Subscribers Only

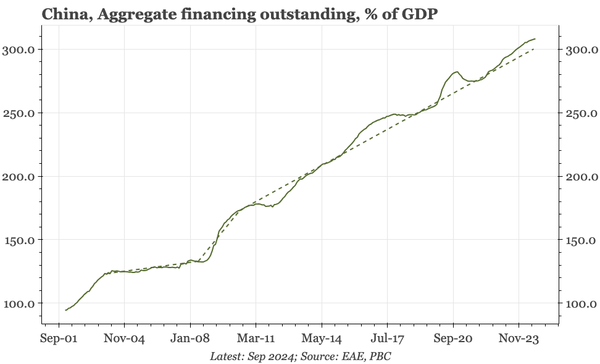

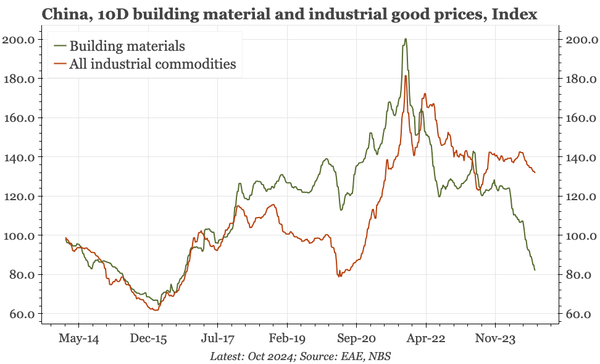

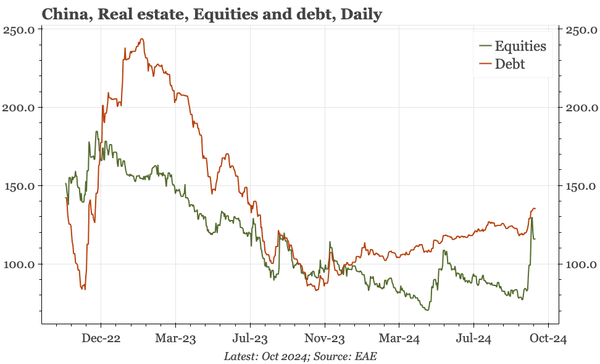

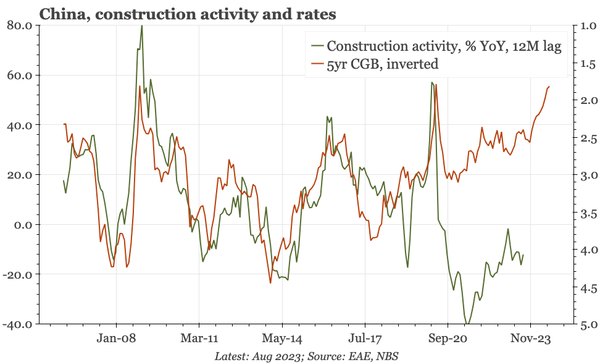

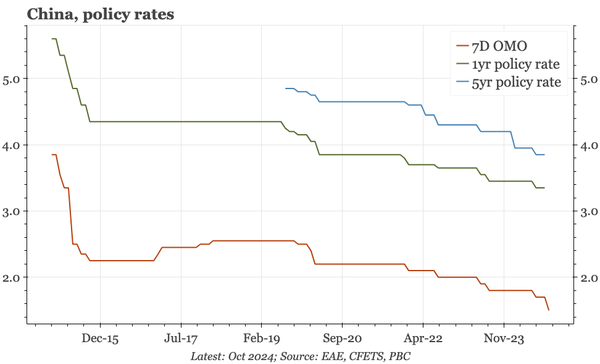

China – keep on muddling through

Looking at today's data, the driver of all the recent policy activism is to get growth back to the 5% target. That doesn't suggest a big rebound in the nominal growth that equity investors need. The upside risk is this policy push is happening when there are tentative signs of property stabilising.