China – is (it still possible) the worst is over?

My latest video, making the case for a bottoming of China's economy. In light of this week's poor official data, the argument might look off-base, which means it should at least be interesting. I do think the logic holds up, but as discussed here, there are reasons I could be wrong.

I recorded this video about three weeks ago, and was worried the message had been overtaken by events. My argument is about the stabilisation of the economy, but after the bad data released by China on Tuesday, some commentators are talking about recession.

If that is the consensus, then the argument should at least be interesting – but listening over it again, I think the case made still stands up. It is presented in three parts: the evidence for stabilisation, the drivers of that, and finally the implications.

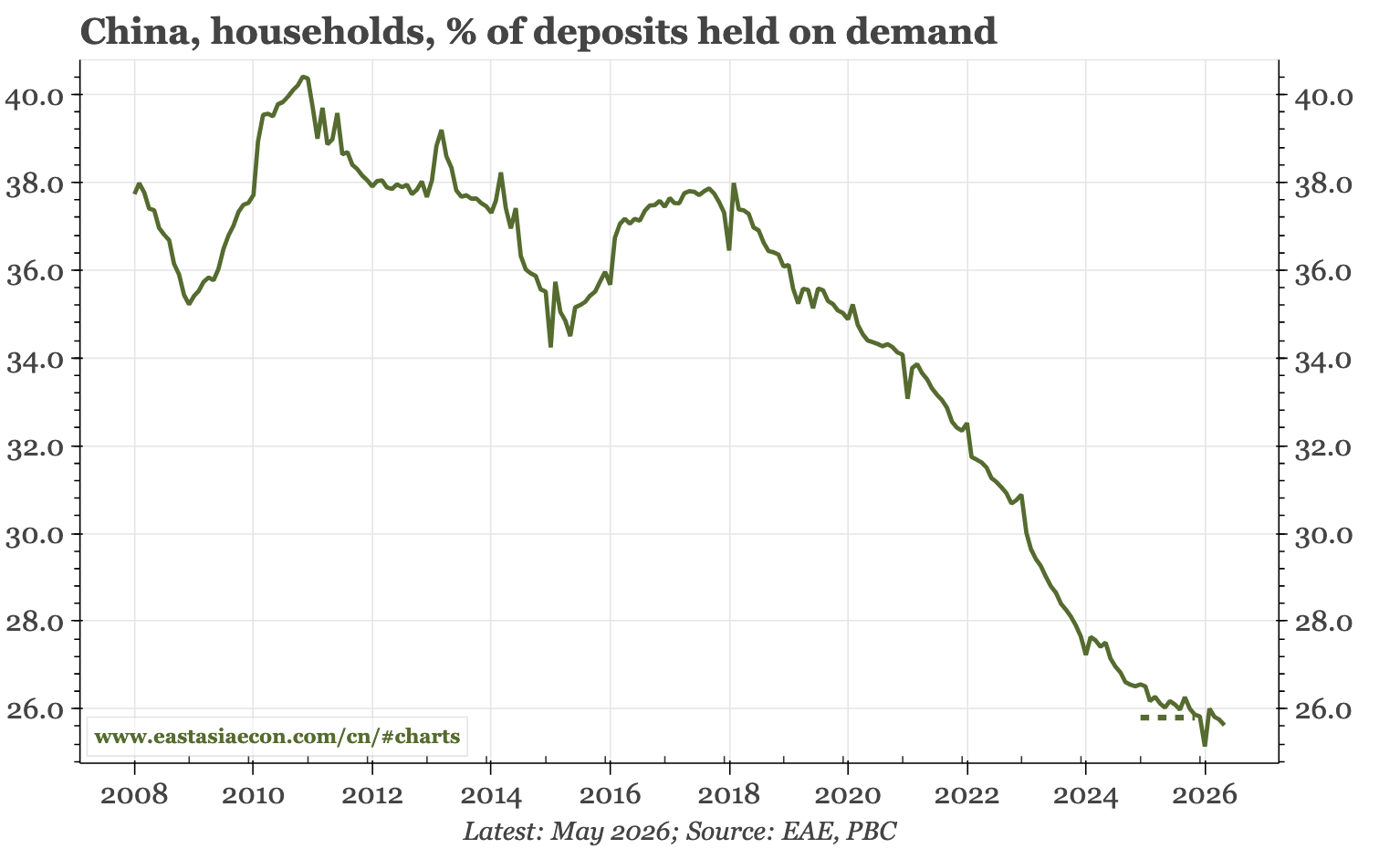

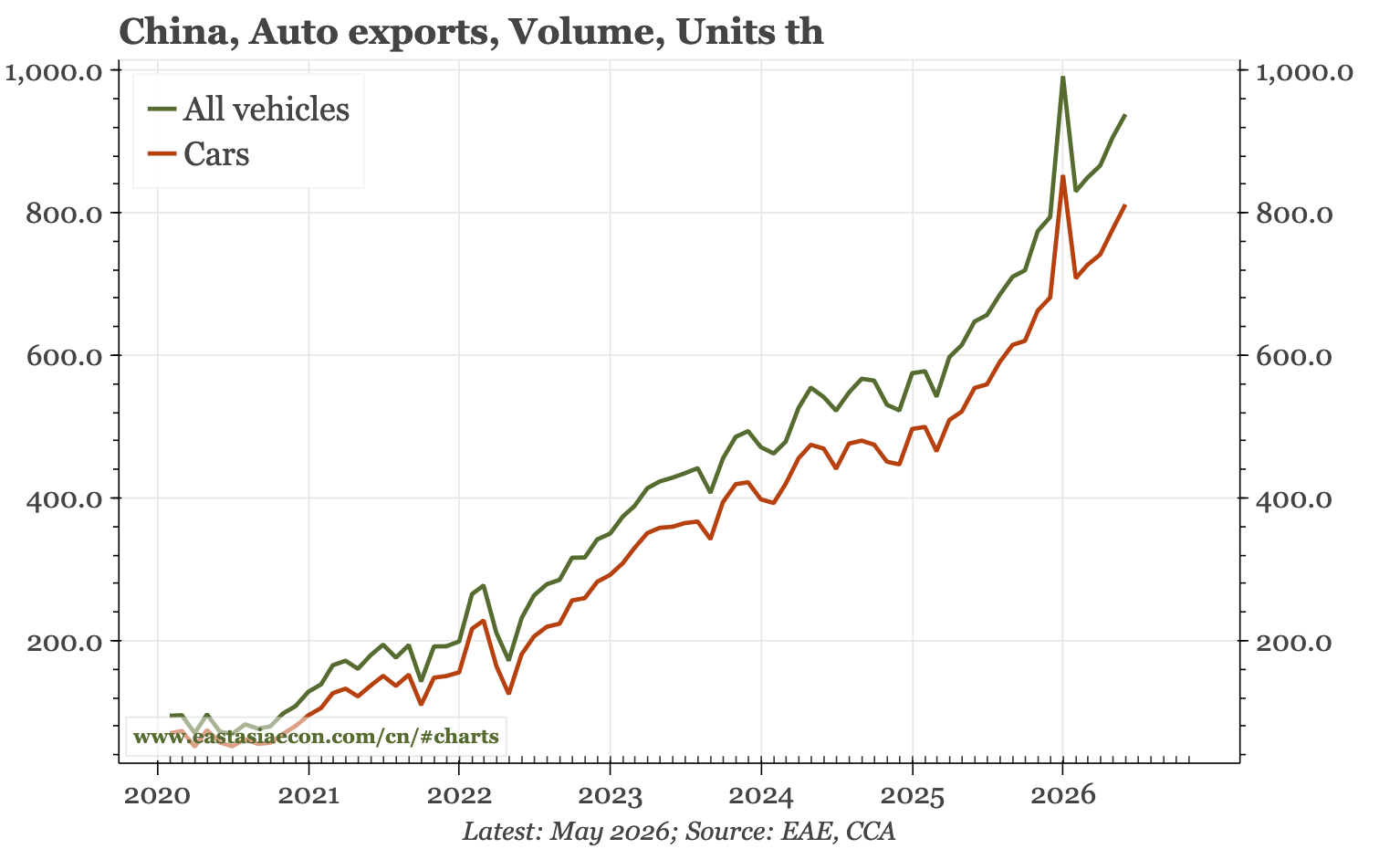

The evidence includes the demand: deposit ratio, inflation and exports. As for the drivers, some are more structural, like the weakness of the currency that has helped exports and lessened the deflationary impulse. Others are dynamic, with the lessening of inflation that began even before the Iran war leading to a slowdown in the pace of monetary easing, and with the big export surplus, triggering capital inflows.

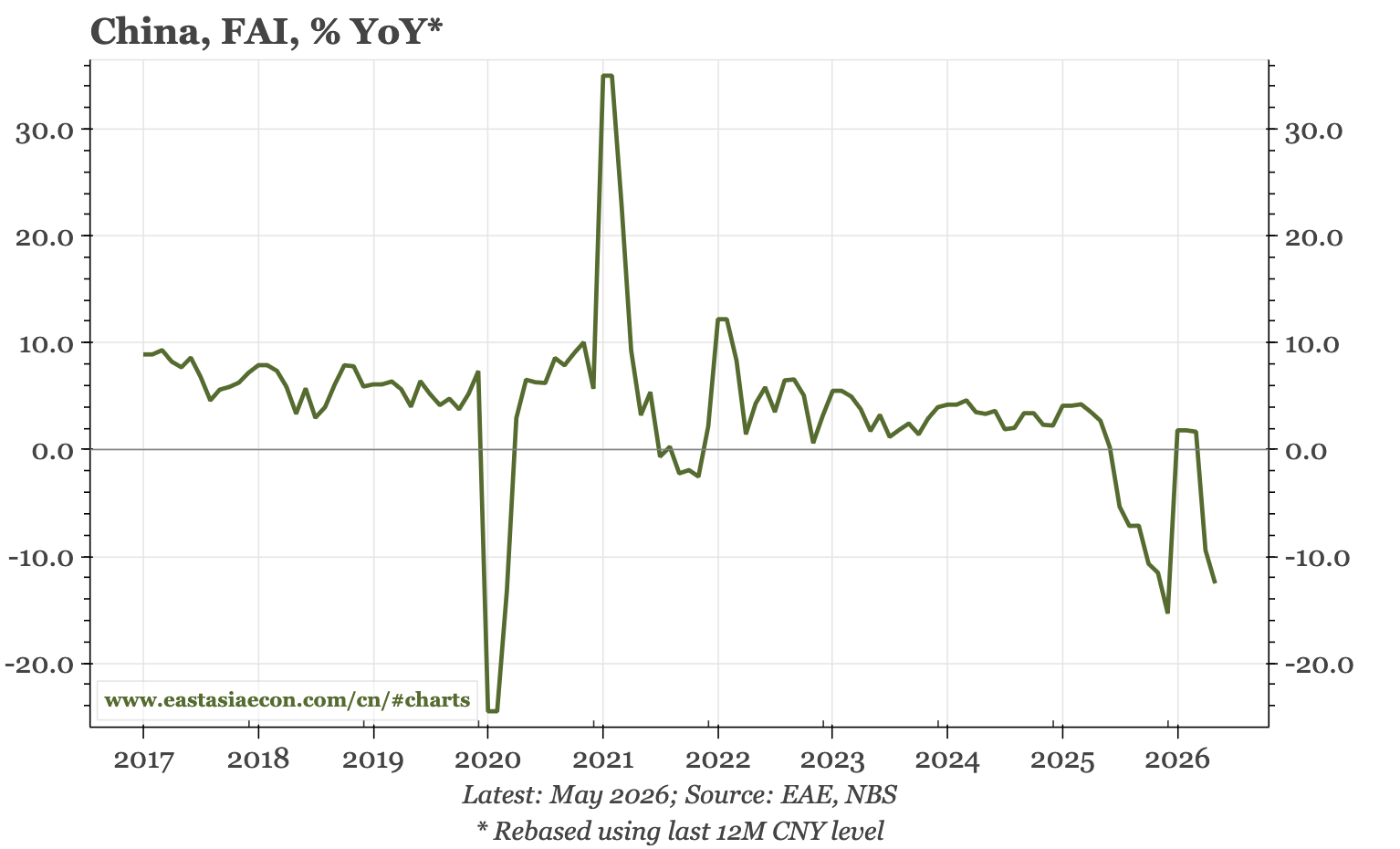

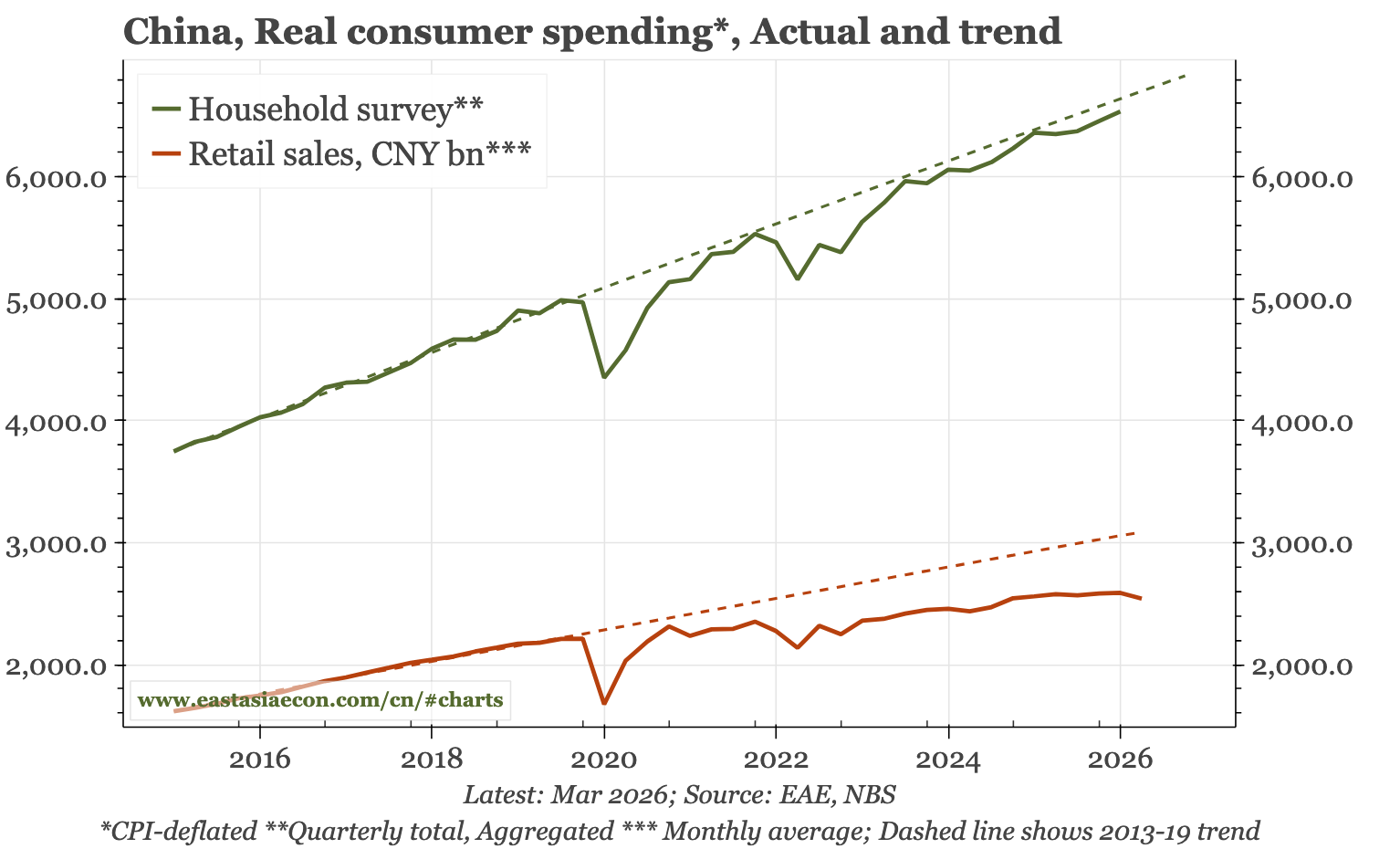

What then to make of the poor data of the last three months? I would dismiss the FAI data are being unreliable. The drop in retail sales is of more concern, and the weakness of consumption is a long-term headwind for the development of China's economy.

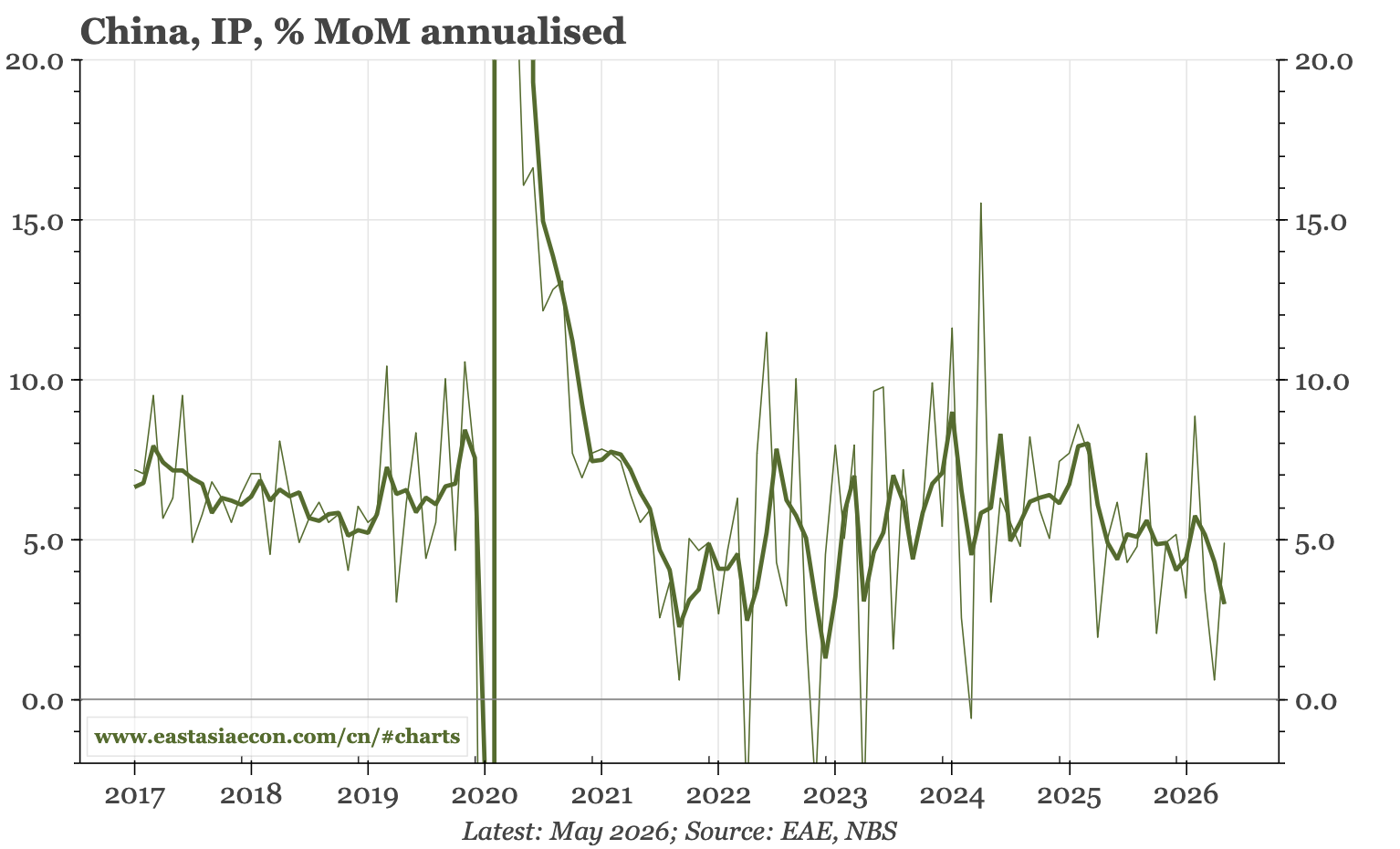

That said, I am not sure that the lack of consumption matters for the short-term. Or at least, I don't think the weakness is significant for the cycle and policy unless if affects industrial production. IP growth did slump in April, but improved somewhat in May. That sequence fits with the start and then lessening of supply disruptions from Iran.

If it is Iran-related problems, then IP should recover further in June. With Japan's data flow this week pointing to a stronger global manufacturing cycle, IP should also continue to get a boost from exports. That external dependence is arguably bad for the rest of the world, but when domestic demand is weak, exports are a key component of China's own growth story.

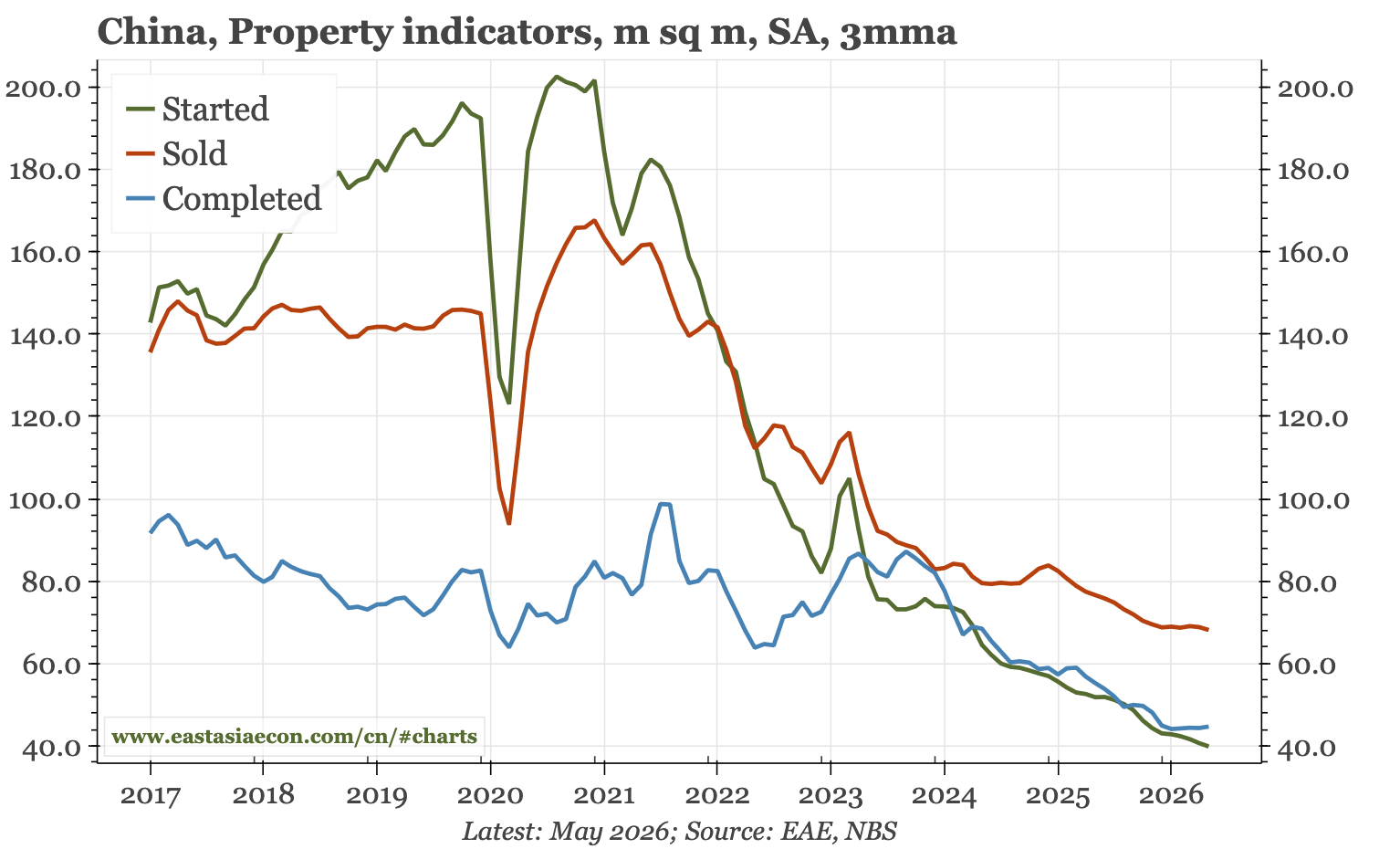

I think getting back to IP growth of 5% is important for the stabilisation argument to be on track. One reason that might not happen is because the weakness in domestic auto sales – which is the standout feature of the recent weakening of consumption – does, in fact, impact domestic output. The other indicators that I would be monitoring are M1, imports and, as always, property. If I am wrong and the economy is turning down again, I would expect it will show up in the CNY.