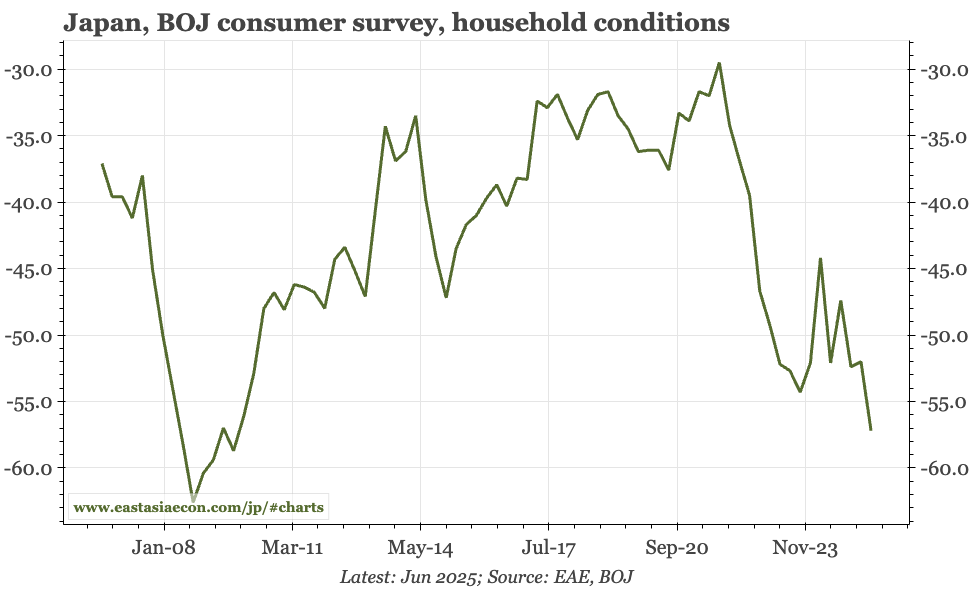

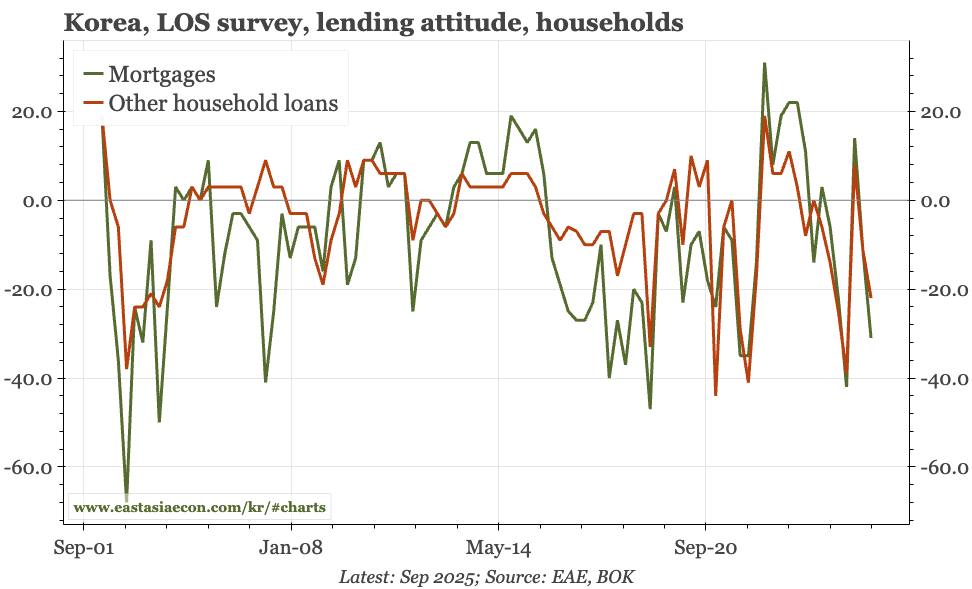

Subscribers Only

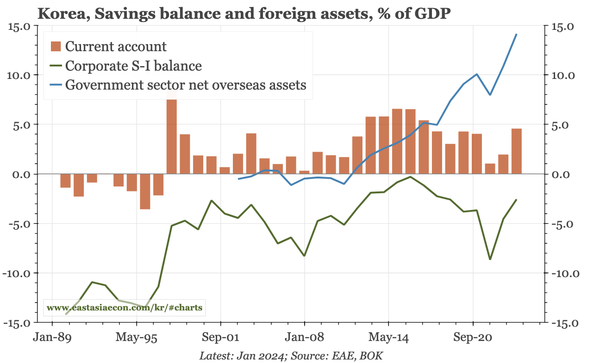

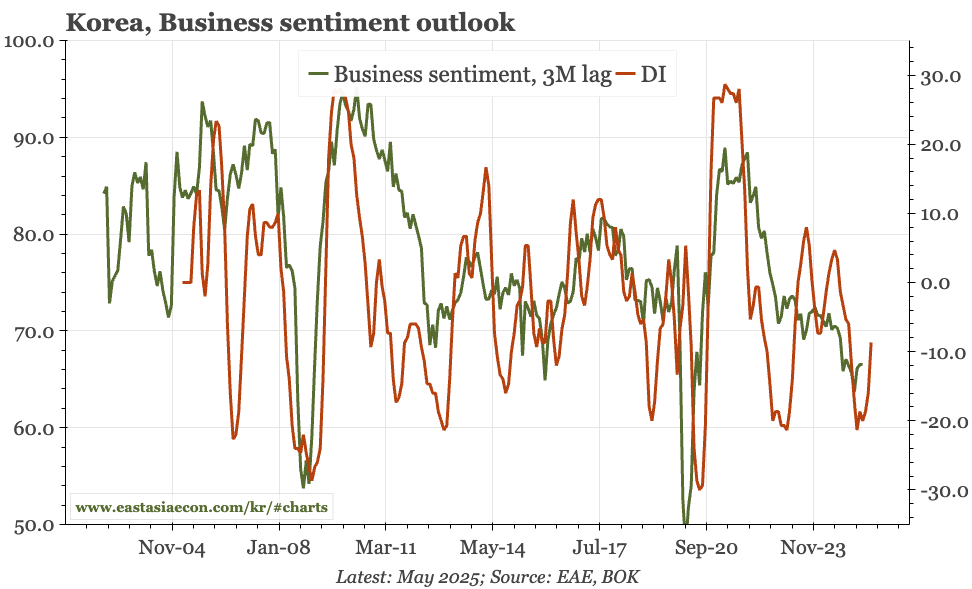

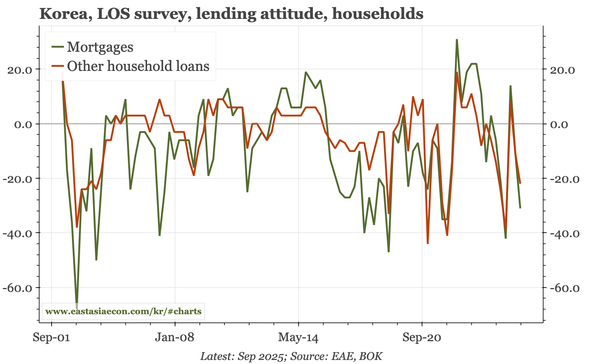

Korea – growth v household debt

Yesterday's minutes showed the clear tension for monetary policy between weak growth and financial excess. The BOK seems confident that the latest macro-pru measures will work. That sets the stage for more easing, though the committee in July wasn't quite as concerned about growth as it had been.