Subscribers Only

Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The platform for tracking and understanding East Asia macro

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

Today's flash PMI was weak, but respondents highlighted JPY-driven price pressures. October CPI data were also firm. Ueda highlighted this week that December is live, but dependent on data before then. The BOJ's assessment of services inflation, and the Q4 Tankan, are particularly important.

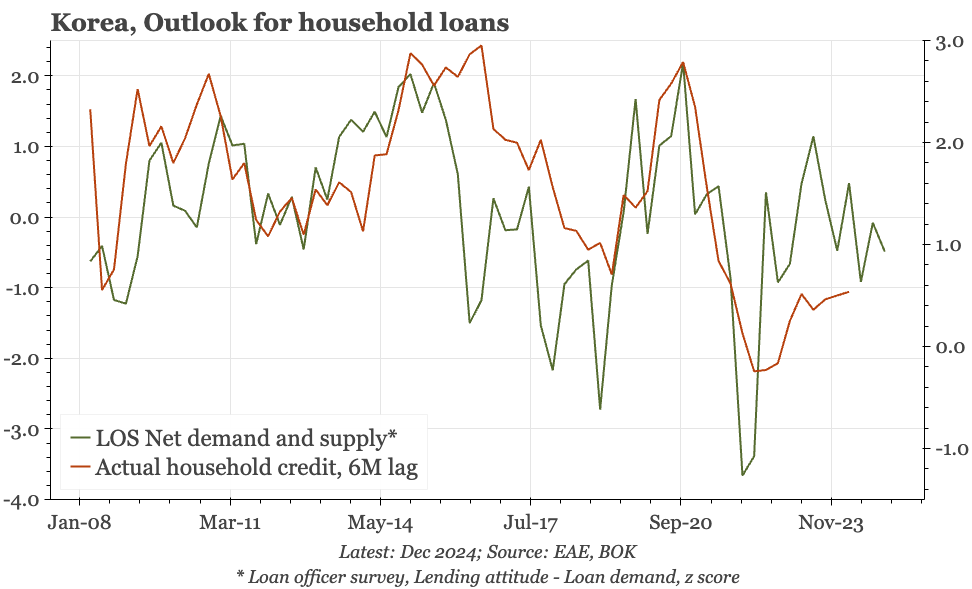

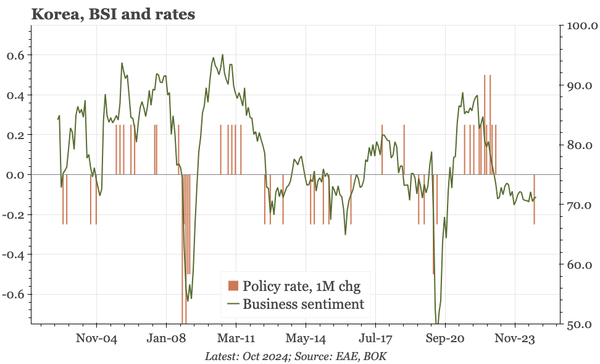

The BOK has been slow to cut, and when it finally did in October, its tone was hawkish. Since then, however, growth of both exports and household debt softening. This opens up room for the BOK to become more doveish, with the risks being KRW weakness, and sticky services price inflation.

Governor Ueda today struck a positive tone on domestic developments. But he also highlighted overseas uncertainties, and didn't give any hint of a hike in December. That doesn't make next month impossible, but it is more difficult.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

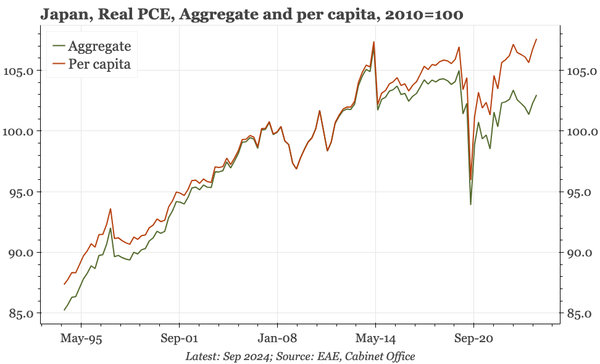

GDP grew again in Q3. Much of the rise since Q2 is because of a recovery in consumption, but that continues to be much more visible in per capita terms: aggregate consumption is still below the pre-2020 highs, dragged down by a fall in the population, a decline that the BOJ obviously can't address.

With a bounce in reported retail sales, it looks like economic growth in October got back to the government's 5% growth target. Overall, though, the tone of the data was rather mixed, with real estate activity in particular still extremely weak.

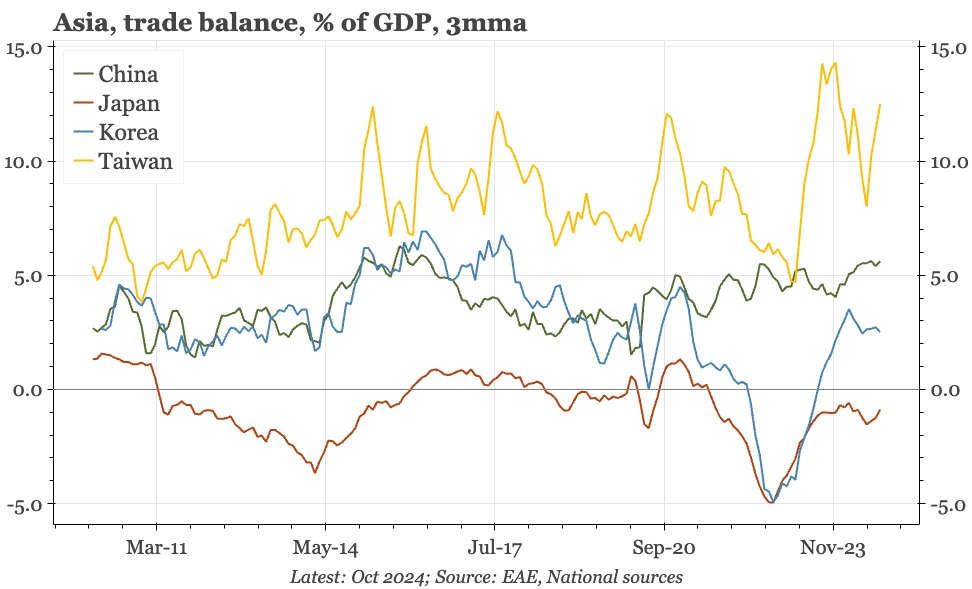

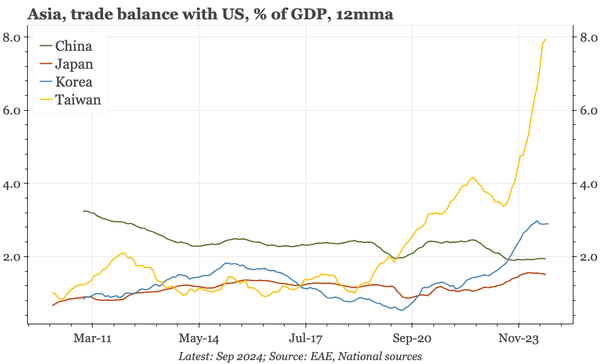

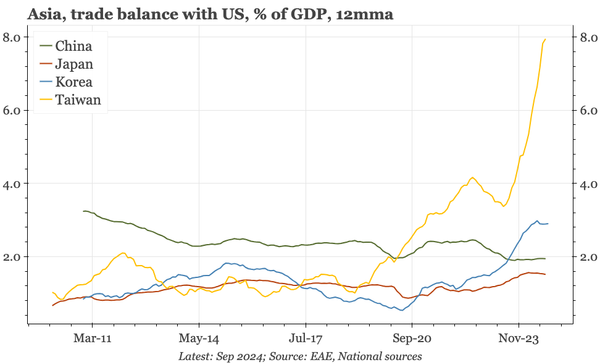

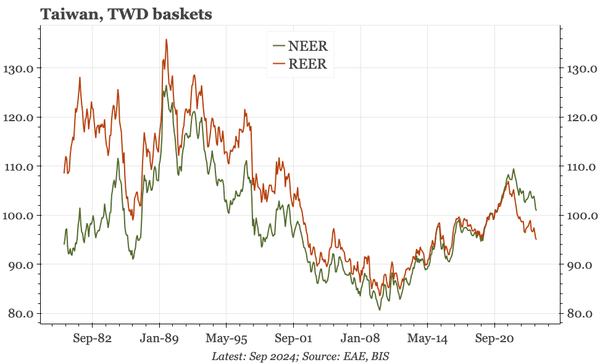

In recent years, trade and FDI flows from Taiwan and Korea have clearly shifted from China to the US. That's what Trump One and Biden wanted, but Trump Two won't like the rising trade deficits, or the CHIPS and IRA subsidies. If he threatens tariffs, will Taiwan offer a stronger TWD in response?

The opinions from the October BOJ meeting show a bit less concern about US uncertainty. That seems premature, given the election, but comments on the domestic economy also don't suggest any change in the bank's fundamental view. Survey data have been a bit softer, but not yet uniformly.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The bond swap does represent substantive policy. But there still isn't support for consumption, so this does look like an effort to put a floor under growth, rather than produce a new upcycle. And while that will probably be successful, stability will be endangered by a new round of Trump tariffs.

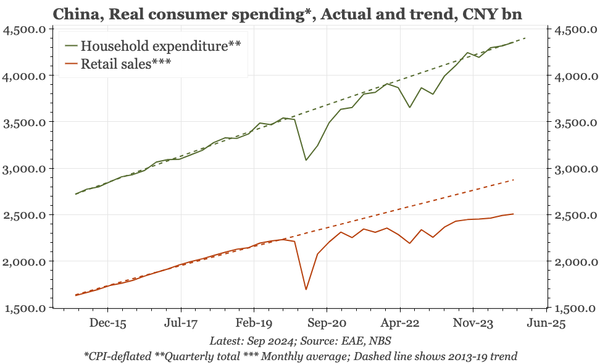

A chart pack arguing that consumption hasn't been as weak as is often imagined, but that downside risks are growing as wage and property income falls. Policy solutions need to overcome the weakness of non-wage incomes, the strength of savings, and the pro-investment official mindset.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The boxes in the BOJ's full outlook report that look at the labour market and wages don't suggest any weakening of the bank's underlying confidence – increasingly evident before July – that Japan's inflation is sustainable. The implication is that rate hikes remain on the agenda.

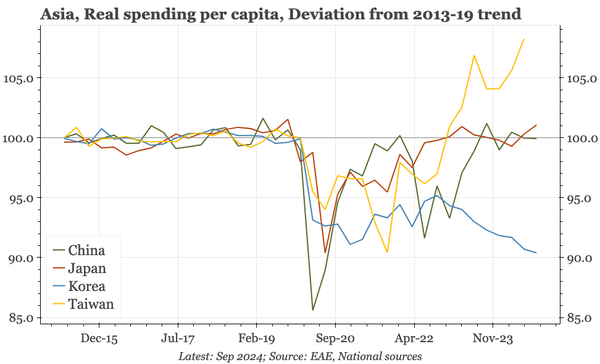

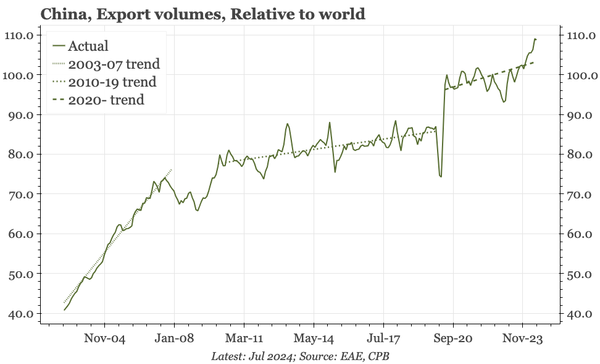

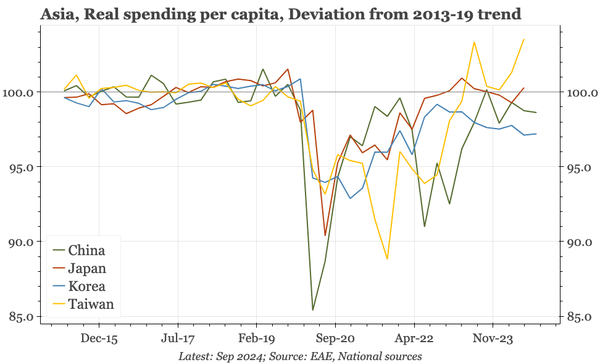

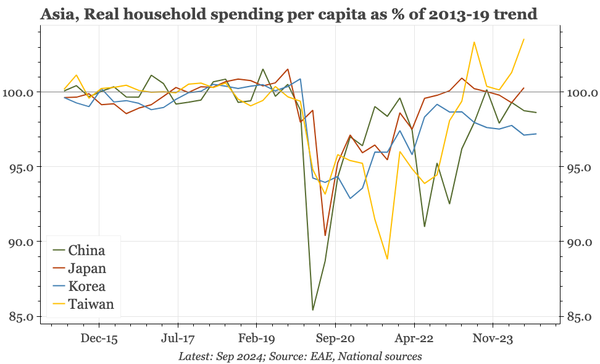

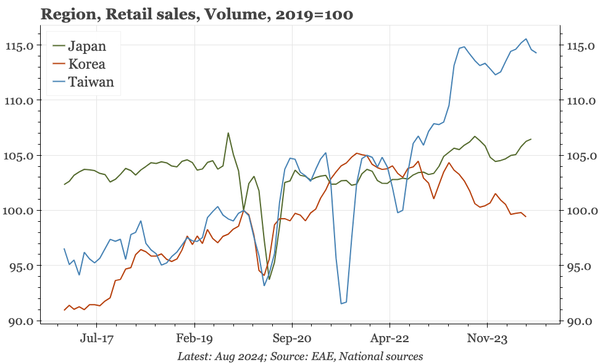

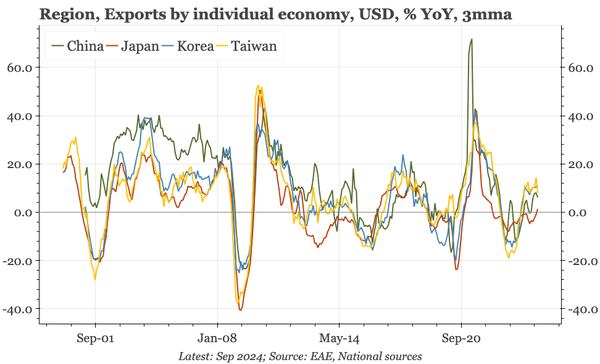

Some analysis of the weakness of consumption in Asia. As the opening chart suggests, the big underperformer isn't either China or Japan, but rather Korea. The clear outperformer is Taiwan.

No surprises from the BOJ (yet): the July forecast for underlying inflation to remain around 2% was maintained, as was the policy caution since August that stresses uncertainty in outlook for the US. There's still the press conference and full outlook report to come.

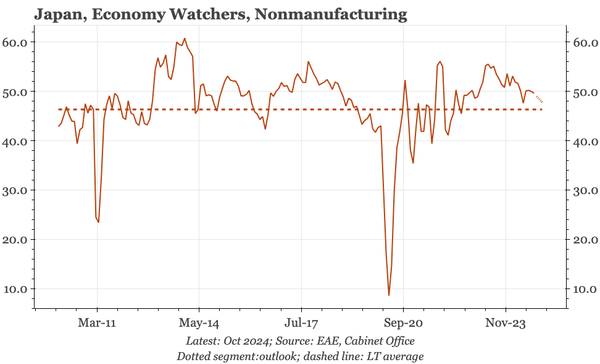

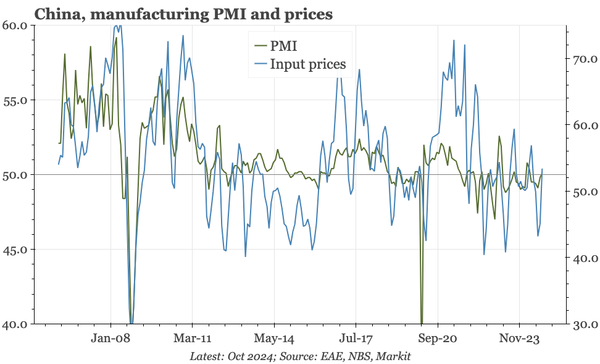

Likely driven by the sentiment-driven rise in prices, the manufacturing PMI bounced back above 50 in October. But there was barely any change in either the services or construction, PMIs, and both will need to improve to think that the economy really is turning around.

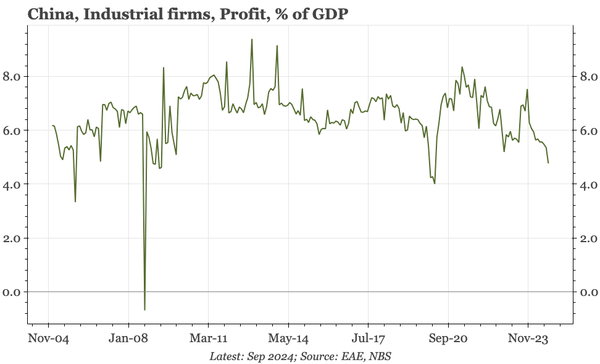

The government yesterday published its monthly series for the profits of the industrial sector. I am always a bit sceptical of the quality of these data. But if you want a trigger for the recent macro policy push, then the sharp fall in profits in September fits the bill.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

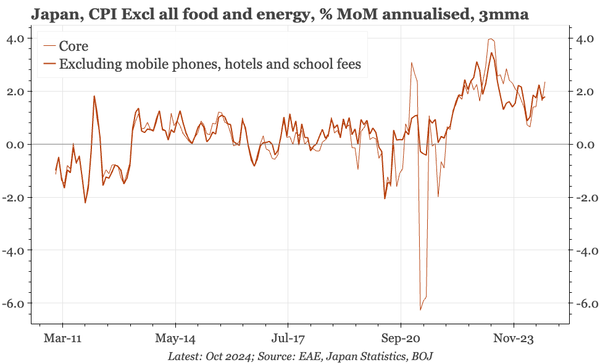

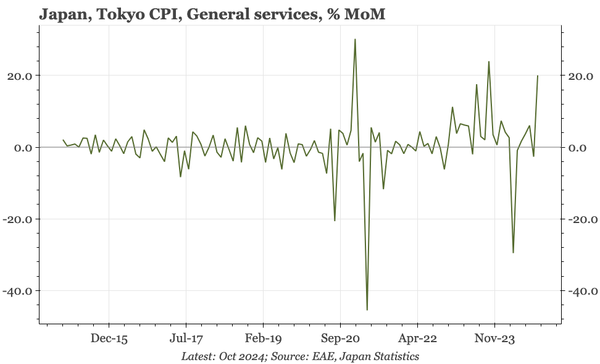

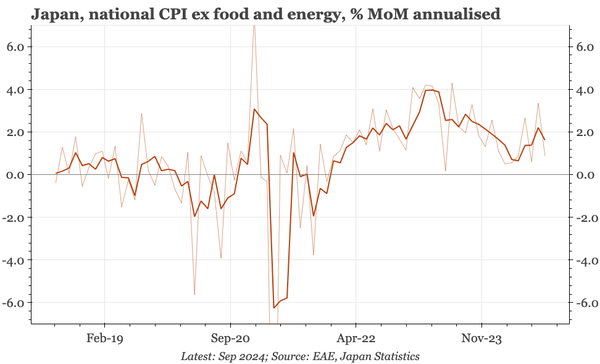

With the BOJ emphasising the twice-yearly patten of service prices hikes, with the second round falling in October, today's Tokyo CPI data are important. They do show services prices rising, and although the details are messy, core sequential inflation in Tokyo is also continuing to run near 2%.

If the BOK was only looking at growth, then data today would give it plenty of room to cut faster, with both Q3 GDP and October business sentiment weak. However, the rise in US rates and consequent weakening of $KRW will be starting to constrain the bank once again.

The slump in confidence and retail sales don't indicate a major cyclical weakening of consumption. That's partly because households have been running down excess savings from covid. But with savings now normalising, consumption is becoming more vulnerable to the deterioration in the labour market.

There's a possibility that TSMC's success is pushing Taiwan into unchartered waters, where the CBC needs to sound hawkish, when the external imbalance is as big as it has ever been. If Taiwan's period of zero inflation has passed, there's a good chance TWD undervaluation will be challenged too.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

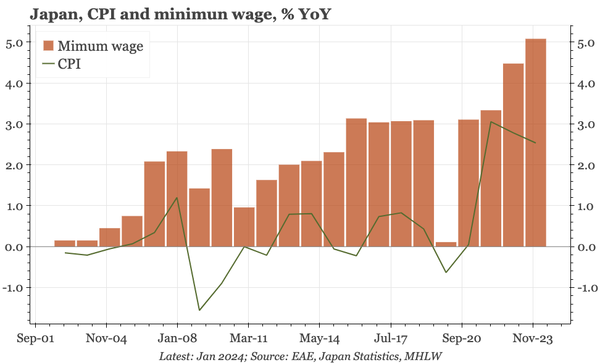

Inflation was softer in September, but the economy still looks on track, with exports and household income up, and early signs of another strong shunto round. At the same time, the JPY is weakening again. This backdrop means the BOJ faces a very tough communication challenge at its October meeting.