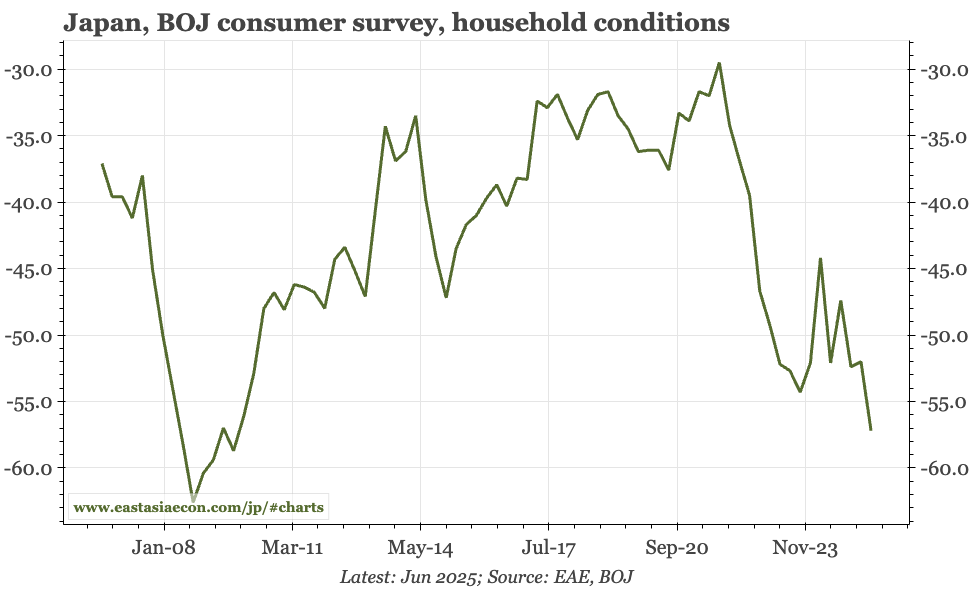

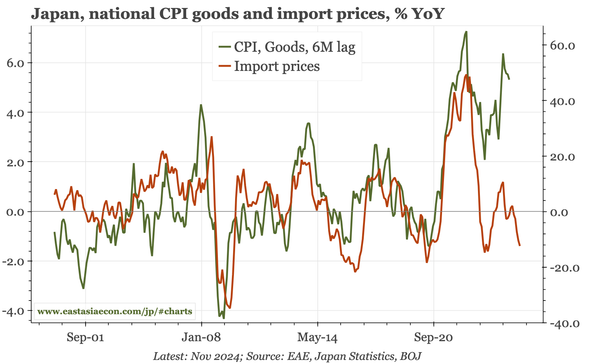

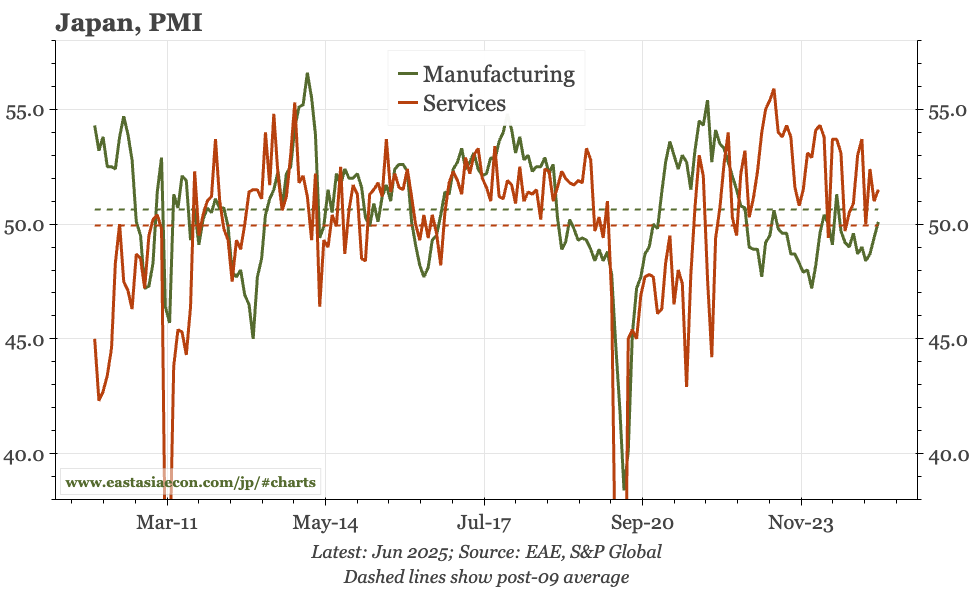

Public Post Japan – three scenarios for the JPY My latest video, discussing the JPY outlook in the context of this year's two shocks: tariffs, obviously, but also the rebound in inflation that caused a new sharp fall in consumer confidence. The risk from US policy is still growing, but, importantly, the rebound in prices is losing momentum.