Subscribers Only

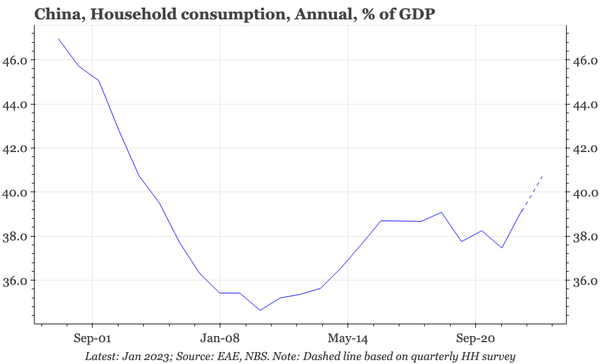

China – a collection of counter-intuitive consumer cycle charts

We combine quarterly household survey data with recently released annual GDP data to show why consumption isn't weak, what that means, and what there still is to worry about.