The East Asia Economist

The BOJ is under pressure, but Japan isn't in crisis. Rising energy prices hurt, but ending YCC would be painful too. Instead, it is probably better to focus on economic normalisation post-covid. That would likely include an influx of tourists concluding that, with the JPY at 135, Japan is cheap.

Japan - Covid not the currency

The BOJ has come in for a fair amount of criticism the last week or so. At the simplest level, the disapproval has two strands: first, with everywhere else tightening, Japan should be too; and second, that with the JPY collapsing, the BOJ needs to end Yield Curve Control, and allow interest rates to rise. The more sophisticated line of attack is that consumer sentiment, already depressed, is at risk of being pushed down yet further by the surging JPY price of commodities. In this way, BOJ policy is encouraging deflation, not reflation.

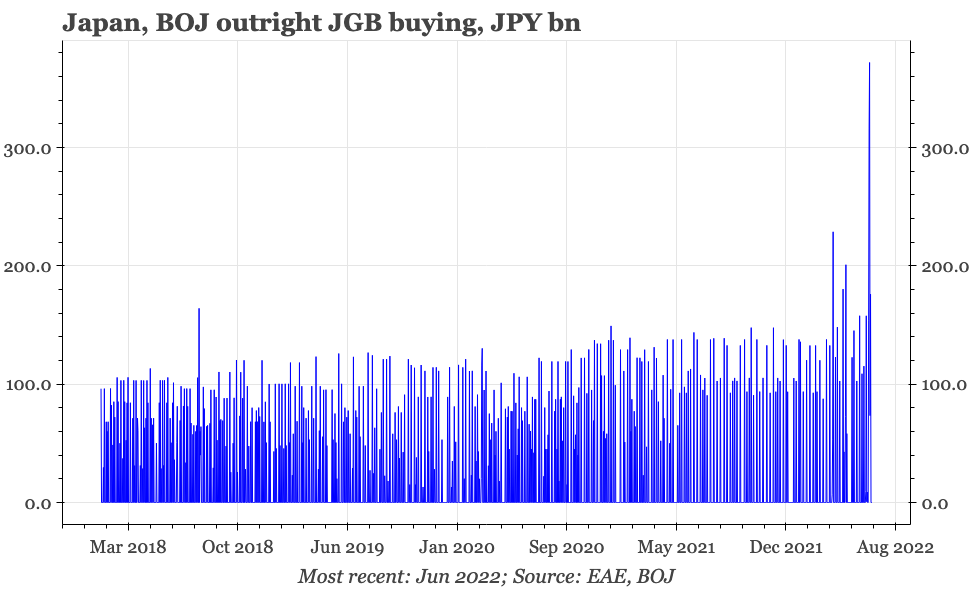

In fact, the tightening trend isn't as global as if often supposed. Korea is certainly all on-board, but elsewhere in East Asia, China is loosening, and Taiwan is only a reluctant tightener, raising rates by just 12.5bp last week. There are differences in activity levels between China, Taiwan and Japan, but there is a commonality in inflation being relatively low, with core CPI running at under 2% in all three economies. As for the JPY, that is weakening fast, and BOJ bond buying last week went through the roof. That said, pro-cyclicality is an inherent element of the BOJ's Yield Curve Control; while the central bank probably feels it is buying too many JGBs much right now, in the run-up to 2020 when global inflation was low, it was struggling to buy enough bonds to keep the monetary base expanding.

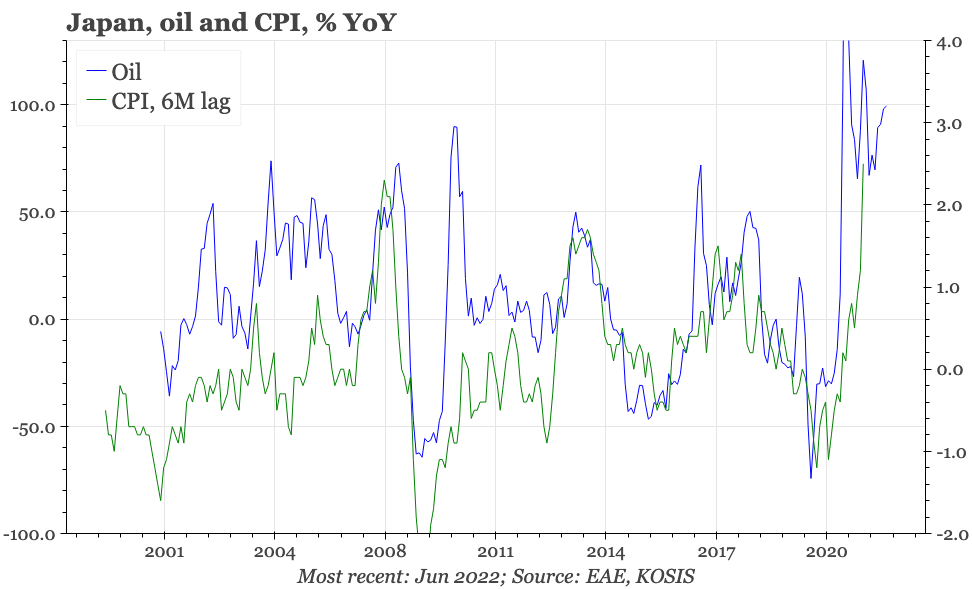

The sharp move in JPY commodity prices is pushing up headline CPI, and that in turn is weighing on consumer confidence. But it seems unlikely that the higher interest rates that would result from the ending of YCC would be great news for consumer confidence either. In any case, the weakness in consumer sentiment preceded this round of commodity price hikes. One factor has been the Covid-19 drag on economic activity, which has been prolonged in Japan, and helps explain why Japanese GDP has yet to recover pre-pandemic levels.

The covid hangover is the result of a larger social reaction to the virus, as well as ongoing government restrictions. Both factors now show signs of dissipating, and given that, a better policy strategy than ending YCC would seem to be to accelerate this post-pandemic normalisation. It has the potential to offset the negative impact on consumer sentiment of rising commodity prices, help deliver the recovery of GDP, and generate the sort of tightening of the labour market that is needed to increase wages. At the least, the BOJ would likely want to see both exhaustion of this potential, and signs that the cost of living crisis is seriously eroding support for the government – something that has yet to happen – before it gives up on YCC.

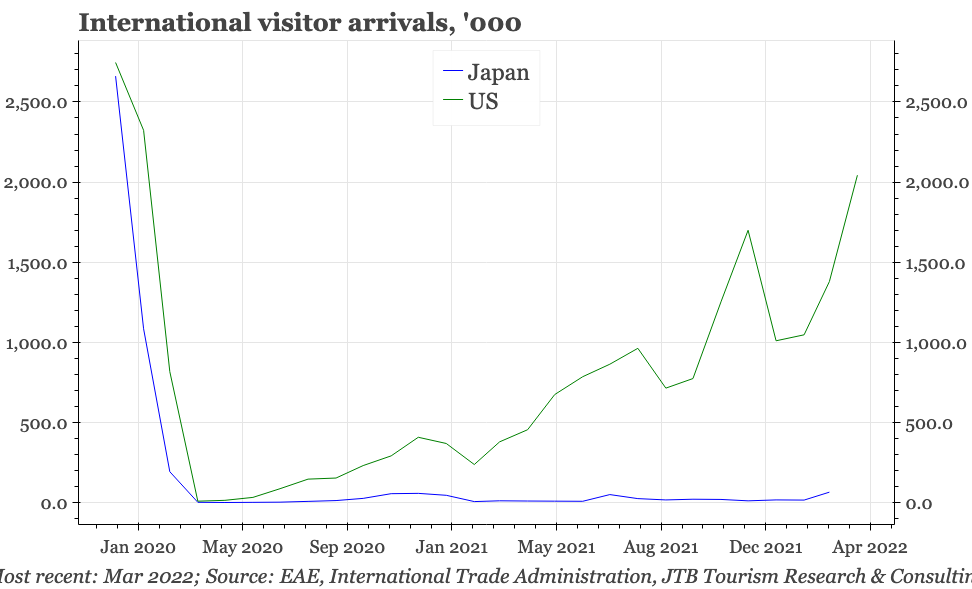

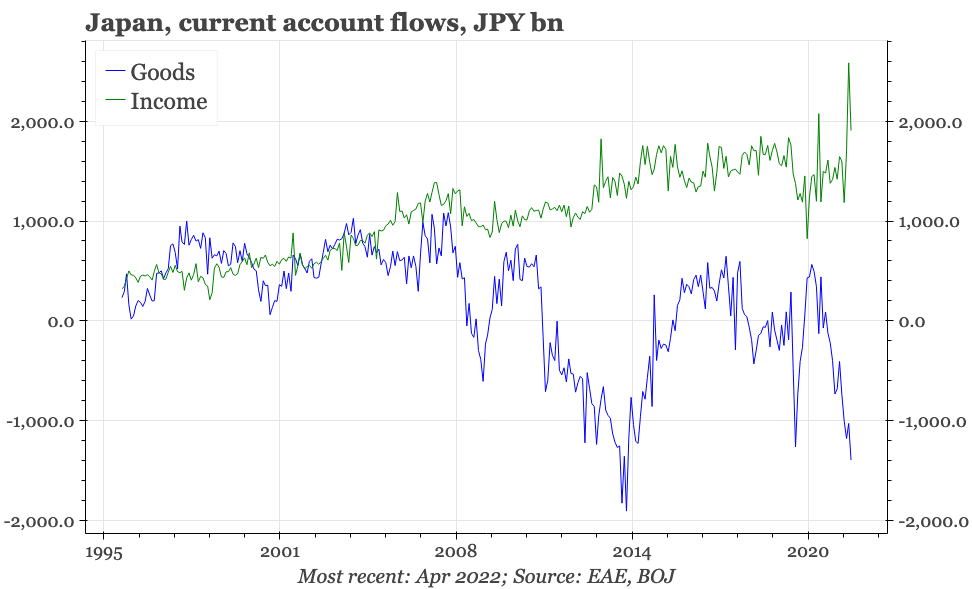

It also isn't clear that the JPY can only weaken. It has moved a long way already, and while rate differentials remain against it, other factors would suggest the currency is starting to look cheap. Despite the rise in the commodity-related import bill, the current account remains in surplus, boosted by the rising JPY value of the earnings from Japan's position as a large net creditor nation. The absolute cheapness of the JPY will become more obvious if the country continues to relax covid-related border restrictions on inbound tourism. With the JPY at 135, many visitors will find the country cheap.

None of this is to say that the current situation is comfortable for the BOJ. The central bank would clearly be hoping to see commodity prices fall, and US markets no longer needing to price in further rises in inflation. The warnings of some in the market that oil will get near USD200/barrel is something of a nightmare scenario for the BOJ. The same would be true of most other central banks too, but it would be worse for the BOJ if that was accompanied by yet more weakening of the JPY.

YCC costs

In terms of monetary policy direction, the BOJ looks like an outlier globally, but it doesn't stand out so much in East Asia in terms of bucking the global tightening trend. However, the central bank in Japan has much less control over the currency than its near neighbours, and its monetary expansion is much bigger, so the result of the differential in policy direction on the exchange rate is more obvious. The CNY has weakened by 6% against the USD since March. But the JPY has fallen by 12% in the last three months and 16% since mid-December.

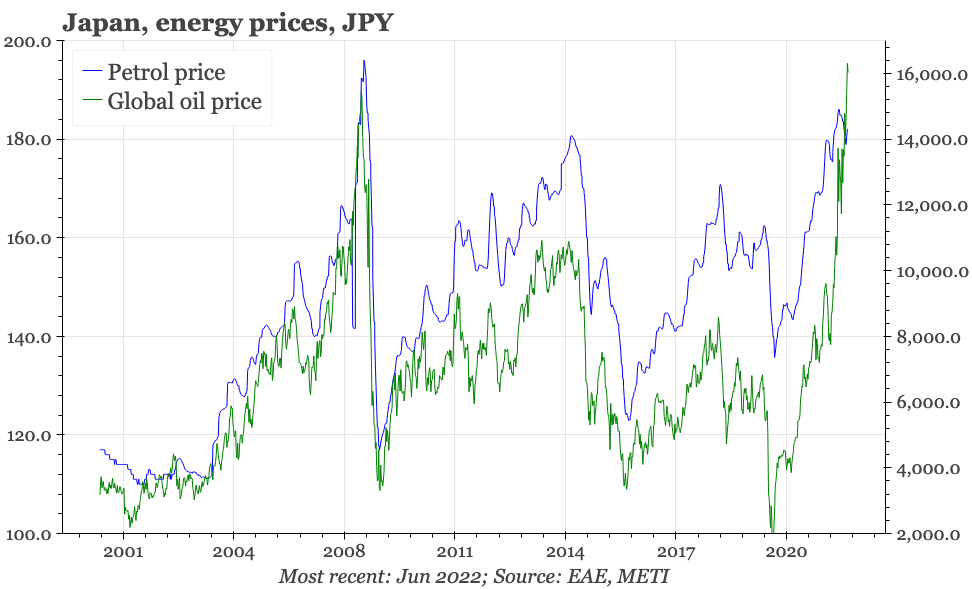

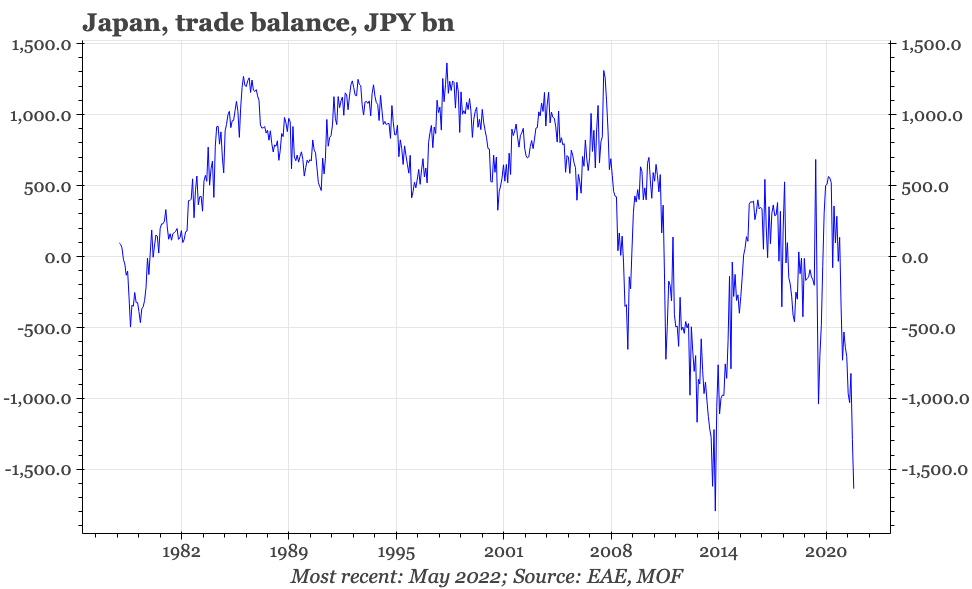

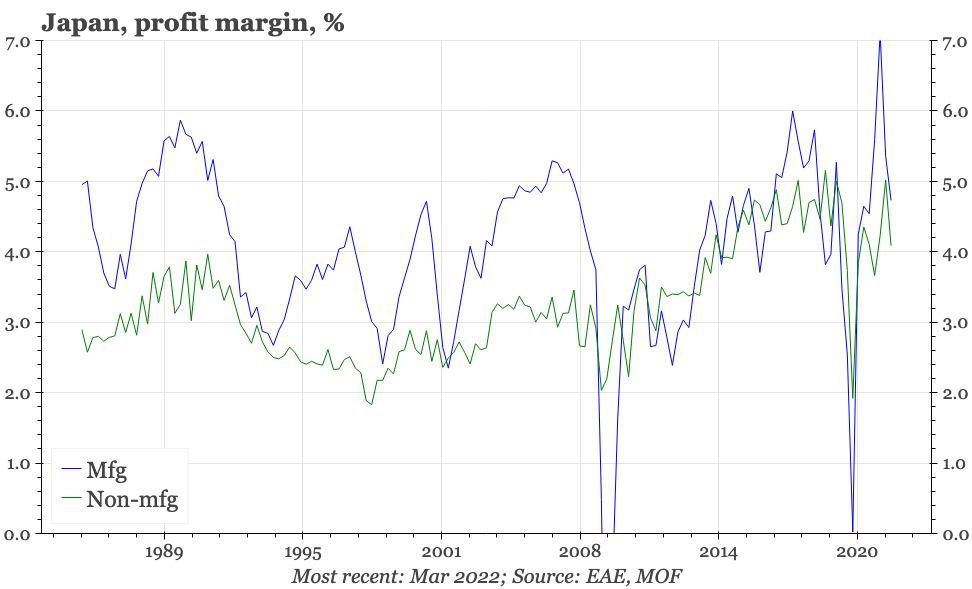

These are big moves, but not unprecedented – the depreciation of the JPY in 2013 was quicker, as was the appreciation in 2009. However, with global commodity prices rising too, there has been a double whammy for import prices in JPY terms. The local price of oil has roughly doubled since the beginning of the year. That also isn't entirely without parallel, but is more extreme than the move in the JPY alone. That sharp rise has helped push Japan's trade balance into deficit, and squashed corporate manufacturing margins in Q1. The ongoing rise in pump prices will squeeze real incomes for consumers.

Covid costs

Of course, if the BOJ was to give up YCC, then that would also impose real costs on the economy. Imported price pressures would recede, but domestic interest rates would rise. Higher rates and a steeper curve would benefit the financial industry, which has been the biggest domestic loser from YCC. Presumably, though, it would hurt the rest of the economy.

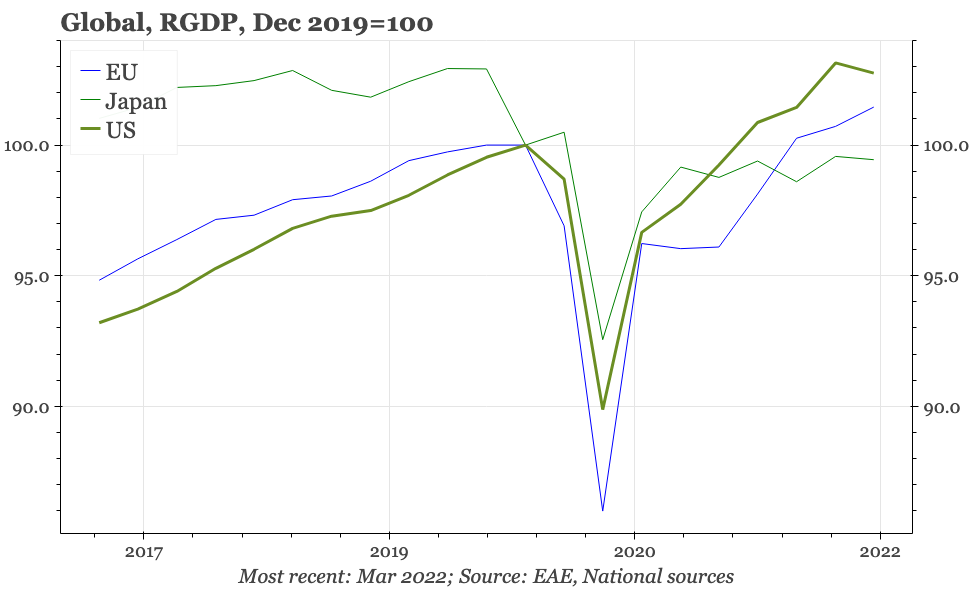

Overall, Japan doesn't look ready for that kind of tightening. Unlike every other major economy, GDP has yet to regain pre-Covid levels. In this way, Japan is at risk of repeating the experience coming out of the financial crisis in 2008. It is somewhat surprising, in that the monetary and fiscal policy response in Japan during Covid-19 matched that of the other advanced economies in a way that wasn't true in 2008-09. At least in terms of being too overtly conservative, there wasn't an obvious macro policy mistake the time around. Nonetheless, Japan's economy is far from fully recovered.

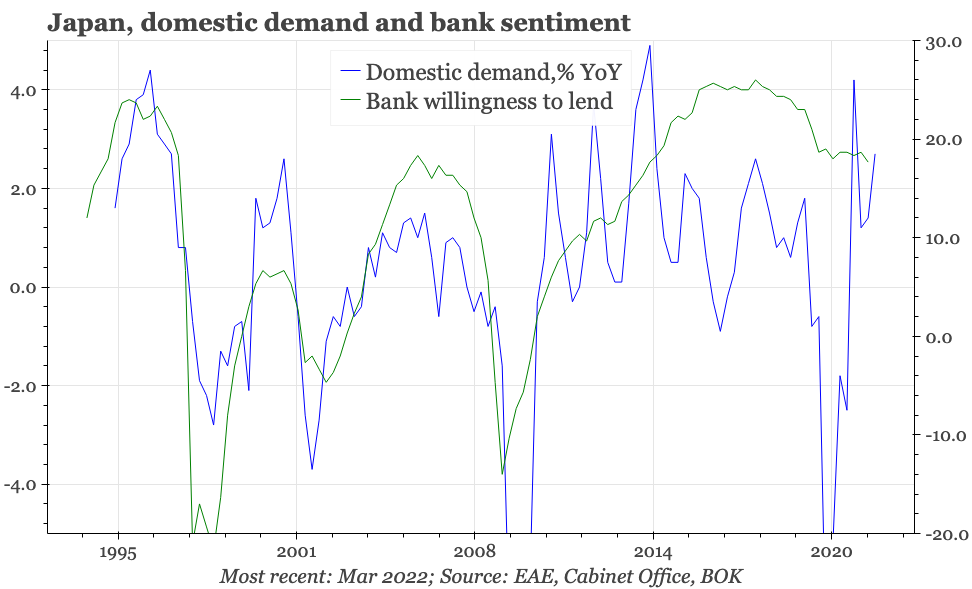

This stalled recovery might be because of YCC itself, as the impaired profitability of the financial sector dissuades banks from taking on risk and so supporting recovery. That doesn't seem to be the case. During the covid crisis, credit officer surveys showed Japanese banks having a greater willingness to lend than their counterparts in the US and EU. The latest Tankan survey of corporate sentiment shows that local banks aren't quite as free and easy with credit standards as they were in 2017, but they are also far from being tight.

The bigger reason for the stalled recovery seems to be the societal and government reaction to covid. Each wave of the virus had a big impact on domestic economic activity, encouraged by the government-imposed restrictions on the services sector. Officials have yet to relax fully these measures: Japan has just started to allow the entry of tourists, but so far, only in guided groups.

This unwillingness quickly to dismantle covid restrictions is perhaps understandable, given Japan's world-beating record in the last couple of years is minimising covid deaths. But there is an economic cost to keeping the restrictions in place: Japan hasn't seen such a strong bounce in services activity as has been experienced elsewhere, particularly in the US. As an illustration, before covid, Japan was receiving more than 2.5m visitor arrivals a month; in March this year there were just 66,000.

In terms of the macroeconomy, the ending of inbound tourism hasn't just been important for domestic activity, but also for the current account. The services balance, which in the years preceding the pandemic had been steadily improving, has deteriorated post-2020 by around 1% of GDP.

External flows

It seems reasonable to assume that tourist inflows will resume if and when the border is opened further. Indeed, it seems likely that the cheapness of the JPY would drive quite a big bounce in tourism. This relates to a bigger point: that as much as interest rate differentials and monetary policy narratives are against the JPY, it isn't at all clear that the fall in the currency is reasonable given the other fundamentals for the currency.

Clearly, the depreciation of the currency isn't needed to offset rising inflation and so keep the country competitive. Not only does CPI inflation remain lower than other countries, but Japan's real effective exchange rate has fallen to the lowest level in fifty years. Despite the sharp rise in commodity prices that has pushed the trade balance into deficit – and the lack of earnings on tourism inflows – the current account remains in surplus. The reason is the large overseas investments made by Japanese companies in recent years, which are generating significant income inflows on the current account. The JPY value of the underlying investments, and of the resultant income, has been raised by the depreciation of the JPY.

More generally, Japan remains a large net external creditor economy. Of course, in other ways, particularly the sky-high domestic debt-to-GDP ratio, the economy is structurally weak. But when thinking about the intrinsic value of the currency, it is useful to contrast Japan with somewhere like the UK. While not as sharp as the move in the JPY, the GBP has also been falling against the USD, but the sterling REER has been appreciating because the inflation rate is heading towards double-digits. At the same time, the UK has a large current account deficit, and is a net foreign debtor. The main weight on the JPY, by contrast, is policy.

Domestic recovery

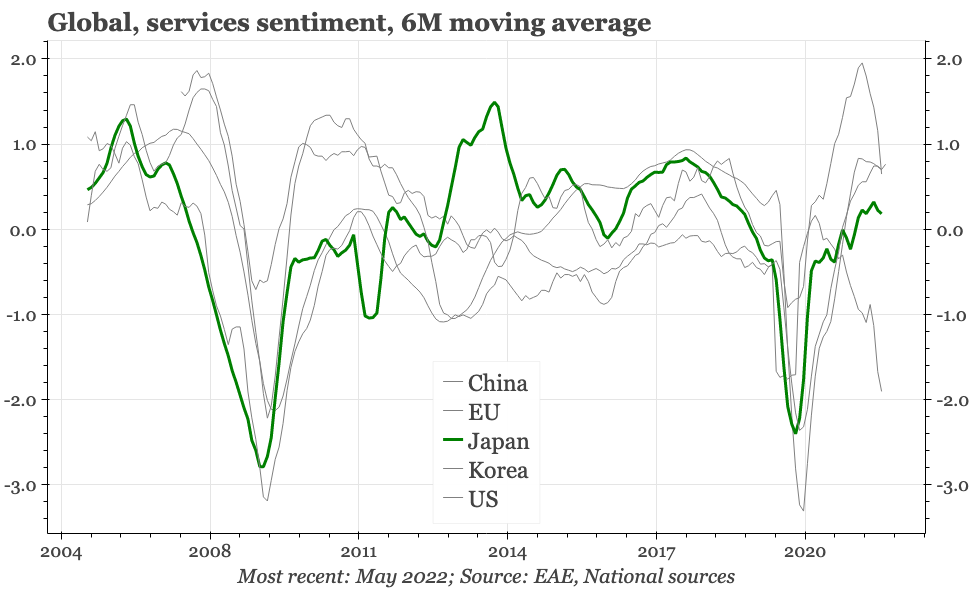

The silver lining for activity is that there should be room for the services sector to recover further from here. There's tentative evidence of that occurring, with services sentiment in this month's Economy Watchers survey reaching the highest level since October 2021. Comments by companies responding to the survey do suggest that this is being driven in part by a post-covid normalisation:

The situation has greatly changed from February, when the movement of people at night was extremely limited due to the implementation of priority measures such as for prevention of the spread of disease. Now we have many night customers. Events have increased, including a recent academic conference that took place for the first time in two years. Night customers, in particular, have gradually increased, helping us to raise sales. (Tokai: Taxi driver)

This month, we feel liberation from voluntary restrictions. This trend is likely to continue toward summer. As people are expected to plan excursion trips and proactive leisure during summer vacations, we hope that relevant goods will sell well. Opportunities for people to get together for events have increased, leading us to place hopes on massive relevant demand. (Kinki: Department store)

That offers quite the contrast with the US, where services sentiment in May dropped to the weakest level since April 2020. The rise in services activity in turn should create rising employment and a further tightening of the labour market. If that can happen, it would help to offset the hit to consumer incomes coming from rising commodity prices.

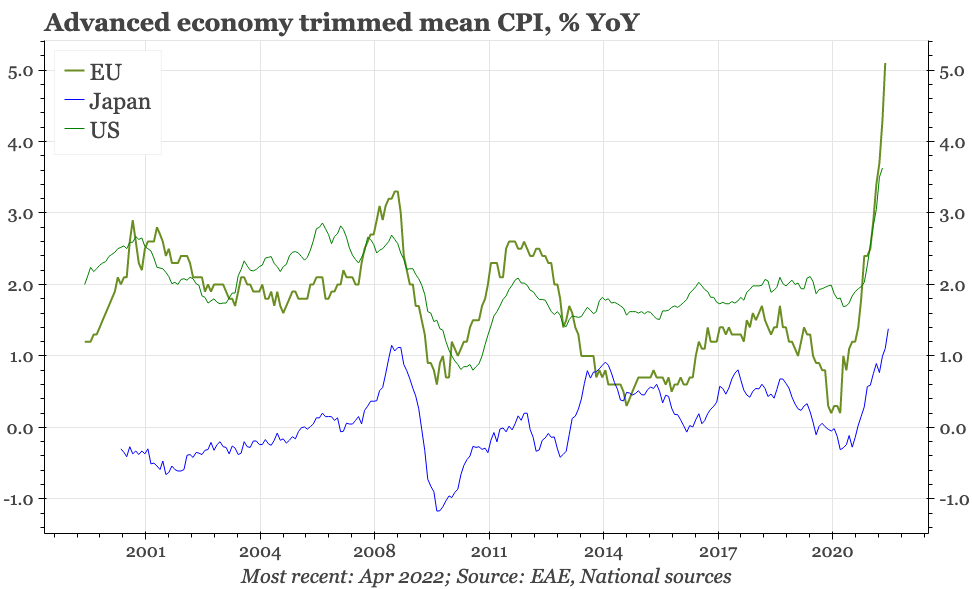

Opening the border and encouraging a normalisation of services wouldn't be a panacea for the economy, but using any available avenue to expand aggregate demand would seem to be a more optimal strategy right now than tightening policy. And unlike other economies where inflation is already sky-high, Japan does have room to increase demand. Inflation has increased, and is high by Japanese historical standards, but core CPI is still rising by only around 1% YoY.

In examining the post-covid gap between inflation in Japan and the other advanced economies, the BOJ has highlighted the bigger rebound in the labour force participation rate in Japan. That ordinarily would be a welcome development, continuing to blunt the negative impact on potential growth of a working population that continues to shrink in absolute terms. But while employment has bounced too, with both demand and supply of labour increasing, there isn't an overall tightening of the labour market that would boost wages. That in turn holds back price inflation, but also hinders the ability of the household sector to cope with the rise in prices that is being driven by the double whammy of commodity price strength and JPY weakness.

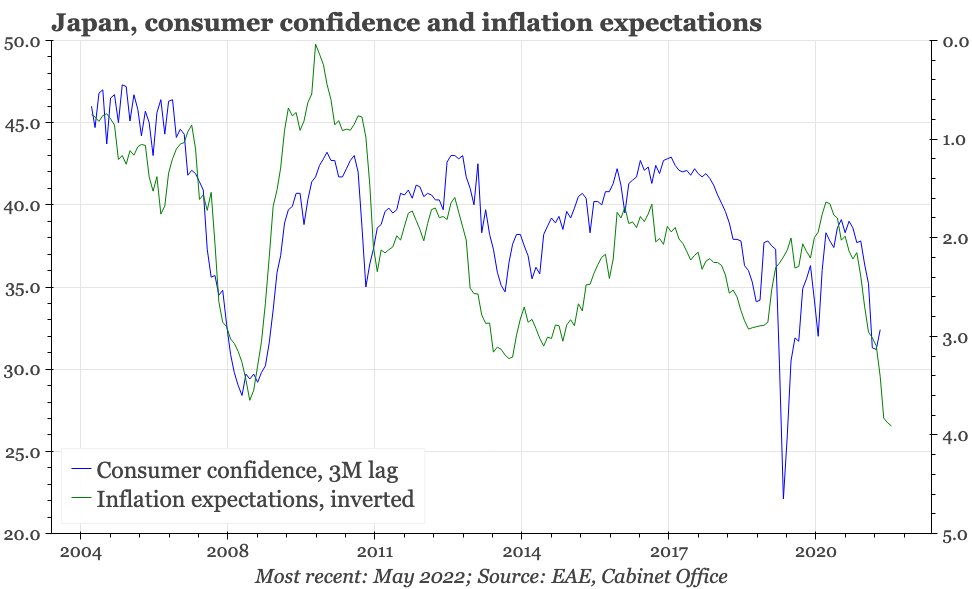

The consumer confidence survey suggests strongly that the rise in inflation so far has been damaging to consumers. Indeed, the BOJ's efforts since 2013 have done nothing to shake the inverse correlation between consumer confidence and inflation expectations, with the implication being that wage growth doesn't keep pace with prices. Against that backdrop, the weakness of the JPY and strength to commodity prices are not welcome developments. It is helpful then that there might be a lift in services activity, meaning the negative impact of rising inflation isn't the only factor affecting consumer sentiment.

Domestic politics

The government has introduced measures to try to mitigate the impact of the rising cost of living, including subsidies for oil wholesalers, and cash handouts for low-income households. But these haven't gone particularly well: one recent opinion poll found that 54.1% disapproved of the government’s response, with only 13.8% expressing approval. In an illustration of the political sensitivity of the rising cost of living, BOJ governor Kuroda was recently forced to retract remarks made to the Diet that “households are becoming more tolerant of price rises” (though he did have research to back up those comments).

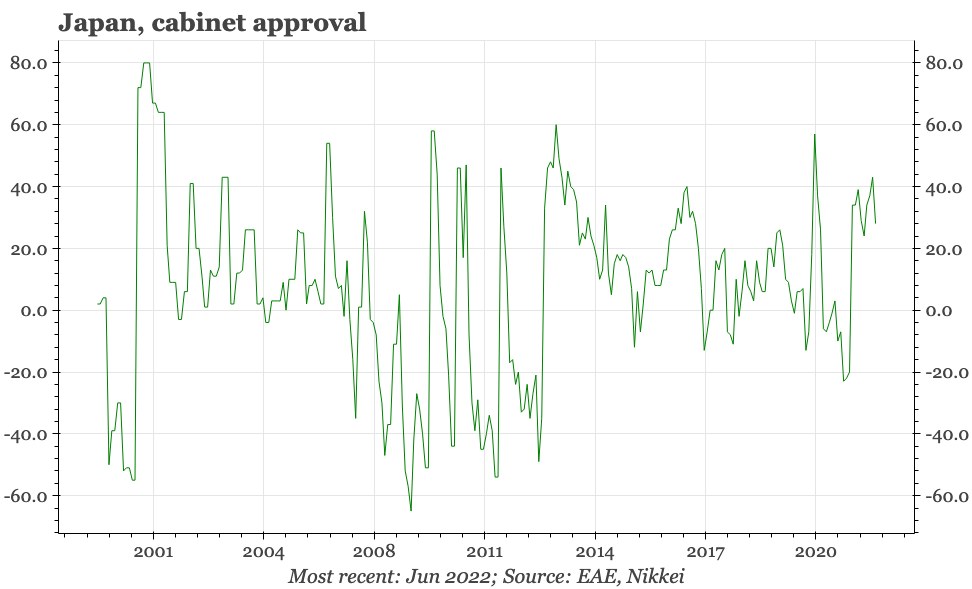

Despite all that, there's no sign that the impact of rising inflation on consumer sentiment hasn't yet coalesced into the sort of domestic political crisis that might force the BOJ to change track. Overall support for the Cabinet remains high, and the ruling LDP is likely to do well at the forthcoming July 10th upper house elections. Until and unless its own support starts to unravel, there doesn't seem an obvious trigger for the government to put political pressure on the BOJ to change course.