Subscribers Only

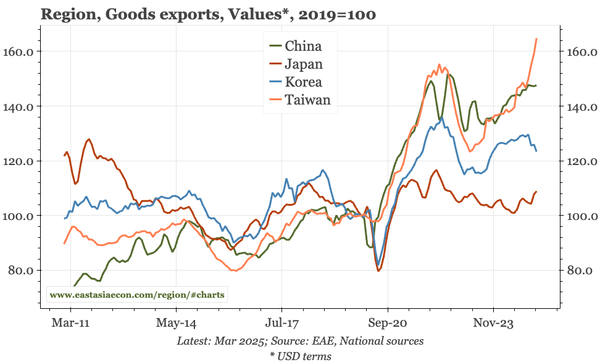

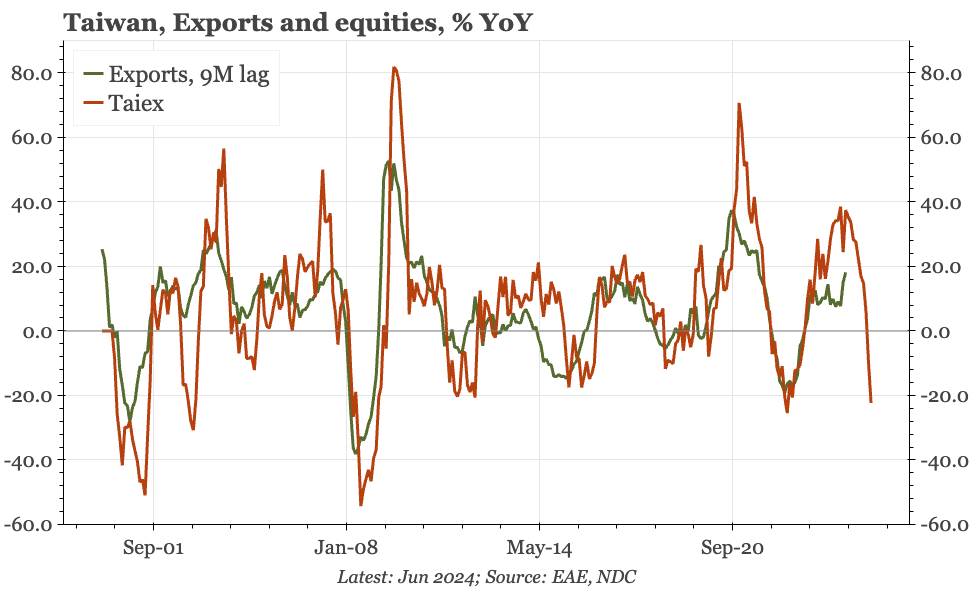

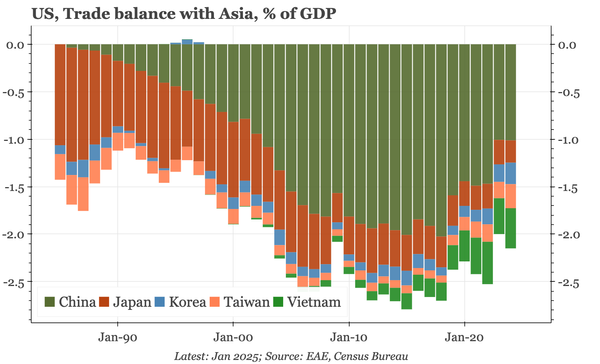

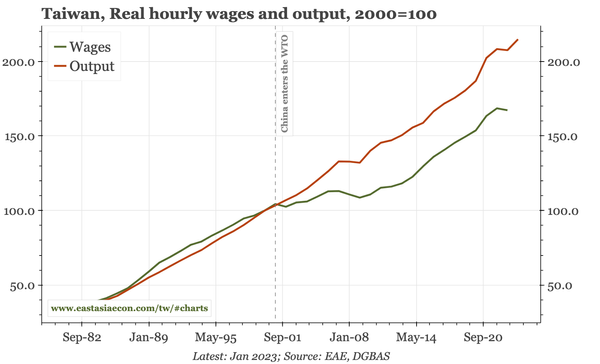

Taiwan – how to cope with the US shock

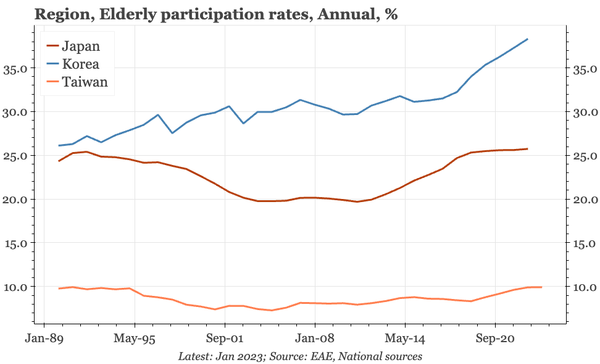

Taiwan macro doesn't attract much attention, but its experience matters. Taiwan was most exposed to the 2000s China shock. That it then suffered near-deflation reflected tight fiscal policy, a lesson that needs to be learnt in dealing with the latest shock, this time emanating from the US.