Subscribers Only

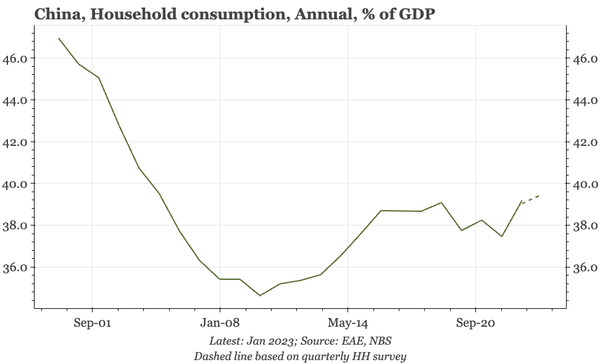

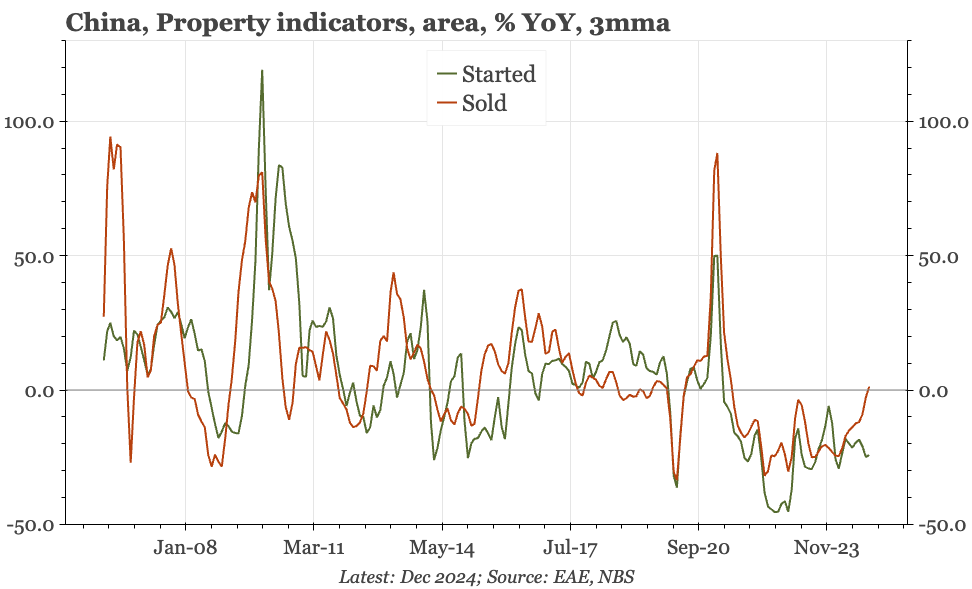

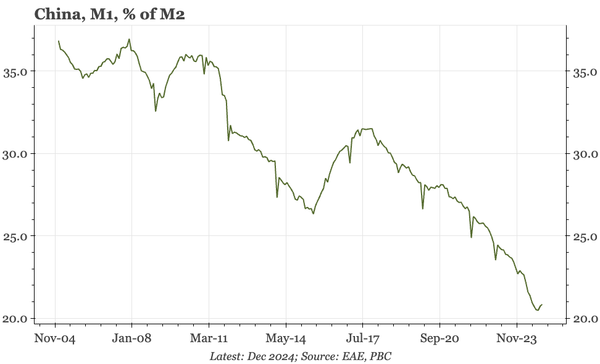

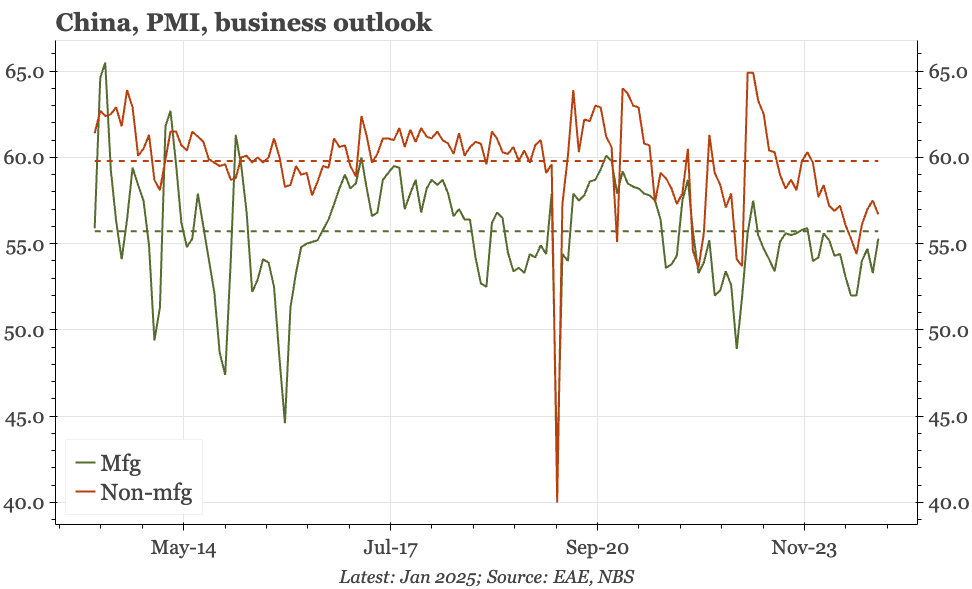

China – not very informative

Data today don't help in understanding the cycle. PMI headlines softened, but that isn't unusual when Chinese New Year falls in January. The details didn't drop in the same way, but also don't look strong. Separate data for industrial profits did improve, but that isn't a reliable data series.