Subscribers Only

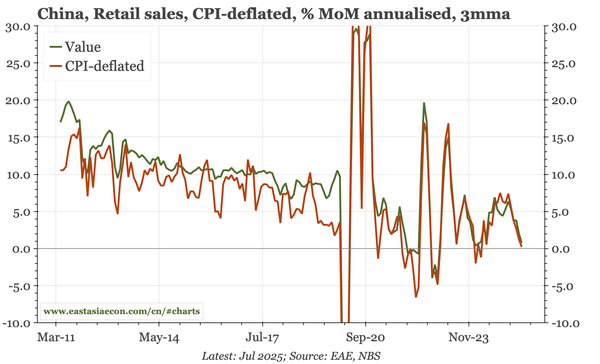

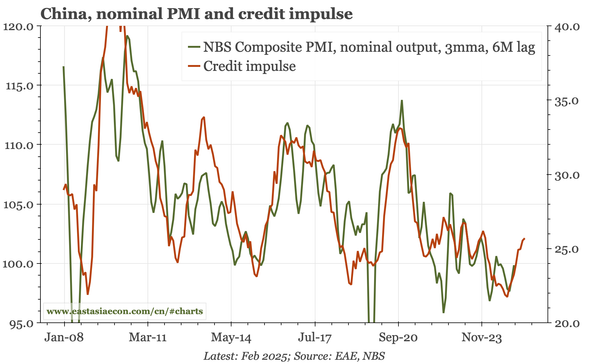

China – a weak nominal upturn

While the PMIs don't point to any real improvement, in nominal terms there's been a lift, with input prices above 50 again. That's in line with the credit impulse. But the credit impulse might already have turned, and while PPI deflation has lessened, output prices don't suggest stronger CPI.