Subscribers Only

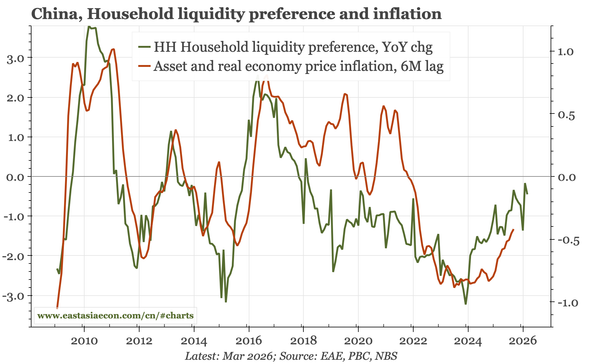

China – inflation up again

PPI inflation accelerated again in April, and with CPI inflation firm, the GDP deflator is on track to rise in Q2 for the first time in 2022. The turn is being led by energy and commodity prices. There are some signs of a stabilisation in underlying prices too, but so far, they are tentative.