Subscribers Only

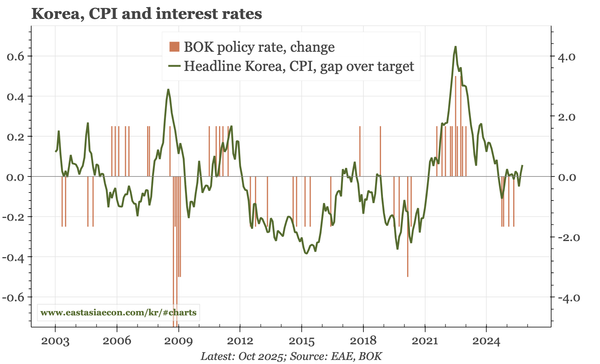

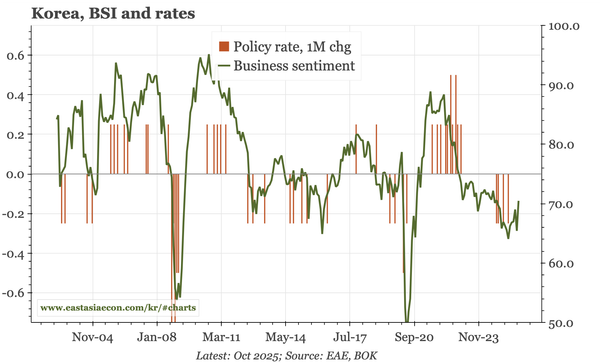

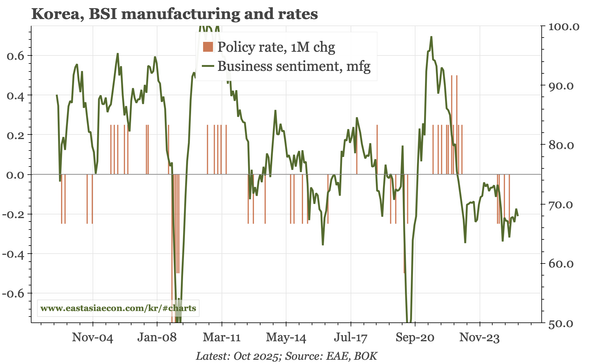

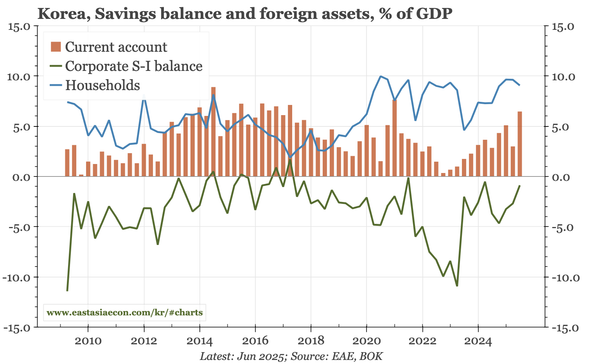

Korea – CA surplus not helping the KRW

Data today show Korea's current account surplus remaining at over 5% of GDP. The fundamental driver is a fall in borrowing by the corporate sector. This structural surplus hasn't started to support the KRW. One reasons is continued outflows from the NPS.