Subscribers Only

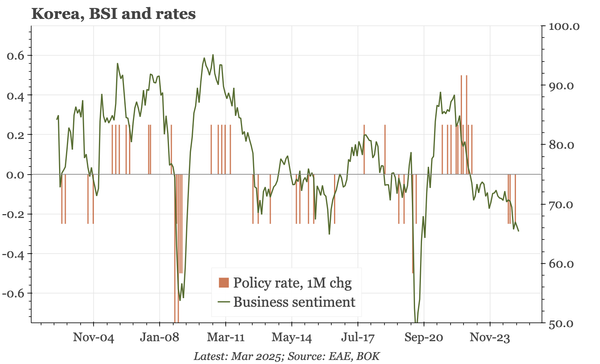

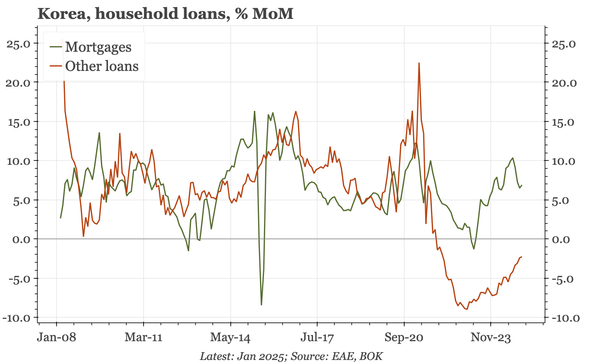

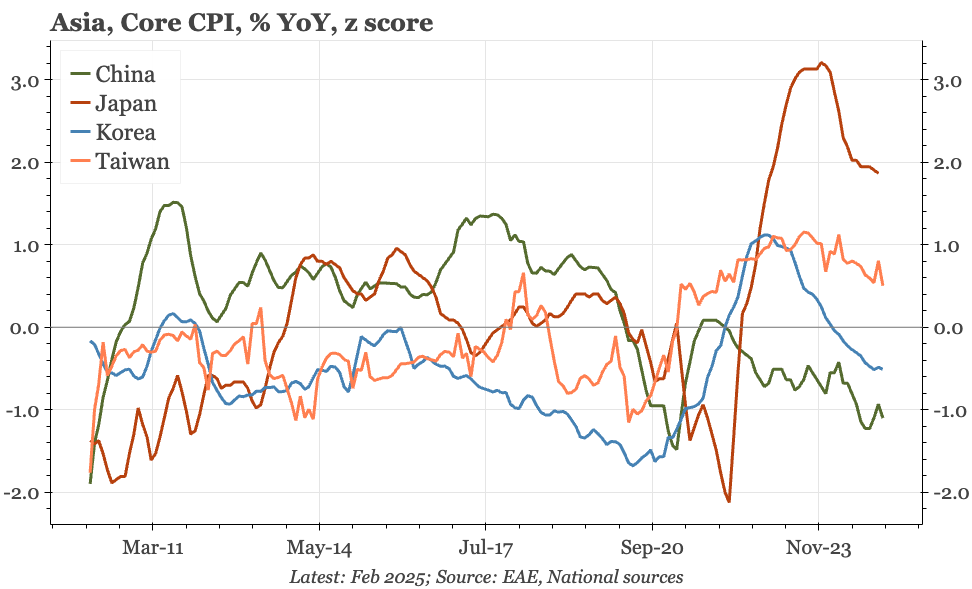

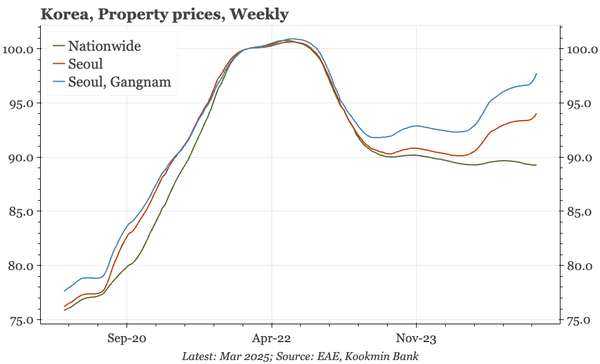

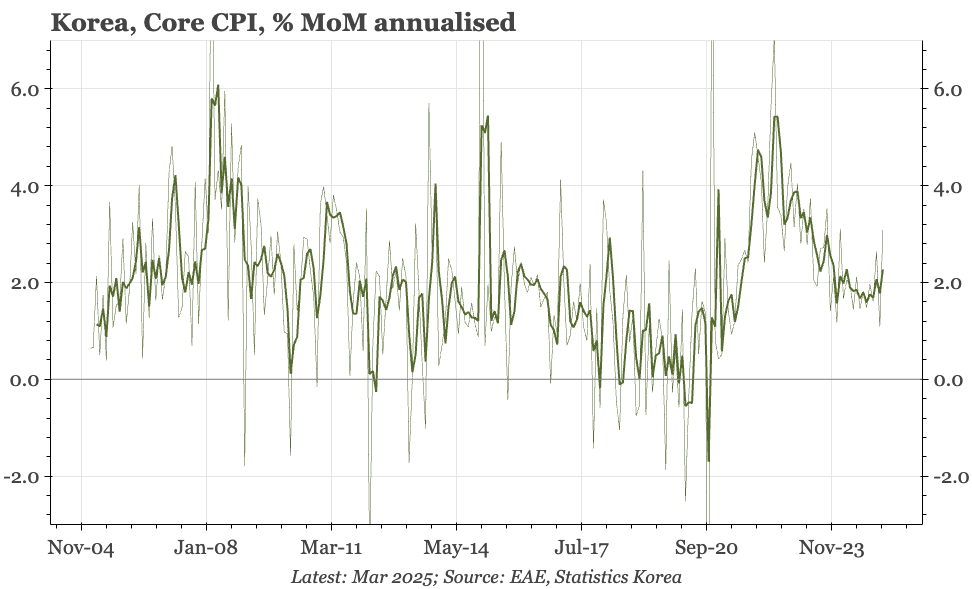

Korea – core inflation up again

With public services prices rising in March, the upwards drift in private services prices of recent months is now showing in core inflation. It still isn't high, but with business surveys suggesting some pressure on goods prices too, inflation is becoming more of a constraint on BOK action.