Subscribers Only

Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The platform for tracking and understanding East Asia macro

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

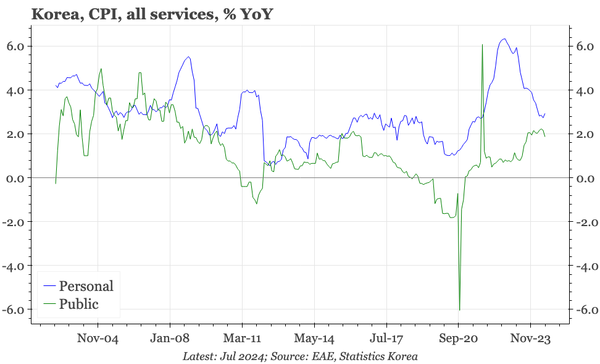

Particularly if US policy action reflects a weaker economy, the BOK will likely cut if the Fed does. However, with the rebound in home price inflation that has been a focus for the BOK, and tentative signs of an upturn in services prices that so far hasn't, the BOK likely won't be in a rush.

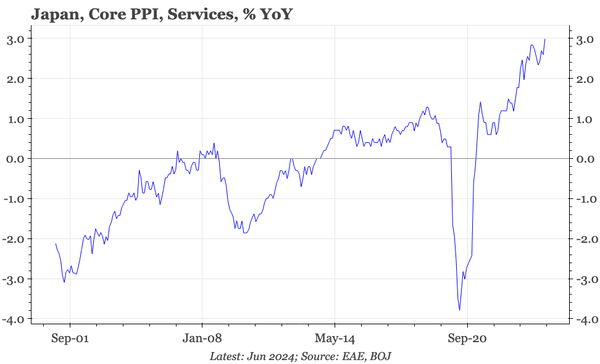

In its full outlook report, the BOJ sounds confident on services prices and wages at larger firms. It is less certain about wage rises at SMEs. Developments at smaller firms, and service price hikes in the traditional (but long-forgotten) price setting month of October, will be important to monitor.

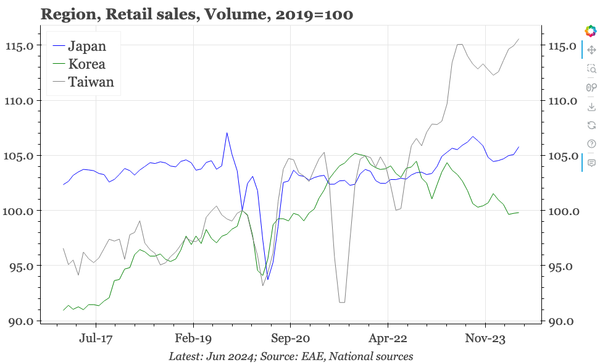

Apart from the changes in actual policy, three things stood out today: changes to the outlook for prices, a shift in the language used to describe policy, and separate from the BOJ meeting, the latest consumption data, which remain weak.

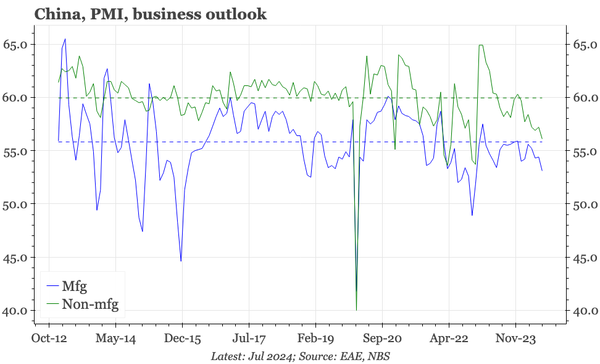

Our China cycle framework is that the muddle through of the last 18M is running out of road. The July PMIs look consistent with that, with weakness in pricing, jobs and confidence. The one remaining contrary indicator is the S&P mfg PMI, which has been strong, and for July will be released tomorrow.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The BOJ became more positive in 1H24, and labour market and price data since should have increased confidence further. So we think the bank hikes next week, with a probability of 60%. That our conviction isn't stronger still is because of the implications of the June non-decision on JGB purchases.

Recent data suggest an unchanged macro story: a slow moderation in inflation and a weak domestic economy, but export and property recoveries. The first two dynamics point to an interest rate cut, but the second two suggest that still isn't imminent.

Overall price expectations in today's July consumer confidence survey fell. But overall sentiment and property price expectations rose. That gives the BOK continued justification for pushing back on expectations for an immediate rate cut.

A reminder of our roadmap for China's cycle over the next few months, which we summarised in an opinion piece in today's Nikkei Asia.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

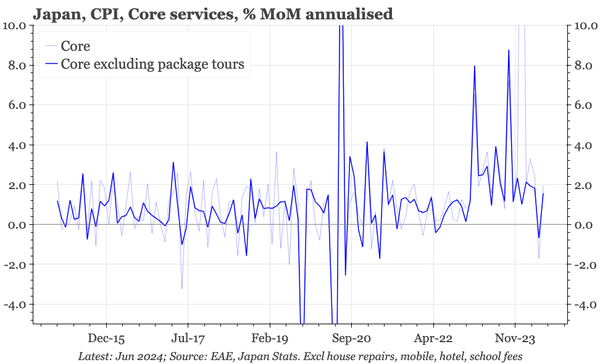

Inflation was largely unchanged in July. Services inflation was a bit higher, but for the BOJ these data are probably less important than the results of the strong Tankan earlier in the month.

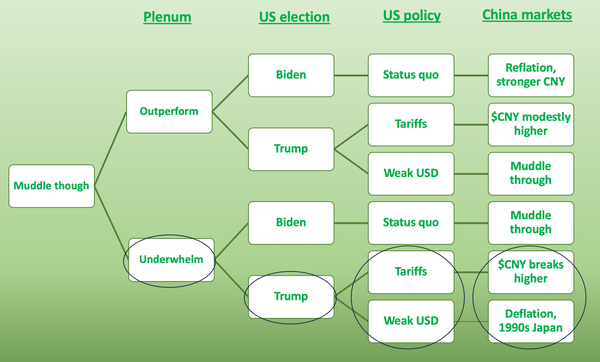

This is our monthly slide pack for China, that goes through the argument we laid out last week: how the Plenum and the US election together likely end the macro muddle through of the last 18 months.

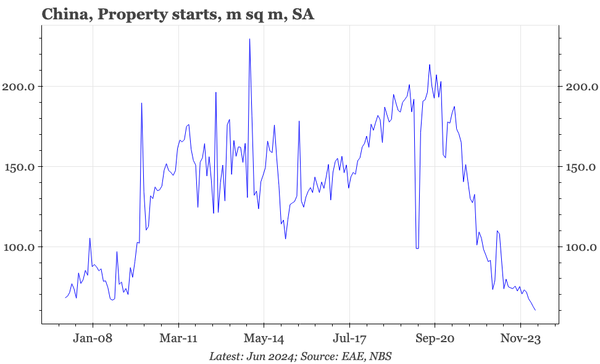

Today's GDP release shows property activity is still collapsing and economy-wide pricing is weak. The PBC will struggle to hold up rates – and thereby the currency – if this week's Plenum doesn't provide a real boost to sentiment.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

Even allowing for a change in credit intensity, June headline credit and money data are bearish. The one positive trend is data through May showing household demand deposits no longer falling so quickly. That shift continuing would help sustain China's macro muddle through.

We don't have conviction about what the Plenum will deliver, but we are confident that with next week's meeting, and then the US election, the macro and market muddle through of the last 18M is likely ending.

In staying on hold today, the BOK put slightly more emphasis on the KRW and household debt. The bank is moving towards a cut, but that decision now seems a bit more tied to the Fed and rate differentials.

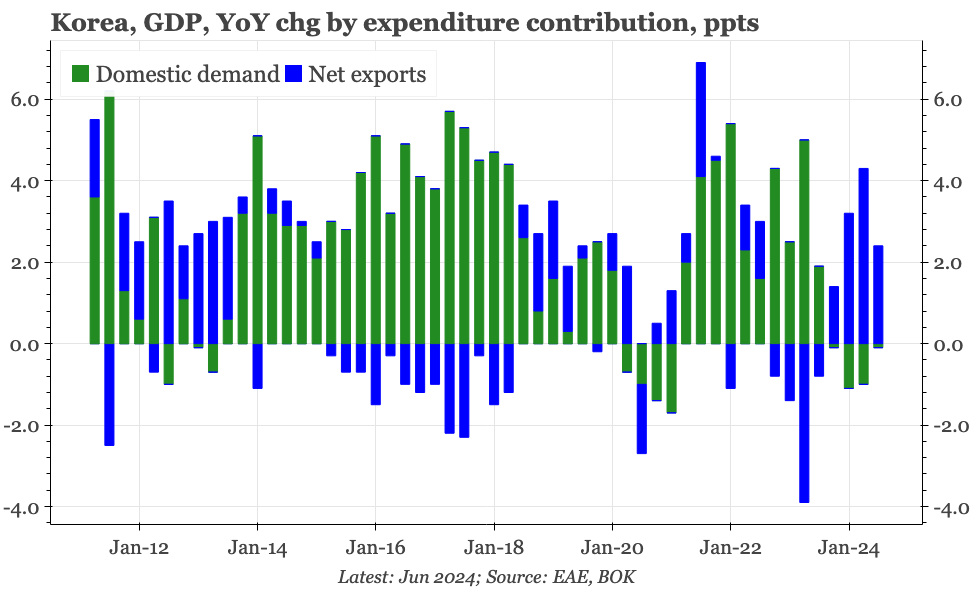

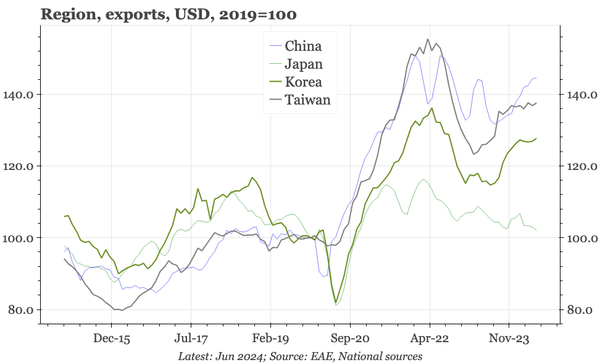

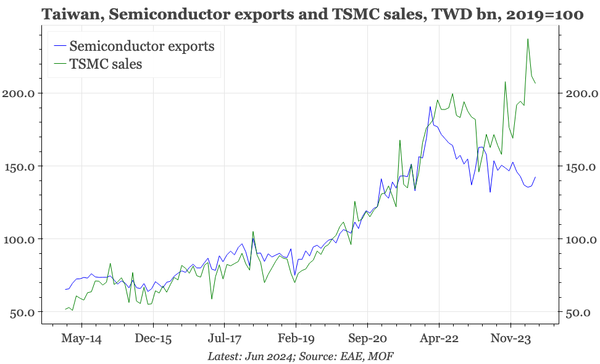

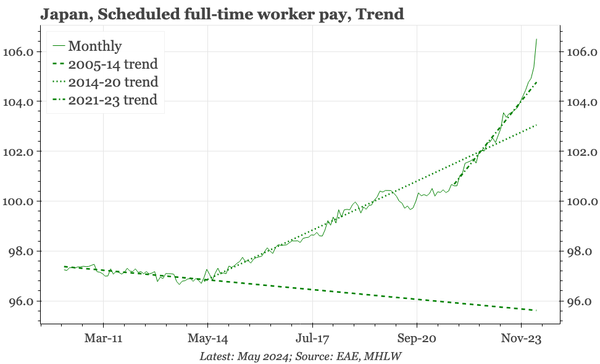

After faltering in 2023, wage growth is now back on the stronger trend that began in 2021. The recovery in the manufacturing cycle gives us confidence that this can at least be sustained, but we'd still like to see a clearer lift in exports.

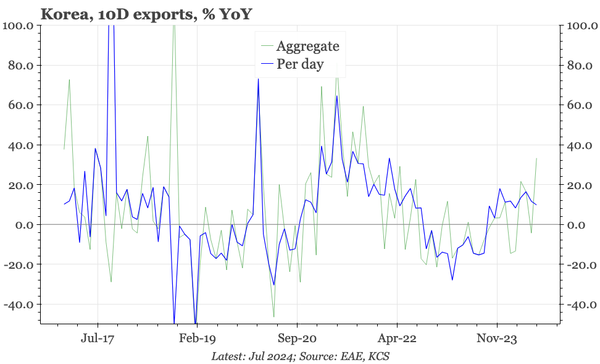

With the labour market another sign of economic weakness, rate cuts are getting closer, but the pick-up in exports continues to give the BOK time to confirm that inflation does indeed drop to target.

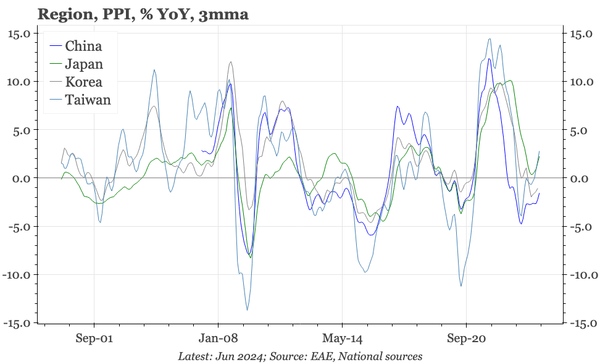

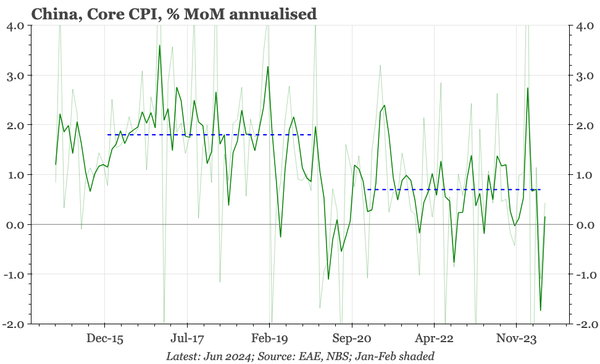

PPI deflation has been more cyclical than structural, and the strengthening in Q2 should continue into Q3. But core CPI remains very weak. Inflation is too low to support rates.

The one-off firm survey undertaken as part of its long-term policy review has allowed the BOJ to reiterate its positive stance, and provide more of the evidence underpinning it.

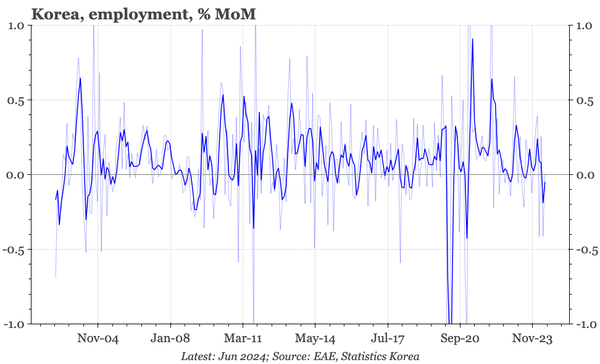

May data give us more confidence that wage growth is accelerating. Other data today for activity aren't as robust, but don't suggest conditions are worsening further.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The moderation in core CPI inflation in June likely won't be enough to keep the central bank on hold if exports rise anywhere near the extent that equities are signalling is possible.