Subscribers Only

Last week, next week

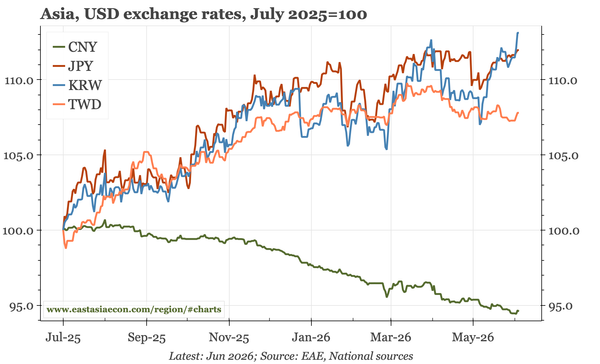

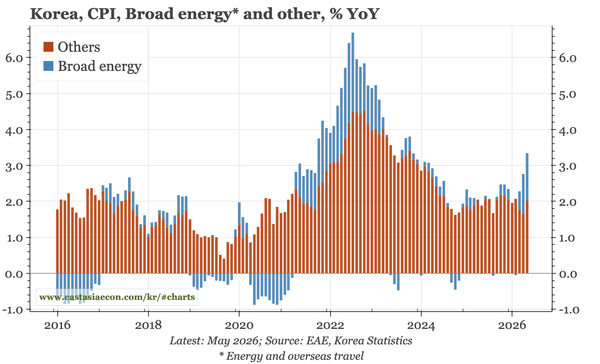

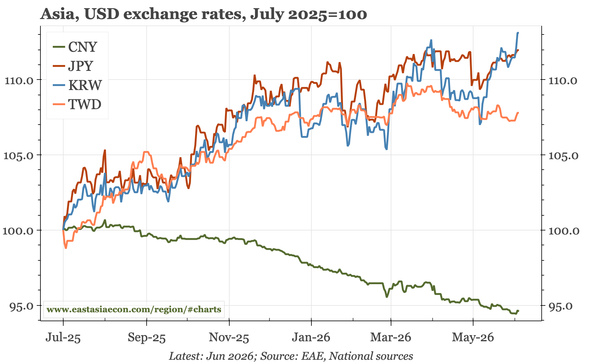

Events in Japan in the next couple of weeks will likely be critical for the region. If a combination of a strong US jobs report and equivocal BOJ meeting push $JPY through 160, KRW and TWD will likely be dragged higher too. The implication would be higher inflation, and more pressure for rate hikes.