Subscribers Only

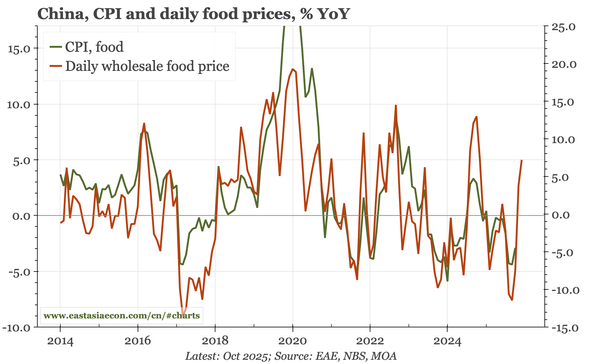

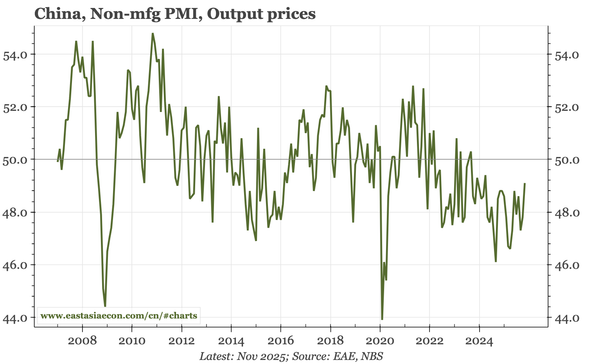

China – food prices lift CPI

Today's inflation data weren't surprising, with the big shift being food prices lifting CPI. Non-food prices aren't rising, but in level terms aren't falling either, which is an improvement from 1H25. Nominal growth should look better through Q126.