Subscribers Only

Japan – limited PPI downside without lower import prices

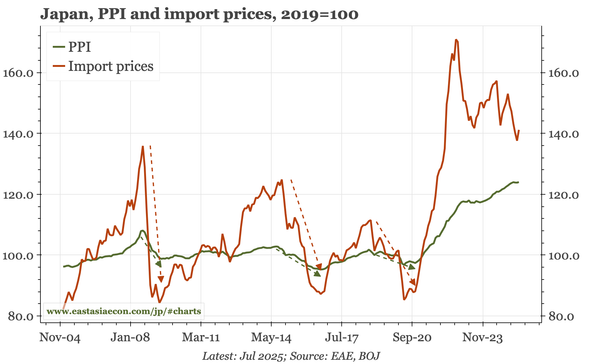

Headline PPI inflation is softening, but a real correction is unlikely without a bigger fall in import prices. In July, import prices ticked up, as did auto export prices, but only slightly. In other data, non-manufacturing sentiment in the August Reuters Tankan remained firm.