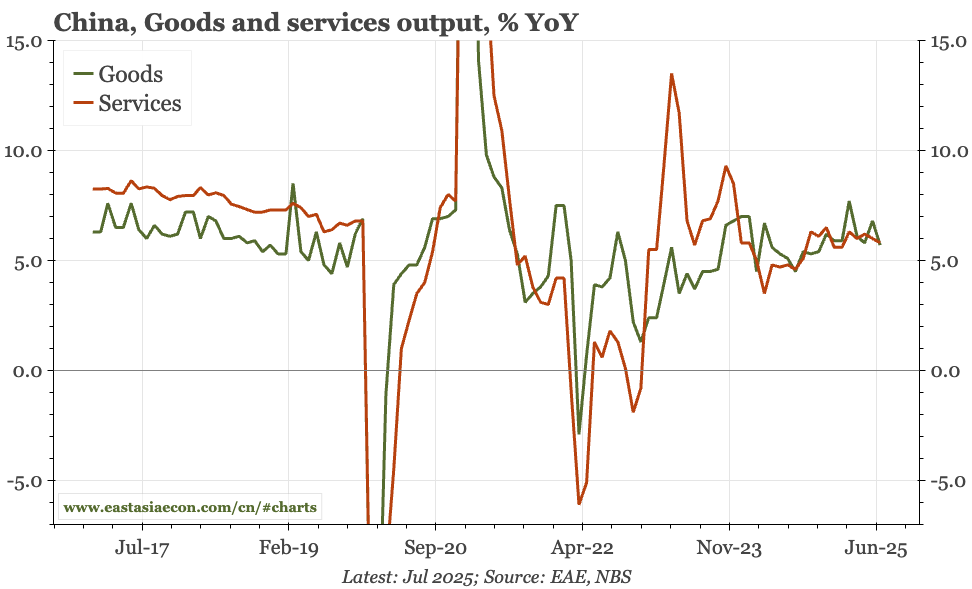

The NBS's statement today talks about "high growth" in services output, led by "modern" sectors like "information transmission, software and IT, and finance". However, YoY growth in aggregate services output– MoM data aren't published – does look to have peaked.

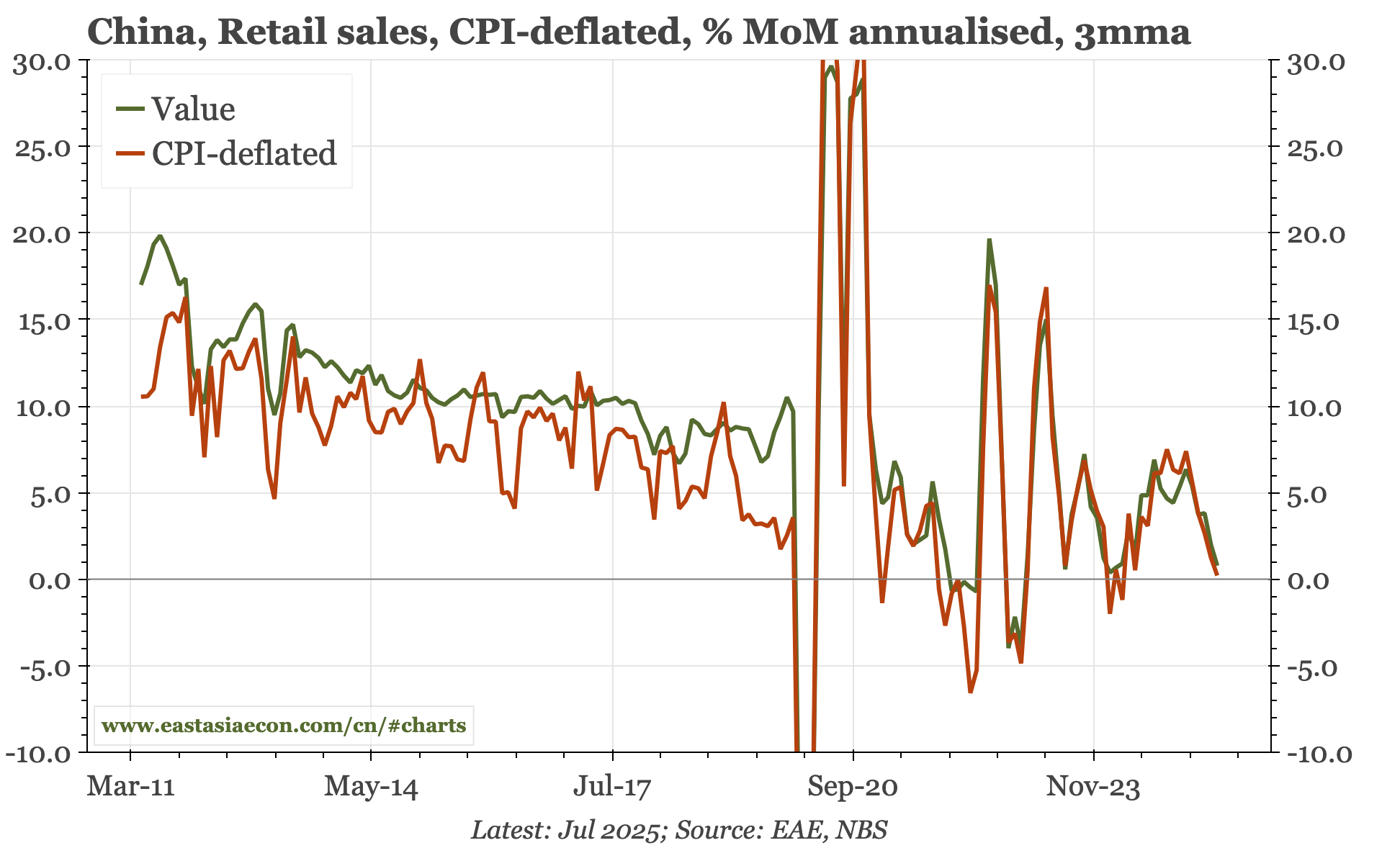

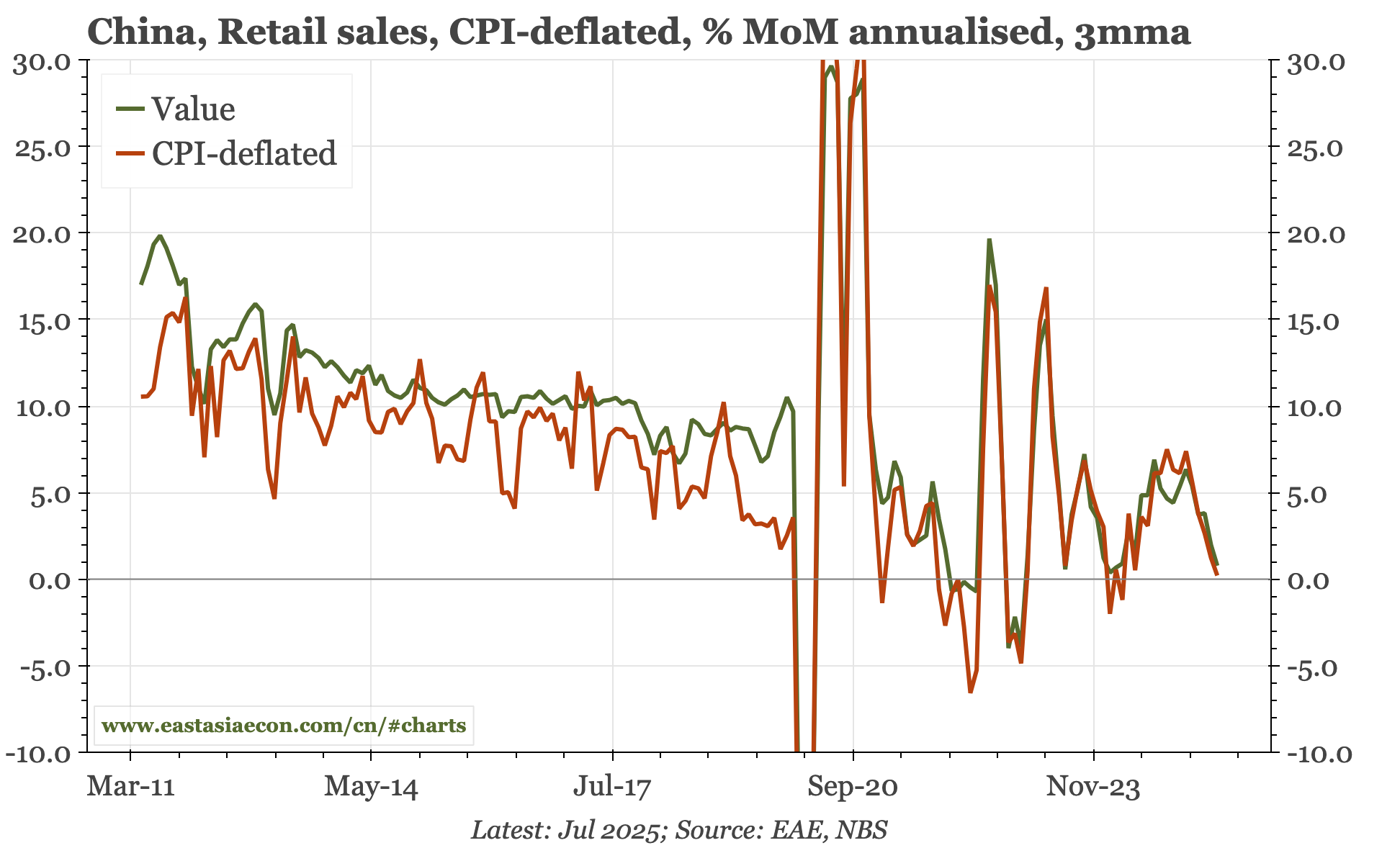

The renewed downturn in retail sales that began in June continued in July, and the drop looks bigger when calculated from the monthly value series than from the official presentation of MoM growth. Part of that is related to the restrictions on official dining, which the government now seems to have relaxed. But goods purchases have also fallen again.